For football fans across the country, September is perceived as a fresh start. Every team has an untarnished record, and the hope that greatness lies ahead permeates the dreams of enthusiasts from coast to coast. In much the same way, as we return from our August vacations and financial markets get back into the swing of things, we have high hopes for a strong quarter. Just like the Philadelphia Eagles and San Diego Chargers, TC Pipelines (TCP) and Energy Transfer Partners (ETP) enjoyed a month of success, gaining 15.5% and 11.4%, respectively.

TCP is the MLP subsidiary of TransCanada (TRP), a Canadian pipeline and power company. TCP jumped 15.4% on September 19th on news that activist investors were assessing interest in splitting the company into a pure pipeline company and a pure power company, a move bearing strong resemblance to what NiSource (NI) announced during their analyst day on September 29th. Of course, rumors are just that; all activist sources remain unnamed and TRP management has issued a press release indicating its faith in the current structure.

The Energy Transfer family of companies announced a lot of news on September 25th, the highlight being that Susser Petroleum Partners (SUSP) will begin receiving dropdowns from ETP. SUSP will also change its name and ticker to Sunoco LP and SUN, respectively. This may cause confusion as Sunoco Logistics Partners (SXL) is also a part of the Energy Transfer family. We look forward to seeing the latest iteration of the org chart at their analyst day next month.

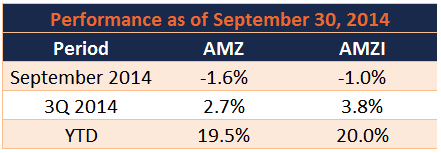

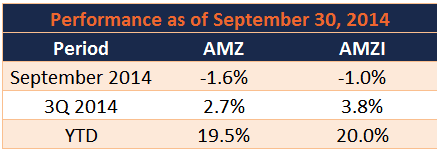

We can’t entirely avoid the hand-wringing of the broader energy MLP market, though, as the Alerian MLP Index (AMZ) fell 1.6% and the Alerian MLP Infrastructure Index (AMZI) fell 1.0% during the month.

Robust production coupled with a slowdown in global economic activity caused global crude prices to drop sharply. While most MLPs have limited direct exposure to commodity price fluctuations, a prolonged period of weakness in crude oil prices could reduce upstream activity and impact throughput on energy infrastructure assets accordingly.

Hi-Crush Partners (HCLP) was the worst performer in the AMZ during September, trading down 25.4%. Given the stock’s strong performance year to date, weakness was likely due to profit taking as the company continued to announce good news in the form of additional long-term contracts with producers.

Natural Resource Partners (NRP) fell steadily throughout the month, losing a total of 17.9%. Other index constituents with losses greater than 10% for the month were EV Energy Partners (EVEP), Alliance Resource Partners (ARLP), BreitBurn Energy Partners (BBEP), and QR Energy (QRE). All of these companies belong to either the Exploration & Production or Coal and Mineral subsectors, which are traditionally more sensitive to fluctuations in commodity prices.

