Summary //

- While a continuation of the Trump administration would be more friendly to oil and gas companies, a potential Biden administration appears manageable for the industry.

- The ability of the president to impact energy infrastructure feels somewhat overstated, particularly with few major interstate pipeline projects currently in the works, though a change in administration could have implications for pipelines in unique situations.

- Even if increased regulations are implemented for energy production or newbuild pipelines under a Biden administration, there could be positive derivative impacts, such as higher commodity prices or an enhanced value proposition for existing pipelines, that help offset potential negatives.

Whether you love election season or hate it, the United States is firmly in the thick of it with the Democratic National Convention last week and Republican National Convention this week. The election has also been in focus for energy investors as a potential change in administration could have implications for the sector. Today’s note discusses the political landscape for energy and the potential impact of a change in the White House for midstream and energy more broadly.

The importance of the president for energy infrastructure (or energy in general) may be overstated.

The ability of the president to impact energy infrastructure feels somewhat overstated. Don’t get us wrong, the president has power and can impact pipeline projects as demonstrated with Keystone XL and the Dakota Access Pipeline (DAPL) during the Obama administration. Frequently, however, the key decision makers for the fate of pipelines or increased drilling regulations can be judges in a federal court or an appeals court. For example, the Trump administration has been supportive of TC Energy’s (TRP) Keystone XL pipeline, but legal and regulatory headwinds have persisted. Recall that very early in his term President Trump welcomed TRP to resubmit its application for a presidential permit, which was denied by the Obama administration in November 2015. The Trump administration approved the pipeline’s permit in March 2017, but the project continues to face permitting challenges. Vice President Biden’s campaign has said that he would revoke Keystone XL’s presidential permit if elected.\

While pipelines within one state are regulated by the state, interstate pipelines are subject to greater oversight. Multiple federal agencies – Department of the Interior, Department of Transportation, US Army Corps of Engineers, Environmental Protection Agency – can have a role in approving interstate pipelines (see this overview of natural gas pipeline permits), and interstate pipelines must comply with applicable laws like the Clean Water Act and Clean Air Act. Keystone XL is one of a few newbuild, interstate pipelines on the drawing board. Many large pipeline projects were completed over the last several years, and other projects have been deferred or cancelled due to moderating US energy production given current commodity prices (read more). There are minimal examples of interstate pipeline projects planned or under construction. Equitrans Midstream’s (ETRN) Mountain Valley Pipeline (MVP) will transport natural gas from West Virginia to southern Virginia upon expected completion in early 2021, and their related MVP Southgate pipeline would transport gas from MVP to North Carolina, with construction expected to start in 2021 and reach completion the same year. With fewer projects underway, the ability of the executive branch to impact infrastructure seems more limited. To the extent permitting for new pipelines is challenged, it should only serve to enhance the value of existing pipelines, which may be candidates for expansion projects in the future.

The unique situation surrounding DAPL bears mentioning given ongoing litigation surrounding the pipeline. It is common for permits to be challenged during construction, but the pipeline has been operational for three years. DAPL is owned and operated by Energy Transfer (ET), with Phillips 66 Partners (PSXP), MPLX (MPLX), and Enbridge (ENB) also owning stakes in DAPL. A court decision upheld the vacating of the pipeline’s easement for Lake Oahe but allowed the pipeline to continue operating. The Army Corps of Engineers is required to outline the options for the pipeline by the end of August. ET expressed confidence on its recent earnings call that an Environmental Impact Statement (EIS) would not be needed, but if ultimately required, the timeline for the EIS could extend into 2021. While not clear cut, a change of administration could potentially have implications for the pipeline, which provides critical takeaway capacity for the Bakken.

