Is a global supply gap looming, and how could the US help fill the gap?

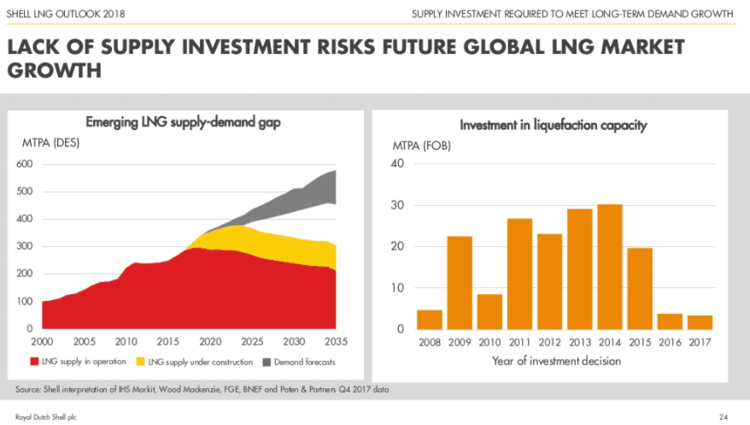

Shell (RDS-A) has highlighted the potential for a supply gap in the LNG market in the mid-2020’s in the slide below from its LNG Outlook 2018. The chart on the right shows the dearth in final investment decisions (FID) for adding liquefaction capacity globally in 2016-17. For its part, the US did not have any FIDs in these years. Cheniere’s FID for Train 3 at Corpus Christi (0.7 Bcf/d of capacity) in May was the first FID for liquefaction capacity in the US since 2015. The concern is that the lack of FIDs in recent years will lead to insufficient supply in the 2020’s.

Source: Shell LNG Outlook 2018

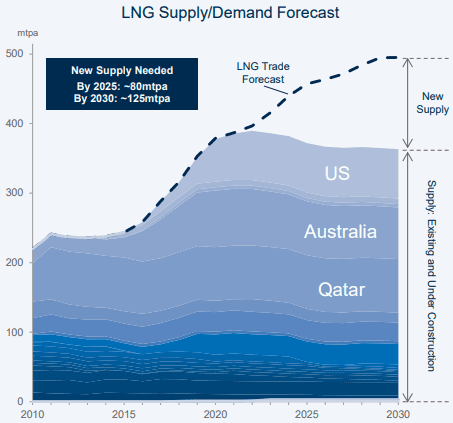

Similarly, Cheniere has forecasted in its presentations that another 80 MMTPA (10.5 Bcf/d) of LNG supply will be needed by 2025 as shown below. By 2030, Cheniere estimates 125 MMTPA (16.4 Bcf/d) of supply will be needed in addition to what’s currently operating and under construction.

Source: Cheniere Investor Update Presentation from May 29-30, 2018

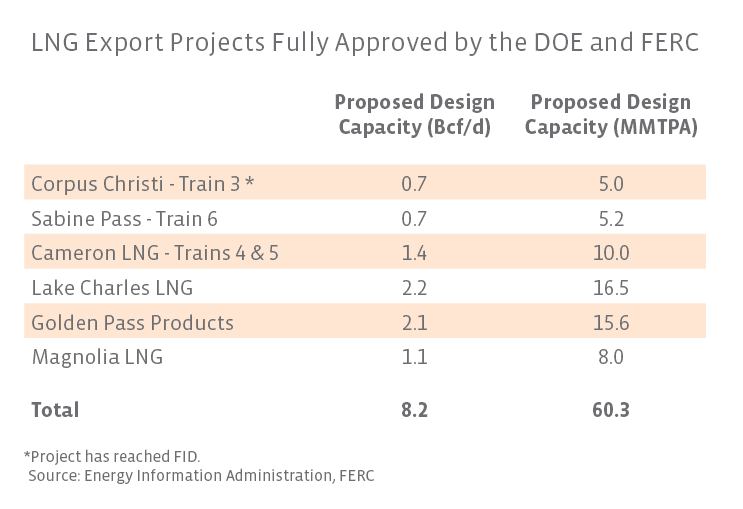

There are several expansions and new projects on the drawing board in the US that could help fill this supply gap. Some projects expected to come online in 2019 could add trains in the future. In addition to Train 3 at its Corpus Christi terminal, Cheniere has proposed seven additional midscale trains at Corpus Christi and also has the necessary permits to add a sixth train at Sabine Pass (0.7 Bcf/d of capacity). Sempra Energy’s (SRE) joint venture Cameron LNG project has received regulatory approval for two additional trains (1.4 Bcf/d of capacity). Freeport LNG has applied for FERC approval to build and operate a fourth train (0.7 Bcf/d of capacity). Aside from expansions, there are projects that have been fully approved but have not reached FID including Energy Transfer’s (ETE, ETP) Lake Charles LNG, Exxon’s (XOM) Golden Pass LNG joint venture with Qatar Petroleum, and Magnolia LNG.

There are several more LNG export projects that have been proposed to the Federal Energy Regulatory Commission (FERC), which oversees the siting and construction of LNG export facilities. Notable proposed projects include Sempra’s Port Arthur LNG, which announced a 20-year contract with Polish Oil & Gas last month. The project has not reached FID but is expected to begin exporting LNG in 2023. Also on the list, Tellurian’s (TELL) Driftwood LNG is expected to begin operations in 2023 and to have a total capacity of 27.6 million tons per annum (MMTPA), which equates to nearly 4 Bcf/d.

Clearly, projects will need to reach FID and begin construction if they are to help fill the potential LNG supply gap. Before reaching FID, companies will want to have financing decided and commercial contracts in place covering the capacity (in other words, assurance of sales). Shell has attributed the lack of FIDs to a disconnect between buyers that prefer short-term contracts or spot deliveries without a contract and LNG suppliers that want long-term contracts to support the hefty investment in liquefaction capacity. While this is an issue facing LNG projects globally, US trade policy is a potential obstacle specific to projects in the US.

What are the implications of the trade dispute with China?

Thus far, LNG exports have not been targeted by China in the ongoing trade dispute between the US and China. China led global growth in LNG imports last year, increasing its imports by 1 Bcf/d to become the world’s second-largest LNG importer behind Japan. China alone accounted for 44% of the global increase in LNG imports in 2017. If LNG exports were to come under fire in the trade dispute, it would likely be a negative for LNG projects in the US looking to secure future sales contracts with Chinese customers. Already, some commercial agreements may be on hold until there is more visibility, likely delaying additional FIDs. That said, it’s worth noting that 40 countries imported LNG last year, and the US exported LNG to 25 different countries. While China is a major player in the LNG market, it’s not the only customer. As highlighted by the contract inked by Port Arthur LNG, Europe is clearly a market for US LNG exports as countries look to diversify their gas supply from Russia.

Stay tuned for next week!

We’ve barely scratched the surface in global LNG markets, neglecting planned projects in other parts of the world to specifically focus on the US. Clearly, these projects will compete with the US, and US projects will compete against each other. Stay tuned for next week as we discuss the broader benefits of US LNG exports for midstream companies and gas producers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}