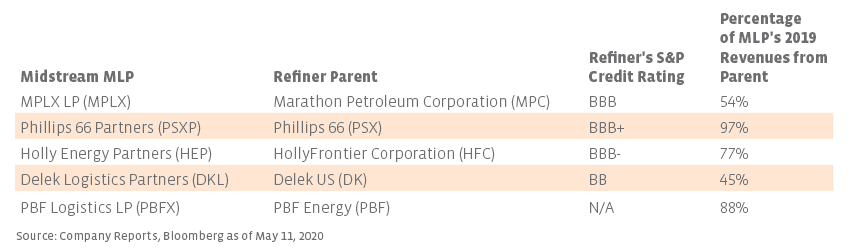

Setting aside MLPs with refiner parents, many other MLPs have significant exposure to refiners. MLPs may operate crude pipelines that supply refineries or product pipelines that take refined products away from the refinery and deliver them to end markets. NuStar Energy (NS) went public in 2001 as Shamrock Logistics and was part of Ultramar Diamond Shamrock, which Valero (VLO) acquired. In 2006, the renamed Valero LP separated from VLO and was renamed NuStar, but VLO remains a significant customer of NS given the legacy asset base. VLO accounted for 28% of pipeline segment revenues in 2019 and carries an investment-grade credit rating with a stable outlook. In 2019, MPC and PSX accounted for 12% and 11% of total revenues for Plains All American (PAA), respectively. MPC was also the largest customer of EnLink Midstream (ENLC) last year, accounting for 13.8% of 2019 revenues. While no customer accounts for 10% or more of revenues, Magellan Midstream Partners (MMP) provides service to a number of refiners. Last year, 62% of MMP’s refined product volumes originated from direct pipeline connections to 18 refineries, including facilities owned by HFC, MPC, PSX, and VLO.

While the demand impacts of COVID-19 have harmed refiners given weaker crack spreads, the profitability of refiners is less dependent on an oil price recovery than their upstream counterparts. The differentiated sensitivity of refiners to oil prices may help diversify counterparty risk exposure for those MLPs (read more) that also have customers producing oil and gas. The size and credit quality of some of the larger refiners is an asset for their related MLPs.

{kind=link}