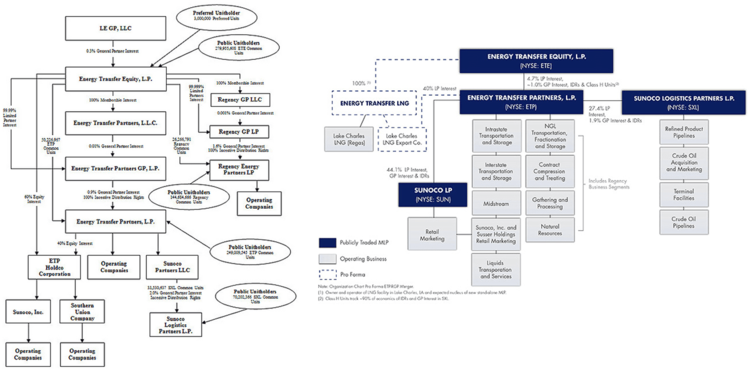

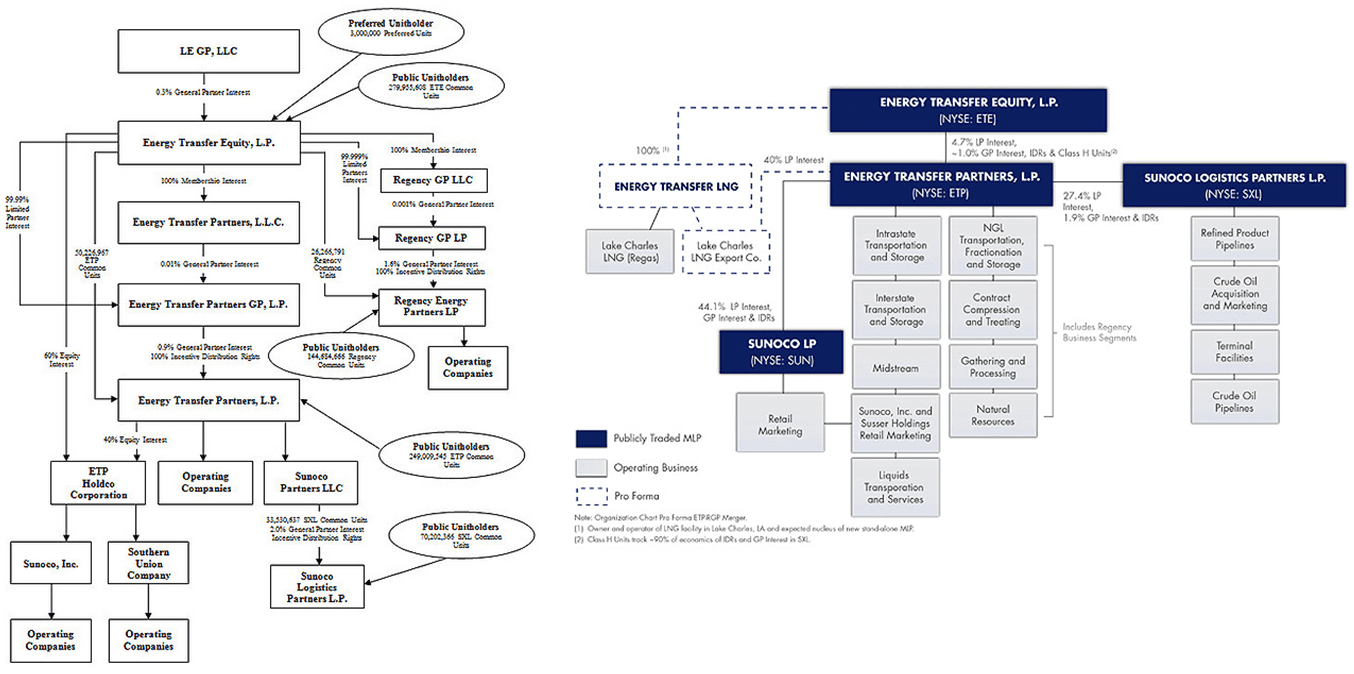

Adding to the horse argument, Energy Transfer Equity (ETE), the GP of them all, is itself an MLP, not a C corporation. Management has discussed potentially using C corporation currency in the future, but a complete conversion would impose a hefty tax bill on Chairman and CEO Kelcy Warren.

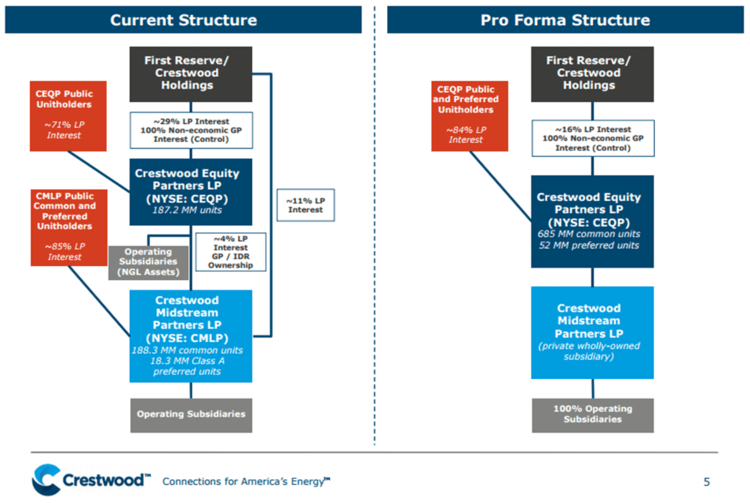

That’s one reason many MLP investors prefer to invest in the GP—they feel that investing alongside management is the better choice, even given the risk inherent in leveraged exposure to the LP. However, that pair trade does not always work out, as Crestwood demonstrated this month (and year).

