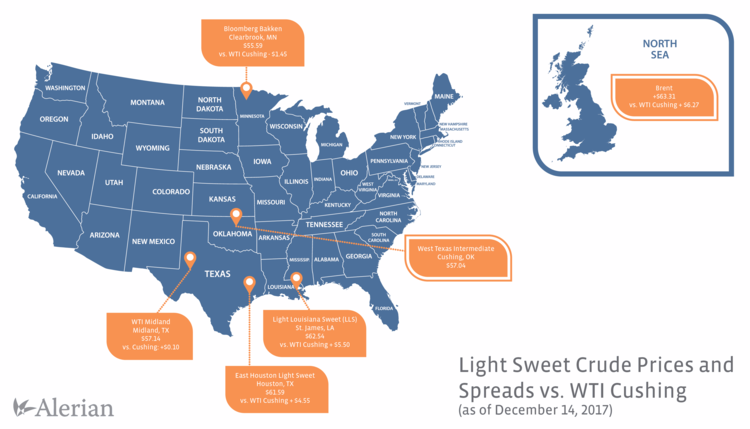

In general, the price for similar crude on the Gulf Coast tends to be higher than at Clearbrook or Cushing, because the Gulf Coast is the major destination for crude and the higher price reflects the cost of shipping crude to that market. Why does crude flow to the Gulf Coast? Simply, it’s because roughly half of US refining capacity is located there and the majority of US crude exports are shipped from the Gulf Coast.

To use an example, the price of crude at Houston should be higher than the price at Cushing with the difference based on the transportation cost of moving barrels from Cushing to Houston. The highest pipeline tariff rate, which would be the uncommitted pipeline tariff, should largely determine the spread. However, spreads don’t always conform to transportation costs, and that’s when things tend to get interesting.

Why do Crude Spreads Matter for MLPs?

- Crude spreads wider than typical transportation costs can indicate a need for more infrastructure.