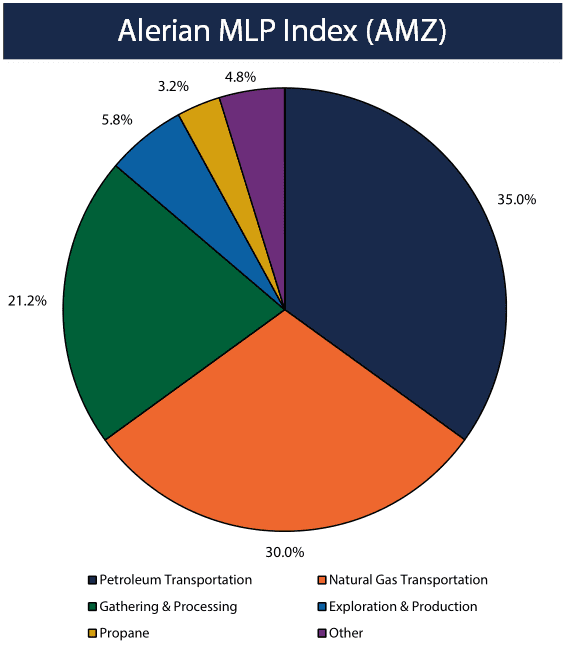

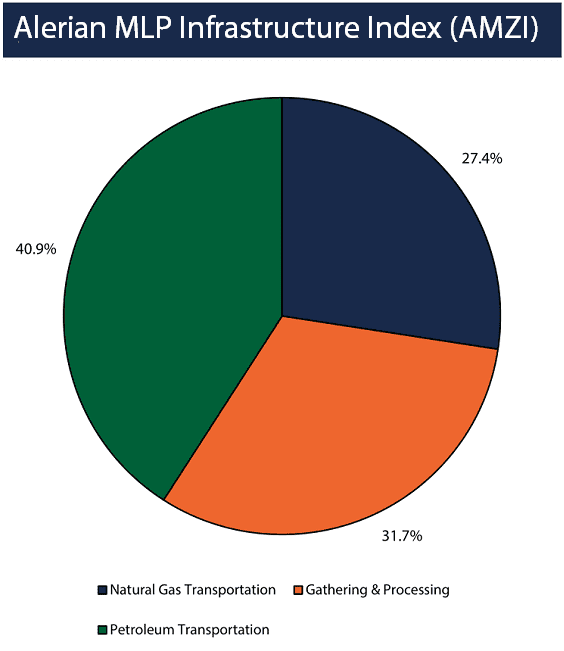

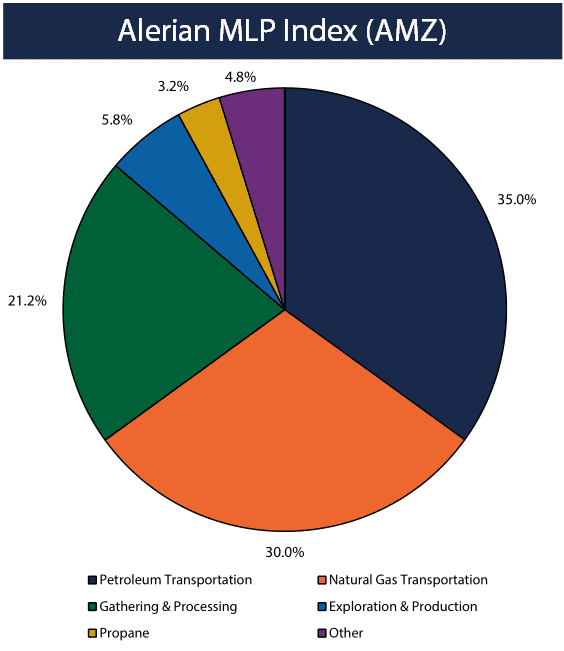

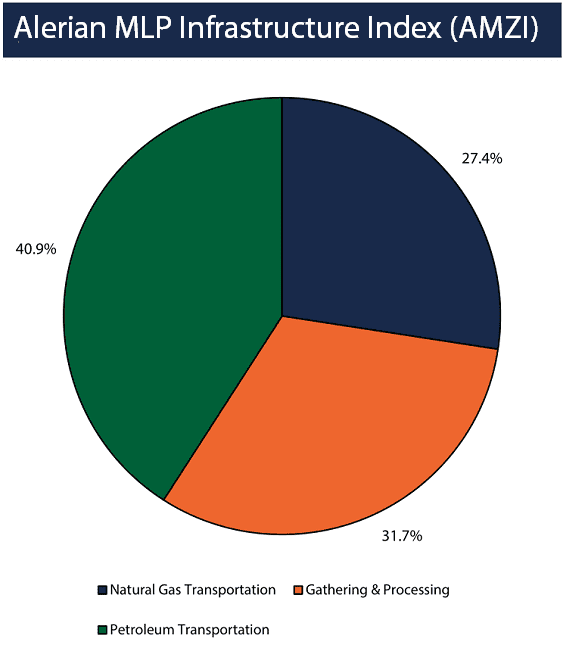

To see the split of subsectors of the various Alerian Indices, we show a pie chart updated every quarter on our factsheets. Those charts are replicated here:

{kind=link}

{kind=link}

{kind=link}