Kanye West is $53 million in debt, and Kim Kardashian (incredible business woman and also Kanye’s wife) has been photographed in a very expensive children’s store. Now, personally, I have a lot of respect for anyone in eight figure debt, because that is way beyond credit card and brand new car debt—that’s the level of debt only a person worth investing in can accrue. However, the public outcry over the cost of their children’s clothes (which is none of our business anyway) shows how phenomenally intolerant we are as a society to people spending money that isn’t in their bank account.

With MLPs, they are only spending the money they have, and while investors may approve now, it could lead to problems down the road.

Some history: two years ago, investors were clamoring for MLPs to have high growth capex budgets; the more opportunities an MLP identified, and the faster they could build projects and close deals, the better. Now, the tide has changed and investors are concerned about whether producers will drill enough to justify new pipelines. While G&P MLPs have already been transitioning to just-in-time build models for years, the most common (and best rewarded by investors) method of adjusting to delayed production and increased financing costs now is reducing growth spending in the near term. MLPs are delaying and cancelling projects where possible. Energy Transfer Partners (ETP) identified $750 million of growth capex reductions for 2016, a reduction of 15% which eliminates their need to raise equity in 2016. Williams Partners (WPZ) reduced their 2016 capex budget dramatically: eliminating more than $1 billion or 32% of the previous budget. Enable Midstream Partners (ENBL) has also delayed projects, allowing it to reduce growth spending by $375 million or 66%, and reducing its need to issue common equity.

This is a bit circular, but if a company is spending less money, it needs to raise less money. Likewise, if capital is difficult to raise, there is less money available to be spent. Since MLPs pay out nearly all incoming cash flow to investors in the form of distributions, in order to finance growth, they must raise capital elsewhere. Typically, this has meant the debt and equity markets. Unit prices are cut in half making equity prohibitively expensive. Without raising equity, only a certain amount of debt can be used before leverage ratios creep too high. So, in addition to investors rewarding those that have reduced capex budgets, they’re rewarding those that have the financing in place for their reduced capex. Sometimes, that has come in the form of alternative financing, like Plains All American Pipeline (PAA)’s upsized $1.6 billion 8% perpetual convertible preferred units issued in January. The company now anticipates that it will not need to raise capital again until 2017.

A company that will not need to raise capital for the next 12 or 18 months has all the money it needs for that period. However, a company that announces it has satisfied all equity financing needs for a given year may still need more capital. This may come in many forms: a DRIP program, ATM offerings, revolving line of credit, or issuing traditional debt in the form of notes. For many of the larger MLPs, their investment grade rating means that traditional debt financing is still available, albeit at higher rates. Transcontinental Gas Pipe Line Company, a subsidiary of WPZ, issued $1 billion of notes at 7.85% in January. Relative to non-energy investment grade companies, that rate is exceptionally high as credit spreads for energy companies continue to remain wide. Previously that month, both Moody’s and Fitch had downgraded WPZ to the lowest investment grade rating possible (Baa3 and BBB-, respectively). The following week, S&P also downgraded WPZ to the last investment grade rating, BBB-.

WPZ isn’t the only company dealing with downgrades. ENBL had its BBB- rating from S&P reaffirmed, but also placed on negative outlook. As we’ve discussed before, rating changes tend to be lagging indicators, based in part on how low unit prices make equity growth financing difficult.

This is a harsh cycle where companies that are already struggling are punished even further. Low equity prices mean that they may turn to debt financing, but debt ratings (and therefore financing rates) can be affected by equity prices. ENBL’s low unit price was specifically cited by S&P as a reason for the change, as “challenging capital market conditions could make it difficult to issue equity to keep financial leverage” below a trigger threshold. Even if the cost of note issuance remained low, leverage ratios limit the amount of debt a company is willing to take on. So, companies must reduce growth capital spending to stay within their means. On the surface, this appears to make sound financial sense: don’t spend money you don’t have. However, pursuing fewer growth opportunities will translate into lower growth. MLPs aren’t trying to run up figurative credit card debt; they’re trying to finance real cash flow generating assets. Before these assets are financed and built, future cash flows are determined by signed, committed contracts.

