Summary

-

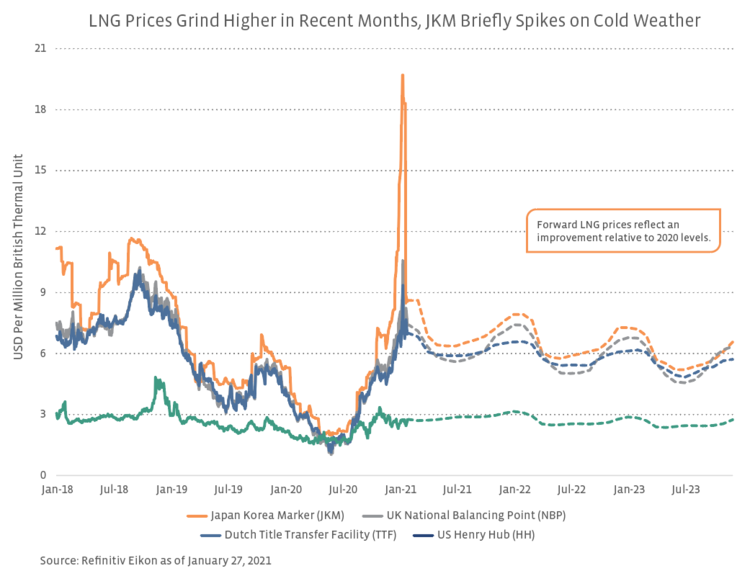

In January, a polar vortex in Asia and Europe drove LNG prices to record highs as demand for heating and power generation jumped considerably.

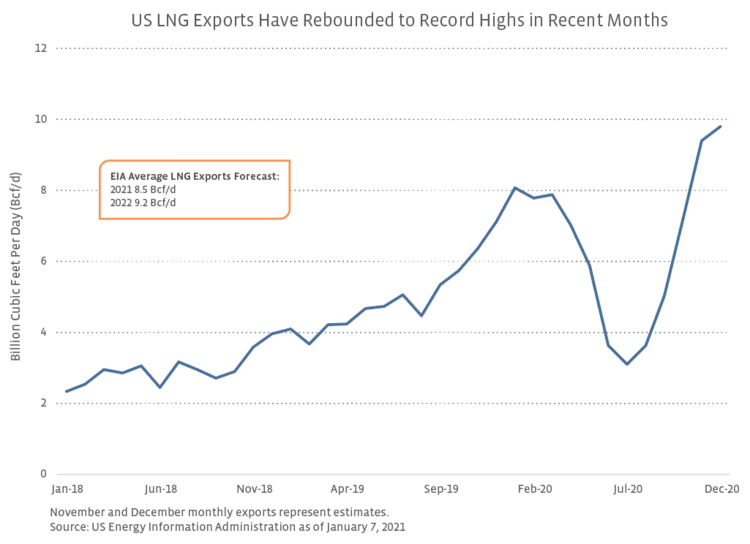

- As prices have improved and demand has picked up, US exports have rebounded from a two-year low in July to a record high of 9.8 Bcf/d in December, as estimated by the US Energy Information Administration (EIA).

- An improvement in LNG fundamentals has resulted in some optimism for current US LNG exporters and those developing new projects.

The market for liquefied natural gas (LNG) has improved dramatically in recent months with positive implications for US LNG exporters. Global LNG prices soared in response to a cold snap in Asia and Europe and supply outages that resulted in a tighter market for spot cargoes. Higher prices have contributed to record export levels from the US over the last few months, and would-be exporters are hopeful that recovering demand will benefit projects under development. This note provides a broad update on the macro environment for LNG and where US export projects stand in 2021.

LNG prices rally on supply interruptions and frigid weather in Asia and Europe.

The struggles for the LNG market entering 2020 continued for much of the year given significant macro headwinds. A general oversupply of natural gas globally and weak demand contributed to significantly lower prices, even after starting the year from a relatively low base as winter 2019-2020 proved mostly mild. The COVID-19 pandemic worsened the pain for US exporters as the prices of major benchmarks in Europe and Asia declined significantly and traded in a tight range with prices at Henry Hub in the US. During the spring and summer, Asian LNG benchmark Japan Korea Marker (JKM) and European benchmarks UK National Balancing Point (NBP) and Dutch Title Transfer Facility (TTF) declined to historic lows at or below $2 per million British thermal unit (MMBtu), with the gas price at Henry Hub even briefly overtaking prices in Europe and Asia. In combination with other factors, many US shipments became uneconomic during the height of the pandemic.

