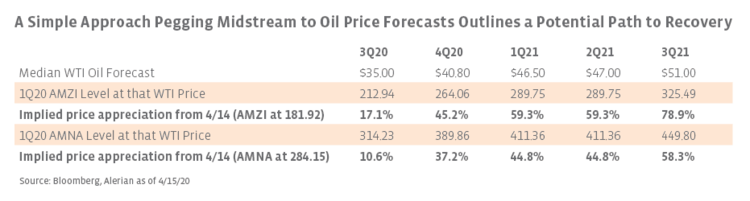

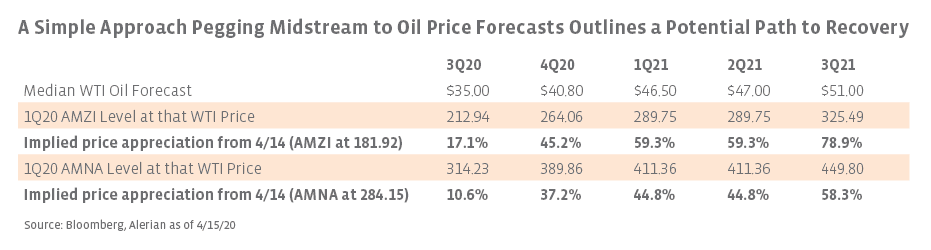

What do Oil Price Forecasts Suggest for a Midstream and MLP Recovery?

When a sell-off occurs, the question on everyone’s mind turns to when things will recover. Tuesday’s research note addressed this question by looking at past drawdowns and recoveries, while today’s note takes another approach using oil price projections. Of course, no one has a crystal ball for future oil prices or midstream equity values, but there are plenty of banks and firms that forecast oil prices, which can be used to forecast midstream equity values. The table below utilizes the median WTI oil price forecast from Bloomberg as of yesterday for the next five quarters as a basis for the potential improvement in midstream. Oil price projections are almost never correct. Who forecasted in January that WTI would be below $20 per barrel (bbl) in April? That said, oil price projections are a good indication of what the market is anticipating for future prices and can be useful when viewed through that lens.

Having acknowledged the weaknesses of oil price projections, this simple analysis is meant to provide some framework to answer the question of when things may recover. For added context, year-to-date through April 14, WTI oil prices are down 67.1%, the Alerian MLP Infrastructure Index (AMZI) is down 51.1%, and Alerian Midstream Energy Index (AMNA) is down 40.1%. The table below includes index values for the AMZI and the broader AMNA that correspond to the oil price forecast. For example, on March 10, WTI closed at $34.36/bbl. On that same day, the AMZI and AMNA closed at 212.94 and 314.23, respectively. If oil prices recovered to $35/bbl in 3Q20 as forecasted and the midstream indexes rebounded to their last price when oil was near $35/bbl, then the implied gain for the AMZI and AMNA indexes from April 14 would be 17.1% and 10.6%, respectively. Similarly, if WTI crude recovered to $51/bbl and the midstream indexes reverted to their value when WTI was at $51/bbl in February, the indexes would have largely recovered from the dismal performance in March. Admittedly, many things would have to fall perfectly into place for that to materialize. Clearly, the oil price is not the only factor that determines midstream equity values, and there is nothing pegging these indexes to past levels at various oil prices. While this analysis lacks sophistication, it is useful as one way to frame a potential midstream recovery while incorporating market expectations for oil prices.

{kind=link}