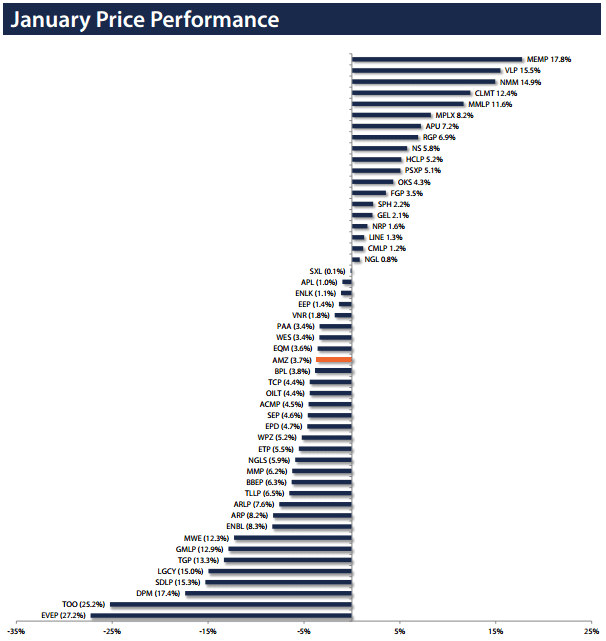

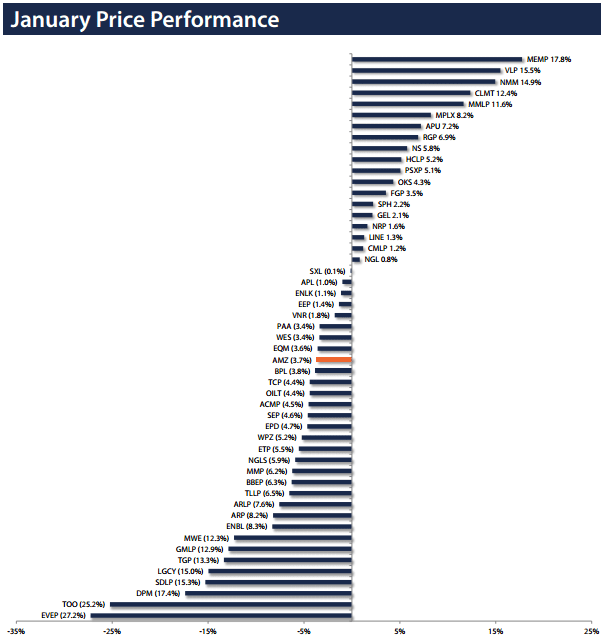

January was another one of those months where diversification really shined. The return differential between the best and worst AMZ performers, MEMP and EV Energy Partners (EVEP), respectively, was 45.0%. Since they’re both upstream names, it’s hard to blame the AMZ’s 3.1% loss on a total return basis on subsector performance. The Alerian MLP Equal Weight Index (AMZE) lost about half as much as the AMZ, suggesting that smaller names generally had a better January than large caps. As an example, Enterprise Products Partners (EPD), the largest constituent in the AMZ, lost 4.7% in January. But the top and bottom five performers represented 1.3% and 2.8% of the AMZ, respectively, so size wasn’t (and isn’t) everything.

Unless, of course, we’re talking about M&A activity. Larger, diversified, investment-grade companies tend to have the balance sheet flexibility to acquire assets at discounted prices in times of market turmoil. Kinder Morgan (KMI) CEO Rich Kinder, who in August described the MLP market as “a fertile field to do a little grazing in,” put the proof in his pudding by announcing the acquisition of Hiland Partners and establishing a strong midstream position in the Bakken by doing so. Plains All American Pipeline (PAA) announced that it added a $1 billion 364-day credit facility. The move from $2.6 billion of liquidity to $3.6 billion has primed the pumps with capital, just in case a good acquisition opportunity comes management’s way.

Just to close with a bit of gossip, Sandell Asset Management wrote an open letter to SemGroup (SEMG), encouraging the company to sell itself. Sandell hoped SEMG would turn subsidiary Rose Rock Midstream (RRMS) into a dropdown story so that SEMG would trade at pure-play GP multiples. As SEMG CEO Carlin Conner is not moving in that direction, or at least not at the pace or with the clarity that Sandell would like, the event-driven asset manager believes a sale would be more effective in maximizing shareholder value. The press release containing the letter goes so far as to list potential buyers: EPD, KMI, Magellan Midstream Partners (MMP), PAA, Spectra Energy Corporation (SE), and Sunoco Logistics Partners (SXL). When SEMG management responded, it basically said that the company is on track as a dropdown story, and that they’ve done some great things under Conner, who took over as CEO in April 2014. However, the Sandell letter pushed the stock up more than 8% on the day of release, and two weeks later, the company announced that RRMS would be acquiring all remaining SEMG crude oil assets.

{kind=link}