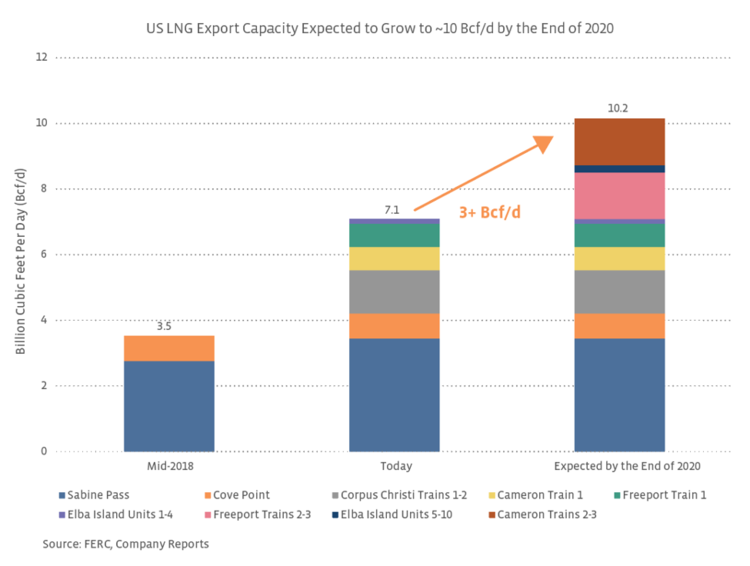

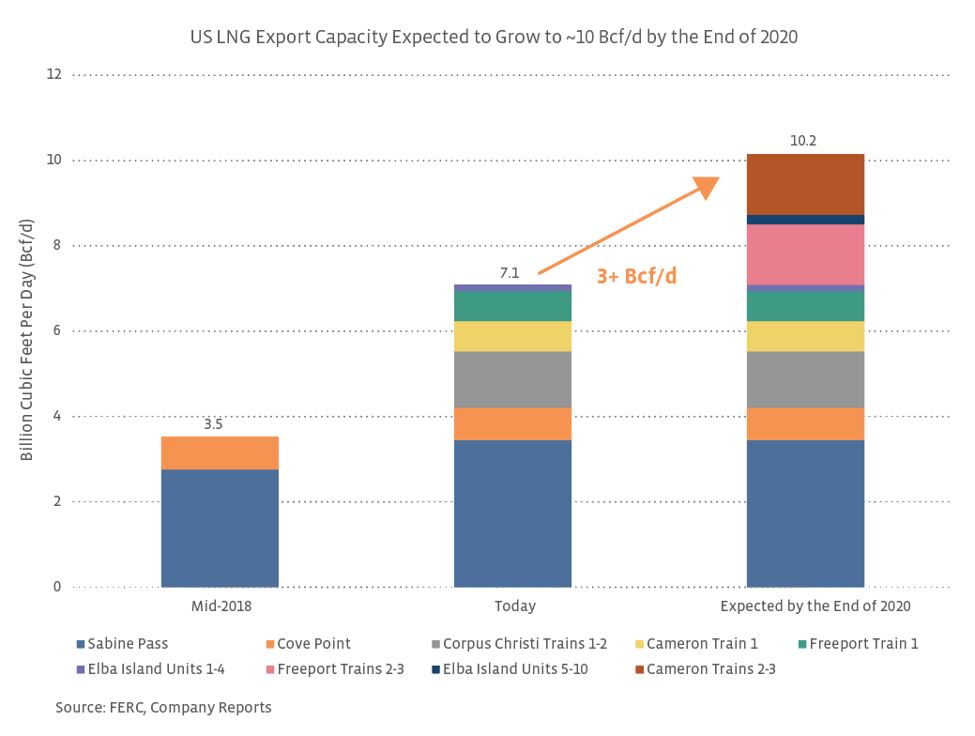

Once these facilities reach completion, the US will likely see more measured capacity additions in 2021 and 2022. Cheniere (LNG) expects its third train at Corpus Christi to be completed in the first half of 2021, and Venture Global’s Calcasieu Pass is anticipating a 2022 startup. Projects in the early stages of construction or nearing final investment decision are anticipated to come online in 2023-2025. Four projects awaiting final investment decision received FERC approval in late 2019 and DOE approval this month to export to countries without free trade agreements with the US, including NextDecade’s (NEXT) Rio Grande LNG, Annova LNG, Texas LNG and stage 3 of Cheniere’s (LNG) Corpus Christi facility.

Global LNG price weakness continues.

