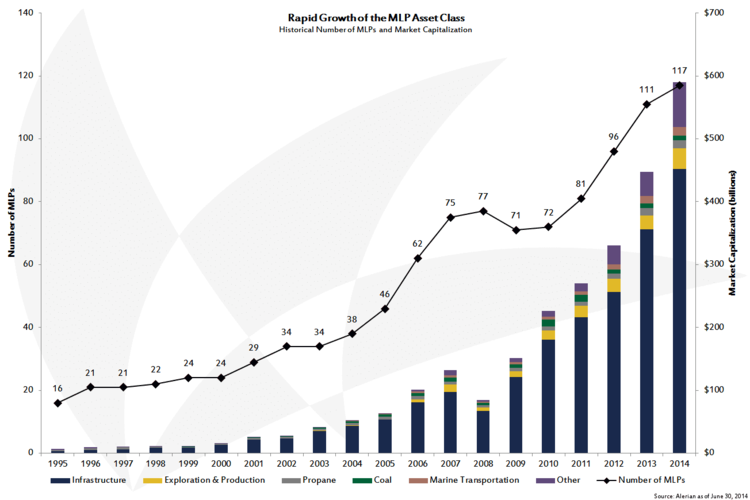

Did you know Alerian was founded over ten years ago? That makes me feel old as an employee, but it’s also pretty incredible to watch how this asset class has grown. As I look back over the past six months, I don’t see a scrappy little emerging asset class, I see something considerably more mature: fewer temper tantrums, an ability to play in at least the minor leagues (Triple-A of course) and be taken seriously, and a credit score reflective of increased responsibility.

While integrated oil companies and energy producers have been willing to sell assets to MLPs for many years, in 2014 we’ve seen them actively pursue the structure as the natural home for their midstream assets. In March, Devon Energy (DVN) combined its midstream assets with the Crosstex family of companies, forming EnLink Midstream Partners (ENLK) and EnLink Midstream LLC (ENLC). Last summer, Devon had considered creating their own MLP and even filed an S-1, but by combining with Crosstex instead, they were able to reach the market much faster. The combination also enables Devon to focus capital spending on expanding its oil interests in the Eagle Ford Shale, Permian Basin, and Eastern Alberta while allowing EnLink to spend the dollars necessary to build and operate the supporting midstream infrastructure. EnLink benefits from the predictable customer base that Devon provides, as well as the premium investors are giving to companies with visible dropdown potential.

Shell (RDS) also filed an S-1 in June to create an MLP, which is expected to come to market in the second half of the year. Given Shell’s size (it will be the largest corporate sponsor of an MLP), it wouldn’t have considered creating another publicly traded security if the potential valuation arbitrage wasn’t big enough. This filing will likely drive other large energy companies with MLP-qualifying assets to at least consider creating their own MLPs.

MLPs used to be considered an alternative asset class, but as I hope it is clear by now, that statement has become less and less true. With the rise in popularity, however, has come an increase in correlations. In July, the broader market was down, utilities were down, energy was down, and MLPs were down. The Labor Department released a strong jobs report, which is seen as a sign of an improving economy. However, fears over the Federal Reserve possibly raising interest rates overshadowed the improving employment situation. At first blush, MLPs decline along with other yield-oriented equities when reports (or rumors) spread of a potential rise in interest rates. However, historically, during periods of steadily rising rates, MLPs have positively differentiated themselves from the broader market. This is due to the growth component of MLP total return, often anchored by inflation-based escalators in the rates they charge for using their assets.

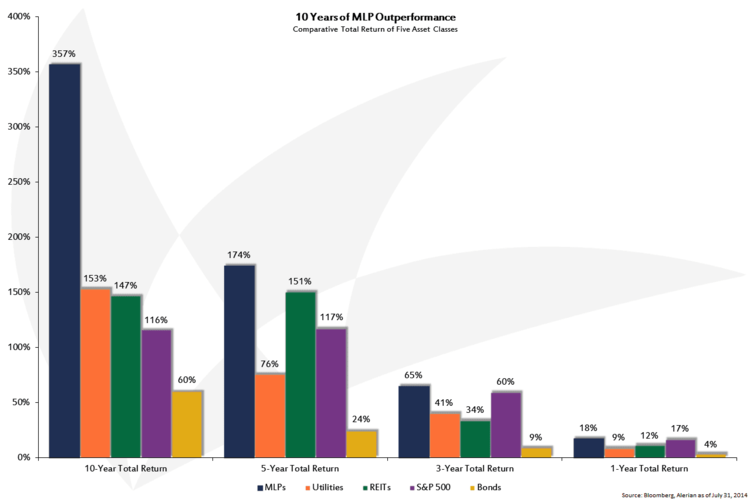

Some investors place MLPs in their real asset sleeve while others use them for income. Regardless of the investor motivation, remarkable amounts of capital have entered the space in recent years. Add to that MLP distribution growth in the high single digits, and generally positive fundamental news from earnings reports, and the historical outperformance against the S&P 500 is very understandable.

At this point, however, no one but the most bullish of the bulls would argue that MLPs are undervalued. As MLPs have become a standard part of many model portfolios, they have already seen a revaluation due to increased fund flows. But the underlying fundamentals and growth prospects remain in place. The amount of money and assets necessary to satisfactorily build out North American energy infrastructure over the next several decades was revised in March. The Interstate Natural Gas Association of America (INGAA), which produced this study, previously had estimated that $10 billion of energy infrastructure investment would be needed per year. That number is now $30 billion. Shale plays and new drilling technologies have changed the worries about peak oil to excitement about the US energy renaissance. This growth underpins the growth of midstream infrastructure. Despite the maturity and current valuations, it is this potential that has prevented the enthusiasm from flat-lining.

Along with that idea, in June, the Department of Commerce permitted Enterprise Products Partners (EPD) and Pioneer (PXD) to export minimally refined condensate. EPD has already shipped its first cargo. Due to the limited nature of the ruling, it’s a marginal positive for MLPs who own crude oil storage along the Gulf Coast, as well as for those MLPs exposed to the Eagle Ford (which is producing a great deal of condensate). However, the real impact of this ruling will be determined by whether this is viewed as a trial run and is a precursor to an eventual lifting or revising of the US crude export ban.

At Alerian, we don’t know what’s in store the next 10 years for Master Limited Partnerships. By then, despite our own gray hairs, we expect to see the asset class continue to establish itself as part of the financial community. Those gangly teenage years are coming to an end, and while there may still be some growing pains ahead, we look forward to seeing the asset class continue to mature.

{kind=link}

{kind=link}