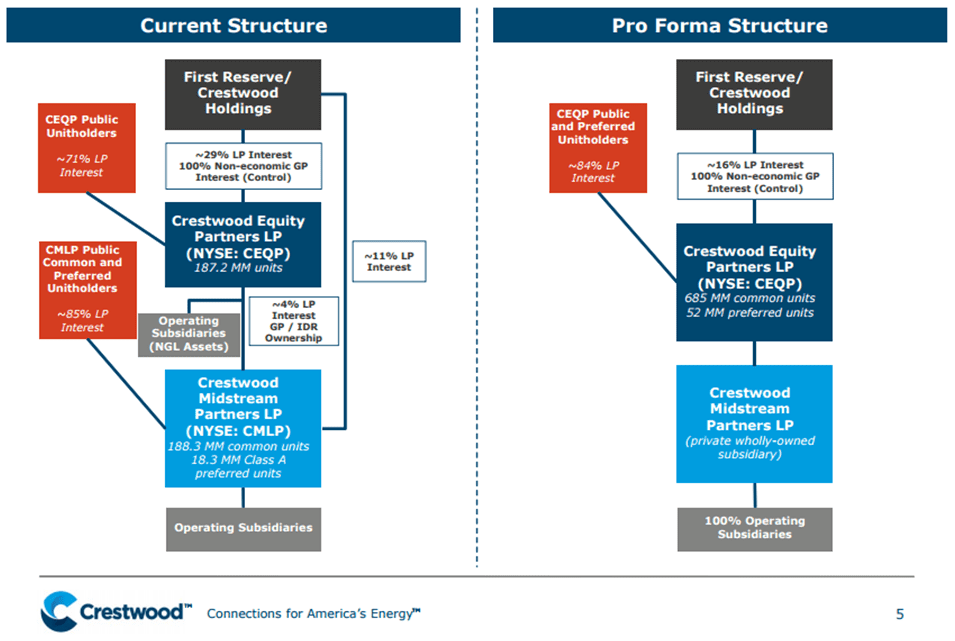

Like WMB pre-transaction, Crestwood Equity Partners (CEQP) was moving towards being the pure-play GP of Crestwood Midstream Partners (CMLP) until they announced a merger in early May. Unlike previous GP/LP mergers where the LP was the surviving entity, CEQP will be the stock that continues trading after the transaction closes. On the date of the announcement, CMLP fell 4.3%, but CEQP fell 17.9% . Investors expected a much better deal, perhaps something with an outside company (a la Crosstex + Devon Energy (DVN) à EnLink).

Analysts previously warned that CEQP may not have been able to maintain its distribution with sub-1.0x coverage. Post-merger, CEQP will be able to maintain the distribution at 1.05x coverage. Based on the conversion rate and current distribution levels, current CMLP unitholders will receive 7.7% less cash each quarter after the transaction closes.

Barring the inevitable lawsuits, what’s done is done. At 1.05x coverage for the new entity, even a successful lawsuit couldn’t do more than line lawyers’ pockets. Moving on, Crestwood benefits from the elimination of its IDRs, lowering its cost of capital. There is also the reduced administration costs and the psychological benefit of a simplified organization, as IDR-less MLPs often note in their marketing materials. Still, despite all the grumbling, no one has complained about Crestwood’s use of the MLP structure.

Just as the KMI and WMB transactions aren’t an indictment of the MLP structure, Crestwood’s decision to no longer have a publicly traded GP isn’t an indictment of publicly traded GPs. In May, both Tallgrass Energy GP (TEGP) and EQT GP Holdings (EQGP) completed their IPOs. TEGP is the pure-play general partner of Tallgrass Energy Partners (TEP). Like EnLink Midstream LLC (ENLC) and Plains GP Holdings (PAGP), it’s elected to be treated as a C corporation for tax purposes, so investors will receive a Form 1099 instead of a Schedule K-1. The company priced 41.5 million units at $29, raising $1.2 billion, the second-largest deal in the history of MLP IPOs. It traded up 9.5% on its first day, and closed the month up 10.5%.

EQGP is an MLP GP and structured and taxed similarly to Western Gas Equity (WGP). Both GPs have E&P parents—EQT Corporation (EQT) in the case of EQGP and Anadarko Petroleum (APC) in the case of WGP. EQGP offers investors the ability to own the GP of EQT Midstream (EQM) without the direct commodity price exposure of EQT. EQGP priced 23 million units at $27, raising $620 million. Based on an expected initial quarterly distribution of $0.09175, EQGP priced at a 1.4% yield and ended its first day of trading at a 1.1% yield after closing at $32.92. Clearly, investors are still eager to participate in GPs.

As of the end of May, there were 122 publicly traded energy MLPs with a total market capitalization of $483 billion. That is a whole herd of horses. When you hear news of the next MLP transaction, there’s always a chance that it’s a zebra, but it’s probably a horse. And (because this is my article and I can extend the metaphor as far as I want), this herd still has plenty of room to run.

{kind=link}

{kind=link}