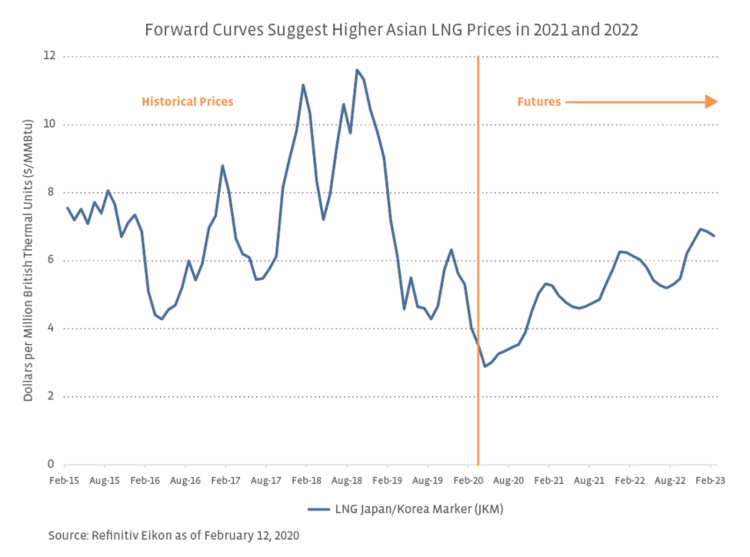

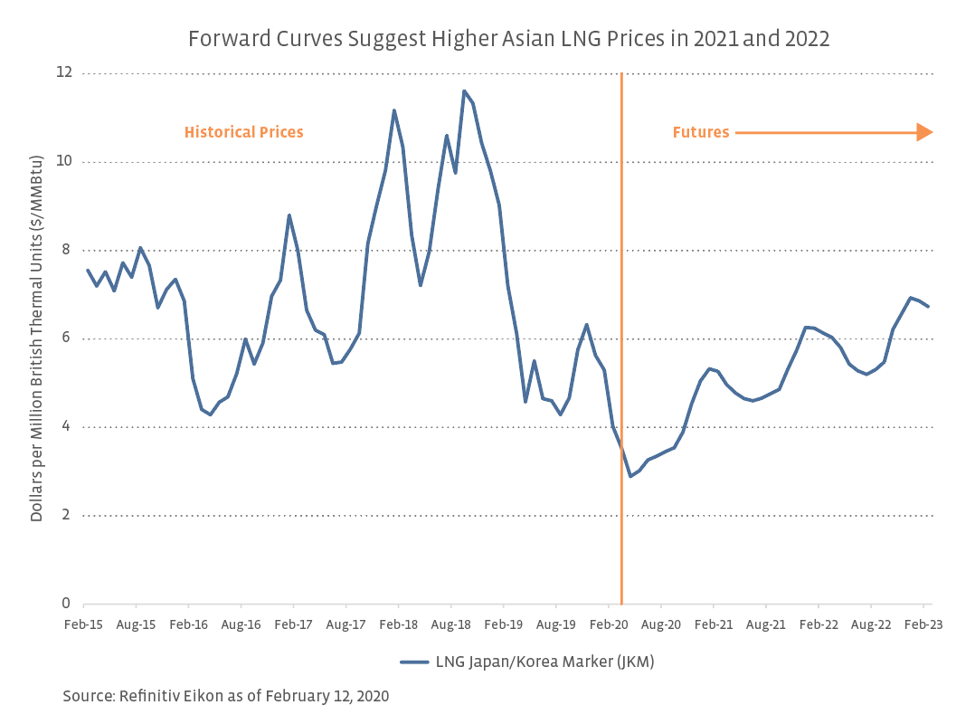

From a macro perspective, the startup of new US projects this year likely exacerbates a weak pricing environment for LNG globally. Prices were already pressured by warmer weather in many geographies and an oversupply of LNG, but fundamentals have further deteriorated due to demand impacts from the coronavirus (see next section for more on China). As shown in the chart below, LNG prices in Asia have fallen significantly, but futures point to a price recovery beginning in 2H20.

It’s important to keep in mind that US LNG exports are often covered by long-term contracts with a fee. For example, the capacity of Dominion Energy’s (D) Cove Point facility is contracted under a fixed reservation fee with 20-year take-or-pay contracts. Cheniere (LNG) has ~80% of its liquefaction platform covered by long-term contracts and cites $5.5 billion of annual fixed fees. For Sabine Pass trains 1-5, Cheniere’s customers pay a fixed fee per million British thermal unit (MMBtu) of LNG and a variable fee at 115% of Henry Hub natural gas prices. While fee-based business helps insulate from weaker prices, projects with extra volumes to sell on a spot basis (uncontracted) are more likely to be negatively impacted by price weakness.

What about China? Implications of the trade deal and coronavirus.

With China expected to drive much of the growth in LNG demand over the coming years, developments in recent weeks garner discussion. On the surface, the announcement of the Phase One trade deal with China last month reads positively for US LNG export projects. The deal calls for an incremental $52.4 billion in US energy purchases for 2020-21 compared to 2017 with the trajectory of increases expected to continue for 2022-2025. In the agreement, energy includes LNG, crude, refined products (including propane and butane), and coal. Notably, the deal does not specify how much could be represented by LNG purchases, and questions have been raised about China’s ability to buy the incremental energy amounts outlined.

Even if the coronavirus had not impacted Chinese demand, it’s unlikely that LNG exports to China would have increased significantly in the near term. For one, a 25% tariff on US LNG is still in place, while lighter tariffs on US crude were halved from 5% to 2.5%. Today, media outlets are reporting that China will begin taking applications for one-year exemptions to tariffs on a variety of US imports, including crude and LNG. This could pave the way for more spot LNG exports to China eventually. Through November 2019 (latest monthly data), LNG has not been exported to China since February 2019, while exports of crude and liquefied petroleum gases continued. Additionally, there are no long-term contracts of size between US LNG projects and Chinese customers,so any exports would likely be spot purchases, which limits the available volumes. While the near-term impact seems muted, the longer-term commentary in the US-China trade deal regarding purchases for 2022-2025 may be encouraging to US projects trying to firm up customers.

Currently, the coronavirus outbreak has weighed on Chinese demand and complicated relationships between Chinese firms and their customers. China’s largest purchaser of LNG, China National Offshore Oil Corp (CNOOC), has rejected cargoes under force majeure because of the virus. Shell (RDS-A) and Total (TOT) have rejected the force majeure. The interactions may give some pause to US LNG projects considering signing long-term contracts with a Chinese customer. On the bright side, US LNG projects in operation are not having to grapple with these issues given the lack of sizable, long-term offtake agreements with a Chinese counterpart.

Bottom line

The impending addition of new US LNG export capacity likely exacerbates the current oversupply in today’s market, which has been augmented by the impact of the coronavirus. Fortunately, US LNG projects are better insulated from some of the market headwinds given their customer base and contract structure.

{kind=link}

{kind=link}