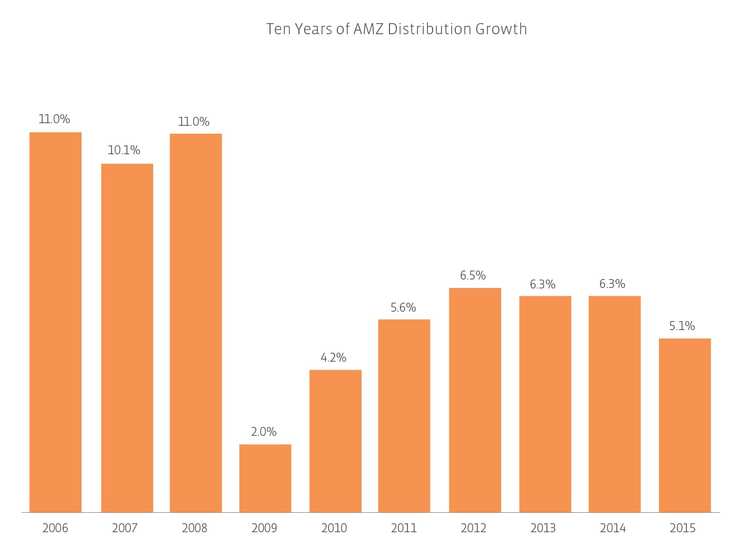

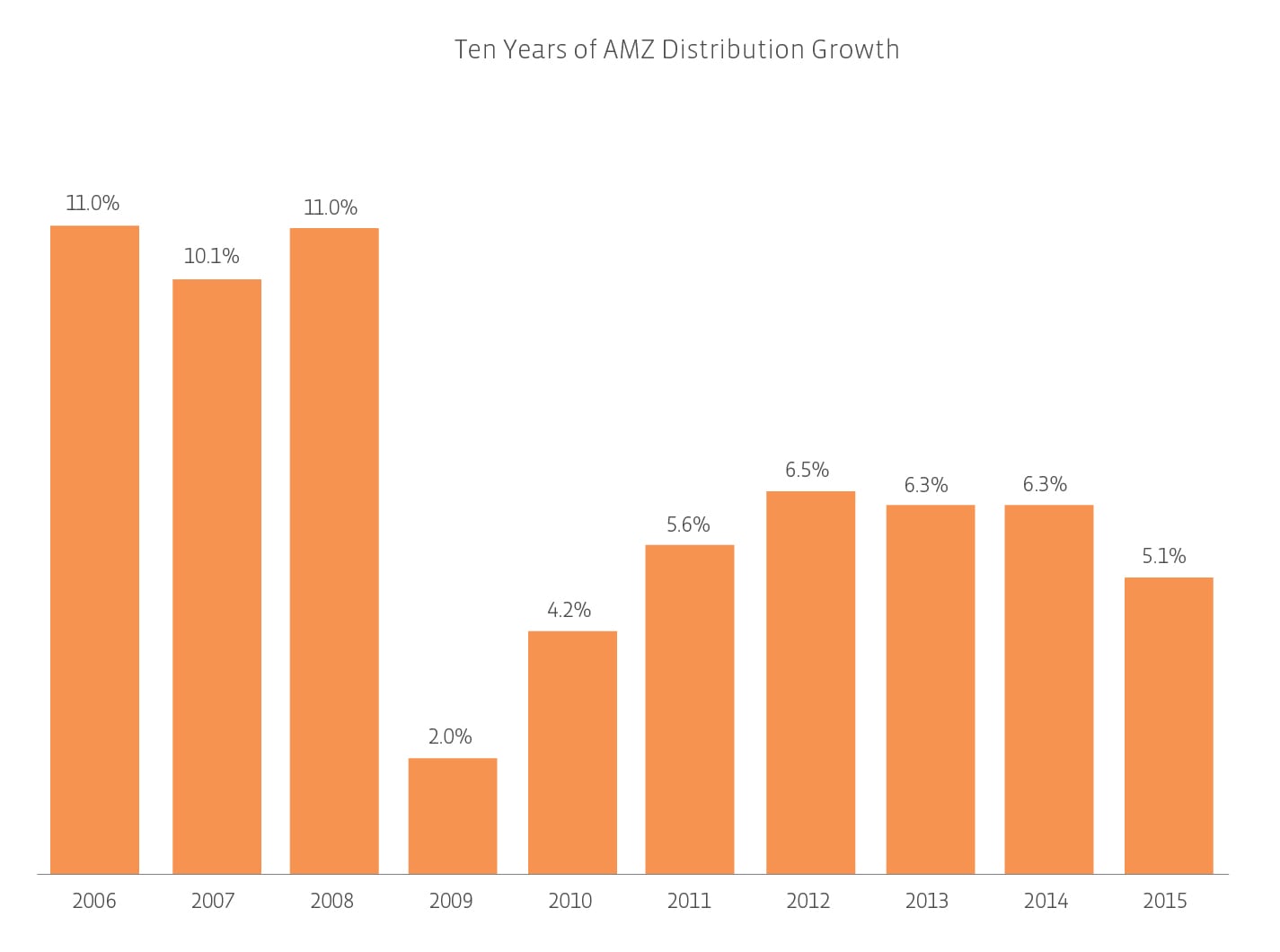

If capital markets access remains limited and companies are forced to operate on shoestring growth capex budgets, the 6.8% annualized distribution growth rate that MLPs have enjoyed over the last ten years will necessarily have to fall. In 2015, despite unit prices falling more than 30%, distributions rose 5.1%. (We saw similarly lowered distribution growth in 2009 when distributions grew by only 2% after a period when capital markets were closed for two years.)

The only silver lining is that previously uneducated MLP investors have either exited the space (as they had no idea what was happening, and reasonably should not own investments they don’t understand), or they have received a crash-course in MLP risk factors: as equities, they will experience volatility; capital markets access is crucial to growth; and debt ratings indirectly affect equity prices in the same way dramatic changes in oil prices indirectly impact midstream MLPs.

{kind=link}