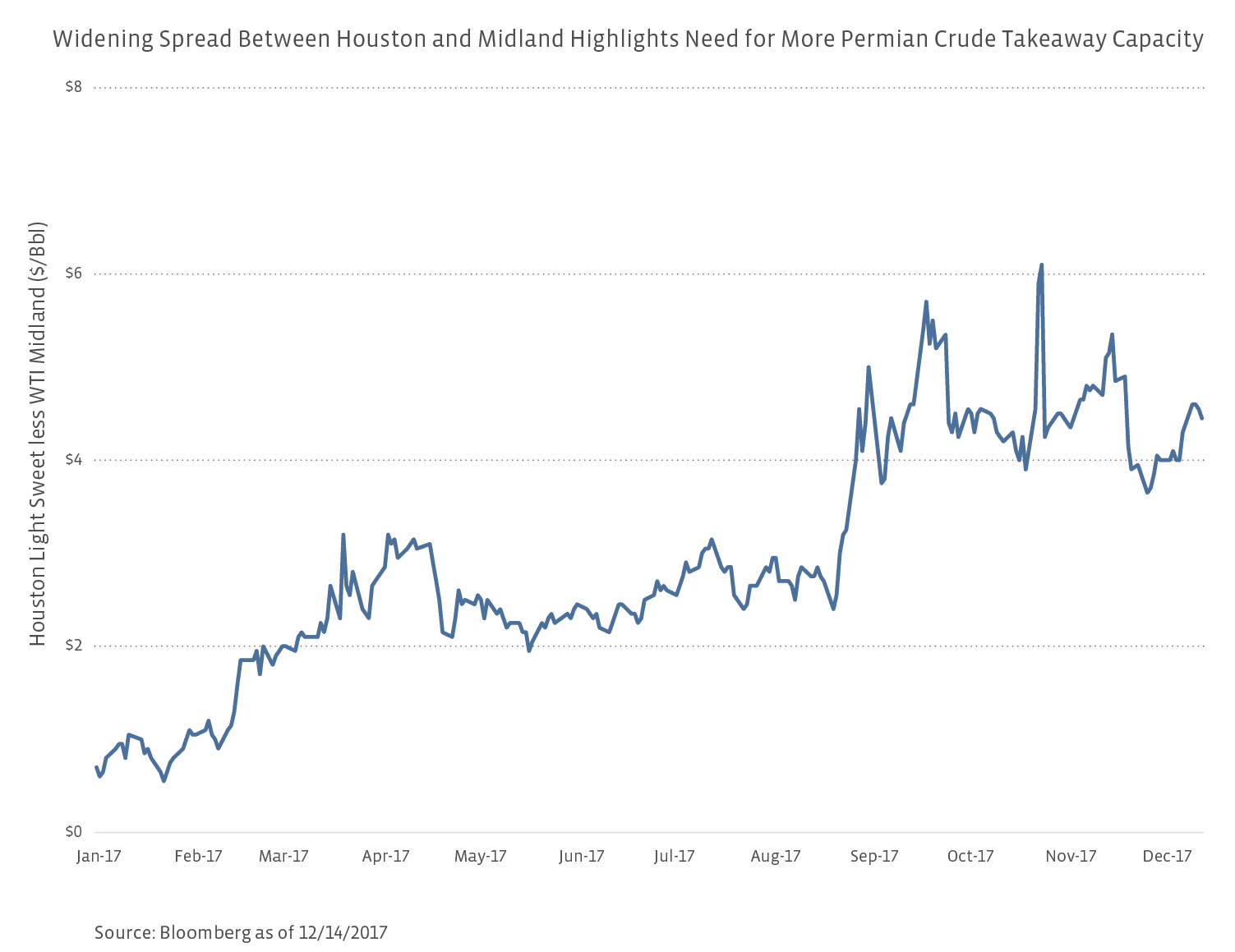

Persistently wide crude spreads that exceed pipeline transportation costs can indicate a need for more infrastructure and can be a helpful backdrop for encouraging shippers to sign long-term contracts for pipeline capacity. The current spread between prices at Cushing and Midland compared to the Gulf Coast is a good example of a structural issue. As of December 14, crude at Midland was pricing $4.45 per barrel below crude in Houston, which is wider than the applicable pipeline tariff. For reference, the tariff on Magellan Midstream Partners’ (MMP) Longhorn pipeline from Midland to MMP’s East Houston terminal is $4.1446 per barrel for spot shipments or $2.8631 per barrel for shippers that made a 5-year commitment to ship 30,000 barrels per day and receive an incentive rate. You can see below how the discount in Midland crude relative to Houston has widened over the course of this year.