In recent months, however, LNG prices have improved significantly and provided a boost for US exporters. From June through the end of 2020, European and Asian prices largely moved in lockstep upward as mobility restrictions began to ease with (temporarily) lower case levels of COVID-19. Higher LNG prices may also have been driven by supply interruptions in countries such as Malaysia at the Bintulu LNG facility, Australia due to longer-than-expected downtime at Chevron’s (CVX) Gorgon LNG facility, and in the US due to a busy hurricane season on the Gulf Coast. These outages likely reduced the availability of contracted volumes relative to expectations. By October 23, JKM had risen to $7.25/MMBtu, while TTF increased to $5.35/MMBtu – the highest level for TTF since October 2019 and the highest price for JKM since February 2019. Prices in Europe and Asia continued to gain steam in November and December, but US prices at Henry Hub were largely rangebound with a brief increase above $3/MMBtu in November. The increase in price spreads between US and international prices has helped to drive a recovery in US exports, which will be discussed more below.

In January, a polar vortex in Asia and Europe drove prices to record highs as demand for heating and power generation jumped considerably. The rapid increase in demand exacerbated existing supply issues and tightened the market for spot cargoes, contributing to temporarily high prices. Refinitiv Eikon reported a record high closing front month price for JKM of $19.70/MMBtu on January 12, with TTF also rising substantially to $9.35/MMBtu on the same day. As of January 27, JKM has averaged $15.17/MMBtu in January following an average price of $9.27/MMBtu in December, both the highest levels since 2018. Forward prices have come off the record highs seen earlier this month but indicate some support for improved pricing going forward relative to 2020, with expected price spreads likely to continue to benefit US exporters.

US LNG exports rise to record highs at the end of 2020.

While LNG markets were challenged for much of 2020, the strong recovery in the fourth quarter drove a significant rebound in US LNG exports. The chart below plots monthly exports from January 2018 through December 2020. Keep in mind that LNG export capacity from the US increased by 3.3 Bcf/d in 2019 and by 2.7 Bcf/d in 2020, helping drive the steady increase up until 2020 (read more). In the wake of the pandemic, exports fell precipitously from 8.1 Bcf/d in January 2020 to 3.1 Bcf/d in July at the trough. Amid a depressed pricing environment, many buyers opted to cancel or defer dozens of US LNG cargoes over the summer, and LNG cargo cancellations crested in the summer at an estimated 45-50 in each month from June to August. Despite this wave of cancellations, some exporters, such as Cheniere Energy (LNG), were able to collect a fixed fee with the option to resell the canceled volumes in the market. Despite the difficulties facing US LNG exporters, contract protections have been on full display in steady guidance. Cheniere (LNG) has held its 2020 EBITDA guidance steady at $3.95 billion and is guiding to 2.5% EBITDA growth in 2021. Meanwhile, Cheniere Energy Partners (CQP) delivered on its 2020 distribution expectations by declaring total distributions of $2.59 per unit for 2020 and is guiding to 2.3% distribution per unit growth at the midpoint for 2021 year-over-year.

As prices have improved and demand has picked up, US exports have rebounded from a two-year low in July to set consecutive record highs of 9.4 Bcf/d in November and 9.8 Bcf/d in December, as estimated by the US Energy Information Administration (EIA). Utilization of US LNG export capacity was elevated at an estimated 91% in December, with exporters shipping a record 89 cargoes. The EIA projects that exports will average a robust 8.5 Bcf/d in 2021 (including expectations for volumes to remain near record levels of 9.5 Bcf/d in 1Q21) and 9.2 Bcf/d in 2022. These projections are emblematic of a more constructive outlook for US exports moving forward as the global economy gradually recovers from COVID-19 and the long-term thesis for LNG demand abroad remains intact.

LNG projects continue to progress as macro headwinds have subsided somewhat.

With several major liquefaction projects in the works, midstream LNG companies have been focused on execution and development. In mid-December, Cheniere shipped its first commissioning cargo from Train 3 at its Corpus Christi LNG facility. The company expects to reach substantial completion on the project ahead of schedule in 1Q21 compared to its prior target of 1H21. Similarly, CEO Mike Sabel of private operator Venture Global noted in December that the company is running ahead of schedule on the construction of Calcasieu Pass LNG, with six of 18 production units expected in place by mid-February and commercial operations targeted for 2022. The first phase of Venture Global’s second facility, Plaquemines LNG, is expected to be fully contracted by the end of June with a final investment decision (FID) still expected in 2021. Tellurian (TELL) CEO Charif Souki said in January that the company hopes to begin construction on Driftwood LNG this summer and noted customer interest had increased significantly over the prior month. Through January 28, TELL has risen by more than 120% year-to-date, with gains likely driven by optimism around improved LNG fundamentals and updates surrounding Driftwood. NextDecade (NEXT) is also maintaining its 2021 target for FID on Rio Grande LNG for a minimum of two trains with commercial discussions ongoing.

Bottom Line

An improvement in LNG fundamentals has resulted in optimism for current US LNG exporters and those developing projects, and management teams are seeking to take advantage of subsiding headwinds to move projects toward the finish line. With global natural gas demand expected to rise 30% by 2040 in one International Energy Agency projection from October 2020, US exporters are helping to connect domestic natural gas production with growing gas demand abroad.