Improving demand supports a reversal of industry measures taken in 2Q.

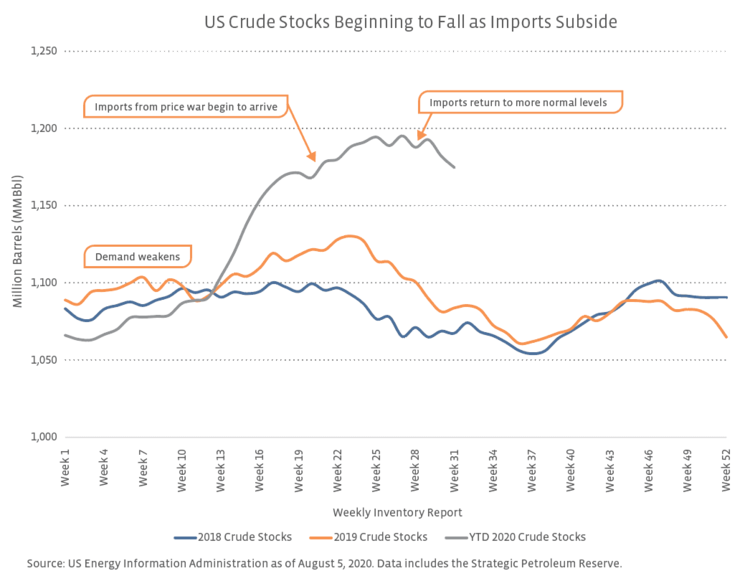

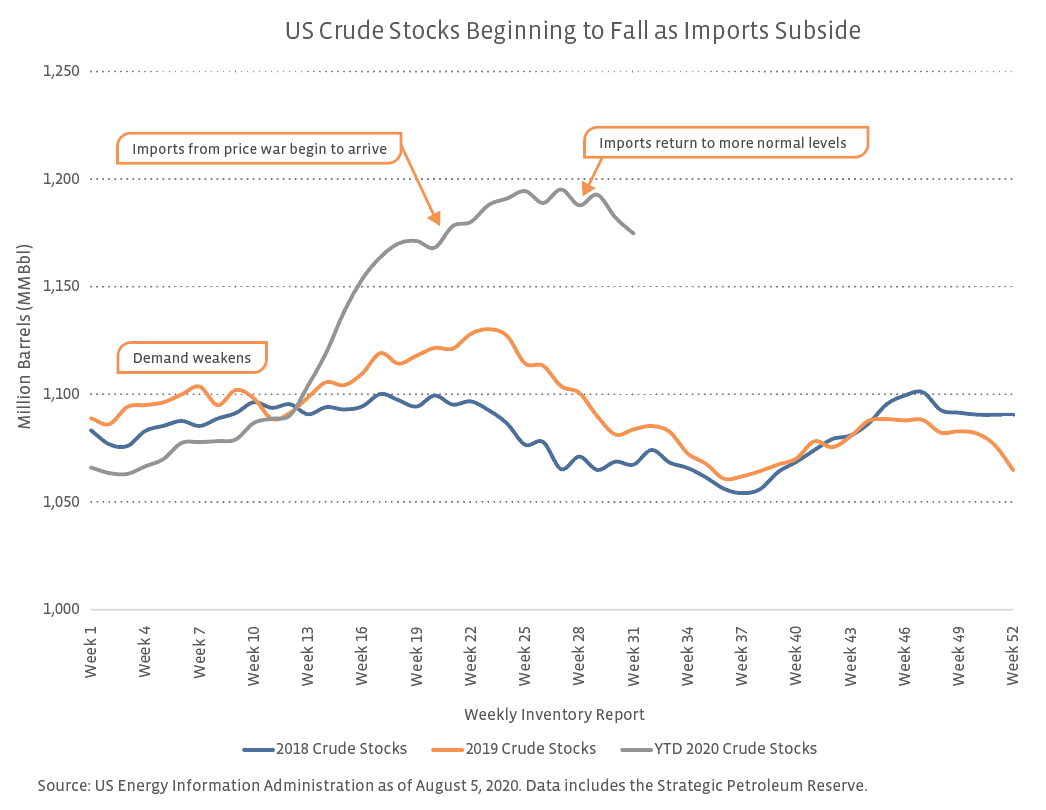

Moving into the summer, demand has improved noticeably, and some of the headwinds from earlier this year and industry responses to those headwinds are unwinding. Based on a trailing four-week average, US gasoline demand is down 10.8% relative to 2019. On their earnings call last week, management of refiner Valero (VLO) noted that gasoline demand in June for their system was back up to 88% of normal after falling by about 50%, and they were seeing improved demand in export markets as well. Refining utilization remains well below normal for this time of year but has ticked up to 79.6% as of the end of July. West Texas Intermediate oil prices have been relatively stable around $40 per barrel since June, and the contango in the futures curve has moderated – another hallmark of an improved market. The stability in oil is allowing producers to restore volumes that were curtailed in April and May. For example, ConocoPhillips (COP) noted on last week’s earnings call that they expect curtailed production from the Lower 48 to be fully restored by September. In short, demand, refinery utilization, and oil production are heading in the right direction, but the ongoing recovery is still somewhat fragile, requiring a careful balancing act by the industry.

What are the implications for midstream?

Improvements in demand and production trends are welcome developments for midstream as these result in higher volumes. Many companies have noted the benefits of minimum volume commitments (MVCs) and deficiency payments in their 2Q20 results, which have helped protect cash flows from lower throughput. While MVCs are an important backstop, improving fundamentals are constructive and reinforce the notion that 2Q was likely the trough for this year.

Many investors expected outsized benefits to midstream in 2Q from their storage capacity given the steep contango observed earlier this year as inventories jumped (read more). While storage is vital in supporting industry operations and allowing flexibility for refiners and producers, it is often overlooked until it becomes scarce. For midstream, storage tends to be contracted for long-term periods, leaving less storage available to capitalize on contango opportunities (i.e. opportunities to store hydrocarbons today to sell at a higher price in the future). However, some midstream names saw benefits in 2Q or anticipate benefits in the balance of this year. For example, Plains All American (PAA) increased its 2020 EBITDA guidance by 3% in part due to the benefits of contango opportunities in its Supply and Logistics business. Enterprise Products Partners (EPD) discussed a $500-600 million benefit this year from spreads, including contango benefits, and expects to end up at the higher end of that range. ONEOK (OKE) noted on its 2Q earnings call that it would realize contango benefits from 2Q in the second half of this year. Storage and contango opportunities have been a small silver lining in a tough environment.

Bottom line

The fundamentals for the US oil market have improved noticeably in recent months with the pace of the demand recovery thus far likely proving better than feared. Improved demand paves the way for increasing refining utilization and restored production incentivized by more stable oil prices – welcome developments for midstream.

{kind=link}