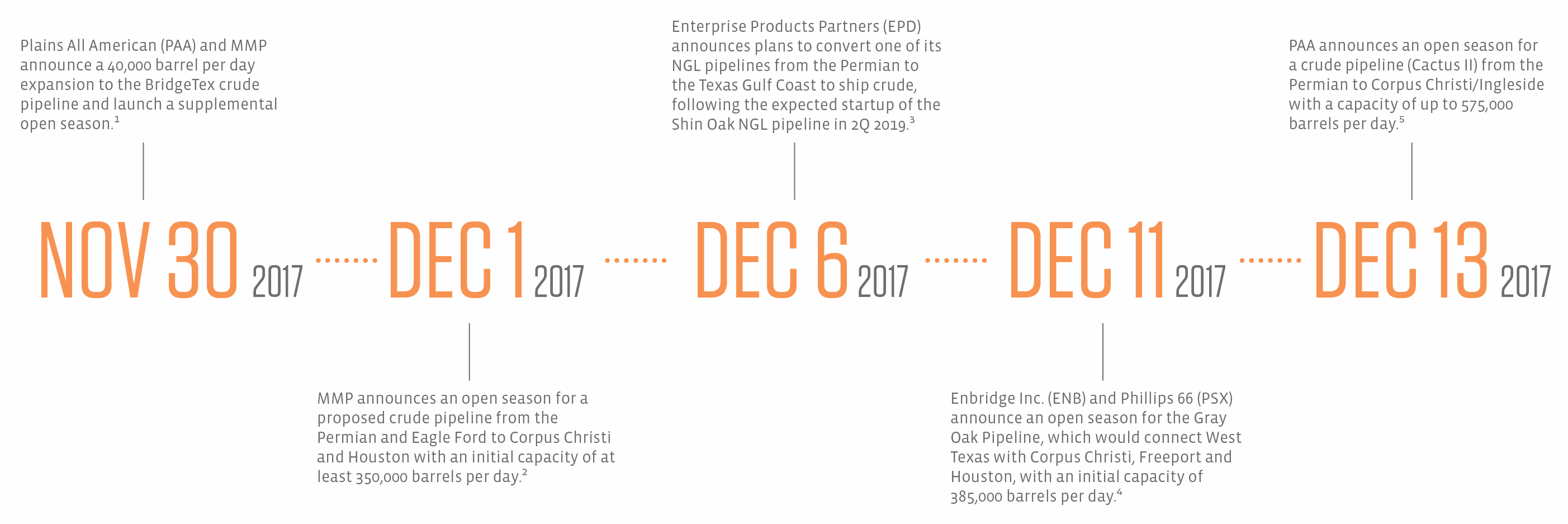

To be clear, expectations of future production growth and shippers’ desire to sign up for capacity are key to determining what incremental pipeline capacity will be needed — more so than current crude spreads. Pipeline projects announced today likely won’t be in service until 2019, and pipeline projects already in progress are more meaningful for addressing current crude spreads. However, the widened crude spread between Midland and Houston arguably creates a constructive background for negotiating tariff rates and getting shippers to sign up for capacity. It’s certainly not the only factor at play, but there has been a slew of Permian crude pipeline announcements recently:

In addition to the announcements in the timeline, two notable Permian pipeline-related announcements were made on December 21. EPIC announced that it had received sufficient customer interest to sanction its crude pipeline from the Permian to Corpus Christi, which will have a capacity of up to 590,000 barrels per day. Buckeye Partners (BPL) announced an open season for its South Texas Gateway Pipeline, which will transport up to 600,000 barrels per day of crude and condensate from the Permian and Gardendale, Texas, to the Texas Gulf Coast.

- Crude spreads can have implications for uncommitted tariff rates.

Crude spreads can have implications for the uncommitted tariff rates that pipelines can charge, pending regulatory approval. For this discussion, we’re just talking about the uncommitted, or spot, rates and not the contractual rates charged to committed shippers. Therefore, the positive or negative impact can be somewhat marginal, depending on the portion of the pipeline’s capacity that is available for spot shipments. Typically, only a small percentage of a pipeline’s overall capacity is left available for spot shipment, with most of the capacity covered under long-term contracts.

When crude spreads widen significantly between two markets connected by an existing pipeline, the pipeline operator may be able to raise uncommitted rates. TransCanada’s (TRP) Marketlink pipeline, which flows from Cushing to Port Arthur and Houston, Texas, is a good example in today’s pricing environment. As you can see in the map, the price difference between Cushing and Houston was recently $4.55 per barrel. Marketlink received approval from the Federal Energy Regulatory Commission (FERC) to increase the temporary discounted uncommitted rate for light crude to $3.00 per barrel effective December 1, 2017 and to raise that same rate for light and heavy crude to $3.25 per barrel effective January 1, 2018. To be clear, FERC sets the ceiling rate – not the rate that must be charged.

Crude spreads can also pressure pipeline operators to lower their uncommitted rates. If typical pricing relationships invert or if crude spreads are narrower than the uncommitted tariff rate, pipelines may seek approval to lower their uncommitted rates to better incentivize spot shipping. Again, keep in mind that this is just on the rate for moving uncommitted volumes.