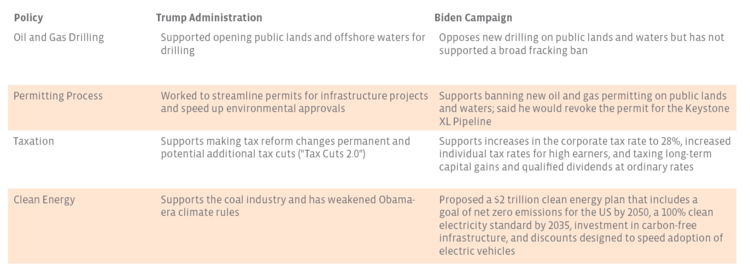

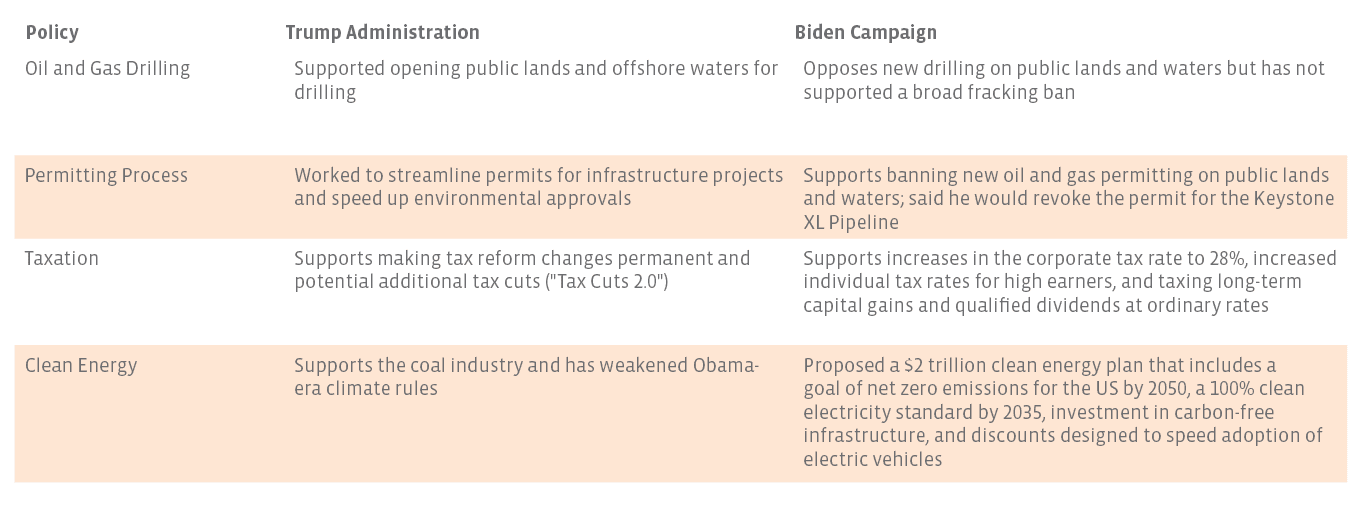

Policy comparison: Trump Administration vs. Biden Campaign Plans

To state the obvious, a Trump administration would likely be more oil and gas friendly than a Biden administration given an emphasis on loosening regulations for the industry and expediting the permitting process for new infrastructure. That said, a Biden administration is more constructive for the energy industry than a Warren or Sanders presidency and appears manageable. Vice President Biden has not supported a nationwide fracking ban or crude export ban, which were some of the more severe measures put forth by his counterparts.

Oil and Gas Activity on Federal Lands: Vice President Biden supports a ban of new oil and gas permits for public lands and waters. As discussed in our piece from last December, an executive order banning new drilling permits on public lands and waters would probably be challenged in the courts. There would also be implications for federal and state revenues, with billions generated from royalties and other fees paid by oil and gas companies. In the meantime, exploration and production companies are stocking up on permits. As discussed on its 2Q call, EOG Resources (EOG) had 2,500 federal permits approved or in the works, which equates to more than four years of drilling opportunities. If drilling activity on federal lands is curbed, operators are likely to shift to private lands. Ultimately, if new or more severe regulations negatively impact US energy production, it could be beneficial for oil and natural gas prices – a potential silver lining for the industry but possibly negative for consumers. With oil prices (and to a lesser extent, natural gas prices) tending to drive sentiment and stock prices for the energy sector, regulations that appear negative for the industry on the surface could be offset by some derivative positive impacts to oil and natural gas prices.

Tax Implications for MLPs vs. C-Corps: Vice President Biden’s tax proposals would widen the tax advantage of MLPs over corporations if implemented, which could have implications for the ongoing MLP vs. C-Corp structure questions in midstream. See more details on the tax implications here. A higher tax rate would have to be weighed against the perceived benefits of the C-Corp structure, namely the potential for broader index inclusion and access to a wider investor base. A common misconception is that the lowering of the corporate tax rate from 35% to 21% (read more) spurred the consolidations and C-Corp roll-ups of MLPs seen over the last few years, but these transactions were largely motivated by a need for simplification or in response to a FERC policy change (read more). The lower tax rate was not a primary reason for the transactions, which were largely consolidations instead of C-Corp conversions. That said, a higher tax rate would be a deterrent for existing MLPs considering changes to their structure. An MLP to C-Corp conversion is very unlikely before the election, and structure questions could be on the backburner for some time as operations take priority in a challenging macro environment. On their 2Q earnings call, management of Enterprise Products Partners (EPD) indicated that they had not spent time this year on an MLP vs. C-Corp analysis, instead focusing on operational execution.

Clean Energy Transition: A potential Biden administration would be more supportive of clean energy and electric vehicle adoption but would likely require cooperation from Congress to bring about change. Even with supportive government policies, an energy transition is still going to take many years. While the goal of net zero emissions for the US by 2050 may seem negative for energy and midstream, it bears noting that midstream corporation Williams Companies (WMB) is aiming to be net zero for carbon emissions by 2050. Though European energy companies have taken the lead on carbon neutrality targets, US companies could increasingly follow suit. That said, as recent rolling blackouts in California have highlighted, the transition to wind and solar energy can result in reliability issues during periods of peak electricity demand if not managed properly. For more information on the energy transition, please see our recent white paper.

Bottom line

With all that is happening in the US today, it is probably safe to assume that energy regulations are not going to be at the top of the list from a policy perspective for whoever wins the election. A change in administration could have implications for some specific pipelines, but overall, the potential impact appears limited given a lack of newbuild projects currently underway. Executive orders are likely to be challenged in the courts, and more meaningful changes in energy policy likely require Congress to act. Even if increased regulations are implemented for energy production or newbuild pipelines, there could be positive derivative impacts, such as higher commodity prices or an enhanced value proposition for existing pipelines, that help offset potential negatives.

{kind=link}