With benchmark West Texas Intermediate oil prices hovering around $22 per barrel for the June contract and regional prices even lower, netbacks for producers are admittedly dismal, making the current outlook for US oil production tenuous. Headlines surrounding potential state or federal government interventions further complicate the outlook. Today’s note examines recent production-related updates from a variety of stakeholders, including oilfield service providers, exploration and production (E&P) companies, and the Energy Information Administration (EIA), as well as the implications of these updates for midstream.

Upstream activity falling sharply without government intervention.

To state the obvious, the current price environment provides little incentive to bring new wells to production. E&Ps have slashed growth capital spending with the dual purpose of effectively storing hydrocarbons in the ground and preserving cash. From the end of February through Friday, the Baker Hughes (BKR) US oil rig count has fallen by 240 rigs (-35%) to 438 rigs. For context, the oil rig count reached a relative bottom of 316 rigs in May 2016 in the last major downturn – three months after oil’s relative bottom in February 2016. The rig count likely has much further to fall. On its 1Q earnings call on Friday, global oilfield services bellwether Schlumberger (SLB) estimated that North American rig and completion activity would fall 40-60% sequentially in 2Q20. On its earnings call this morning, Halliburton (HAL) noted that North American activity is in freefall, and E&P capex is trending towards a 50% decrease year over year. Management expects onshore activity to remain depressed through year-end 2020. With fewer new wells being drilled and completed, shale production will be subject to natural declines, which can be considerable given the front-loaded production profile of shale wells.

Activity is falling in response to the current market environment, regardless of potential government interventions. The Texas Railroad Commission held a well-publicized open meeting last week to receive feedback on potentially prorating oil production, with several industry representatives speaking against the measure, including Co-CEO of Enterprise Products Partners (EPD) Jim Teague. At the federal level, reports surfaced last week that the Trump administration is considering a plan to pay producers for leaving oil in reservoirs as additions to federal strategic reserves. While government intervention comes with its own challenges around implementation and the potential for ensuing court cases, individual companies may preemptively shut in production in the near term due to unattractive prices and/or storage constraints.

To that end, last Thursday, ConocoPhillips (COP) announced that it would reduce production at its Surmont oil sands project in Canada by 75% (100,000 barrels of oil per day on a gross basis) and curtail production across the Lower 48 by ~125,000 barrels per day starting next month. COP expects to make future curtailment decisions on a month-to-month basis, importantly noting that the decisions are subject to operating agreements and contractual obligations. When asked on the corresponding conference call about the industry more broadly, COP’s Chairman and CEO Ryan Lance indicated that he expects similar actions by other E&Ps to be forthcoming, though other producers may be more inclined to maintain volumes to generate cash flow. As storage levels increase (read more), producers are likely going to be forced to temporarily curtail production if there’s nowhere for the crude to move. In its Short-Term Energy Outlook from April 7 (prior to the OPEC+ cut agreement), the EIA estimated that US oil production would fall by 1.6 million barrels per day (MMBpd) over the rest of this year, decreasing from 12.7 MMBpd in March to 11.1 MMBpd (down 12.6%) in December 2020 and stabilizing in 2021. The EIA noted the increased uncertainty around forecasts given ongoing developments with the COVID-19 pandemic.

What does this mean for midstream?

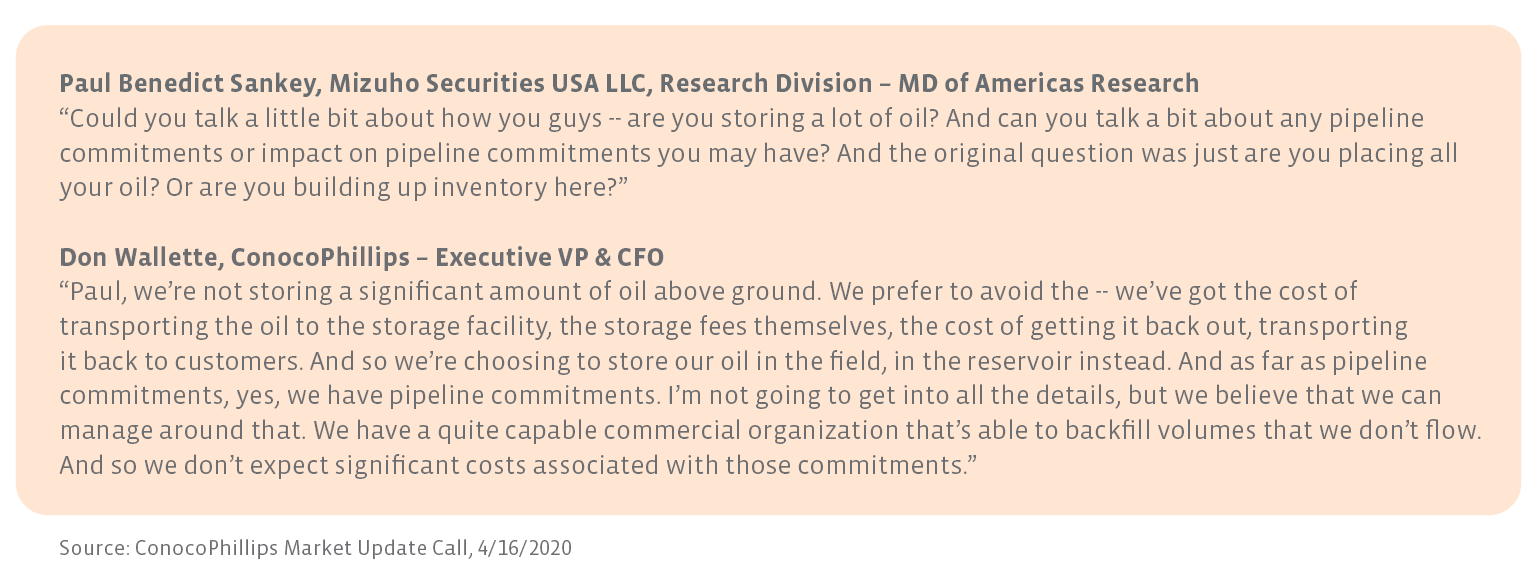

For the midstream business model, growing production is admittedly more constructive than declines. That said, contract features like minimum volume commitments (read more) are meant to protect midstream providers in challenging environments. When asked about pipeline commitments on last week’s call (see text box below), COP’s management noted that they do not expect significant costs related to the commitments and would be able to manage around them. For midstream, the commentary is reassuring, or at the least, does not raise concerns. On another positive note for the potential speed of recovery, COP expects robust production from unconventional wells in the Lower 48 when brought back online.

{kind=link}