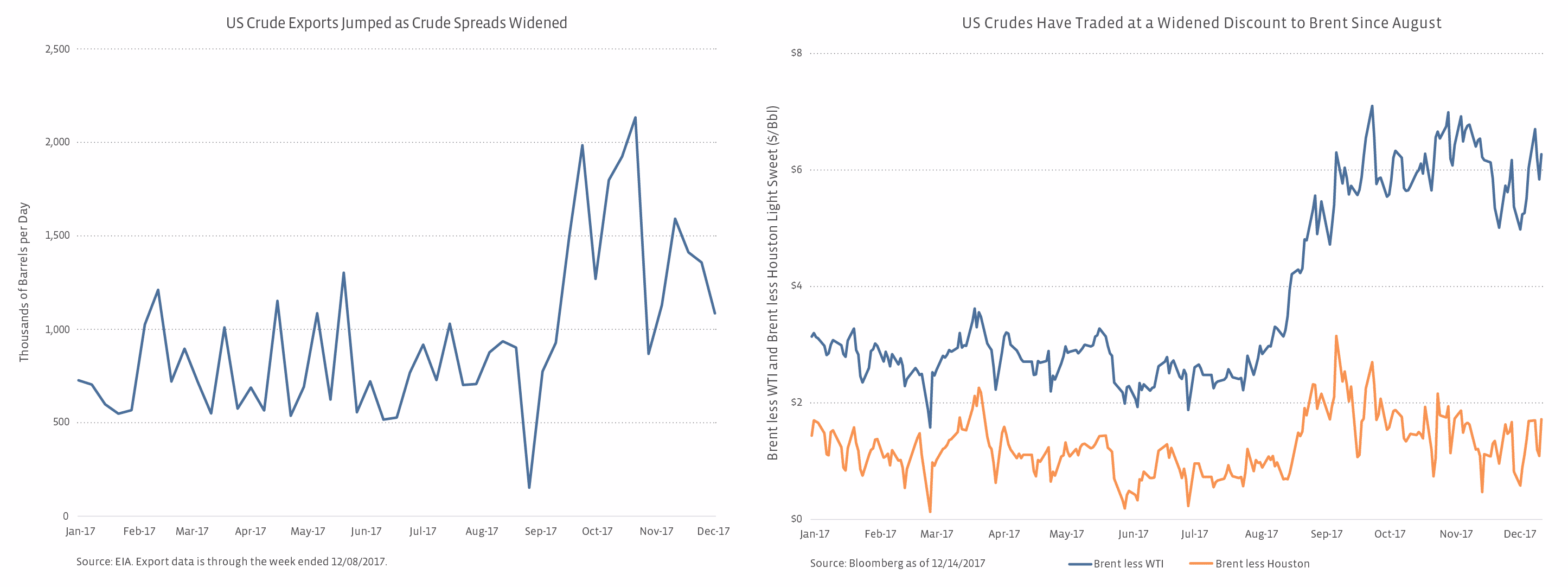

- Crude spreads can incentivize more exports.

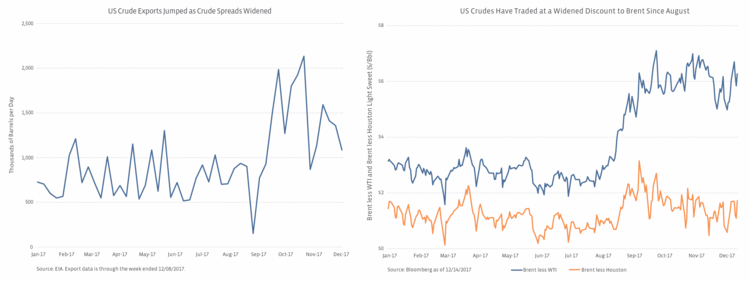

A widened discount in US crude relative to Brent (and other international crude prices) can incentivize more crude exports from the US. As volume-driven businesses, MLPs benefit from increased demand for the pipelines, storage tanks, and marine docks that facilitate crude exports. As you can see from the charts below, US crude exports dramatically increased this fall as the discount in WTI relative to Brent widened and the discount in Houston Light Sweet to Brent also widened. Crude exports reached over two million barrels per day in late October. The spread between Houston Light Sweet and Brent (or the local crude benchmark at the destination) would be the relevant crude spread to compare to shipping rates for moving crude from the Texas Gulf Coast to other parts of the world (Europe, Asia, and elsewhere). While crude exports are primarily driven by the robust production in the US and demand for US crude abroad, widened crude spreads can make US crudes even more attractive for export.

{kind=link}

{kind=link}

{kind=link}

{kind=link}