Did you think this October was the scariest October yet? (You’d be wrong about that—2008 was worse. How quickly we forget.) Now that the panic has mostly passed, consensus has shifted back to the traditional “long-term play on the US energy renaissance,” “commodity price agnostic,” and “toll road business model” MLP and energy infrastructure story. Regardless of what actually happened, this past month was a reminder that MLPs are still equities, and, like all at-risk investments, they are subject to investors’ whims, emotions, and biases.

At Alerian, we spent a great portion of October addressing rumors about the moves in the MLP space. To quickly recap that for you:

Are MLPs more sensitive to commodity prices than we previously thought?

No, fundamentals and business models are still intact, as assets contracted on a capacity reservation or fee basis are neutral to short-term commodity price fluctuations. That said, a sustained move in commodity prices in either direction can adversely impact energy infrastructure assets through lower supply volumes, demand destruction, and/or the risk of recontracting at lower rates.

Is there a hedge fund deleveraging in the space?

While technically possible, we could not unearth anything to substantiate this rumor.

Is Kinder the first domino to fall in the conversion of the MLP space to C Corporations?

No. For the hundredth time. Moving the needle on a $100 billion enterprise is different.

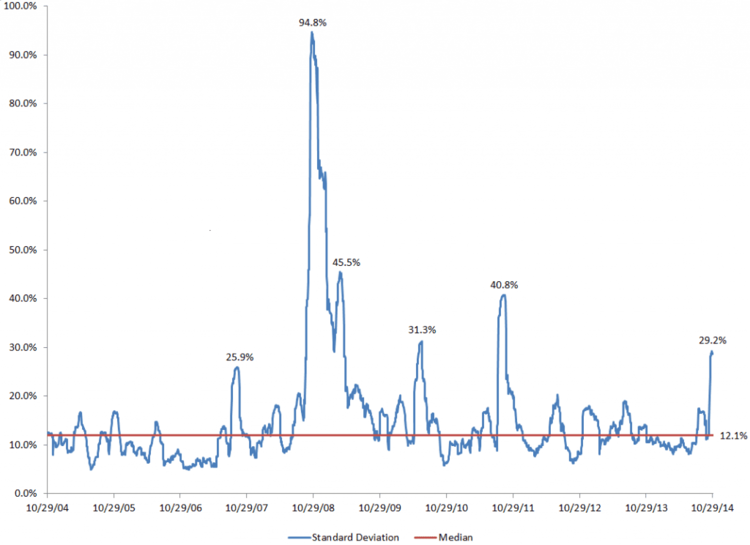

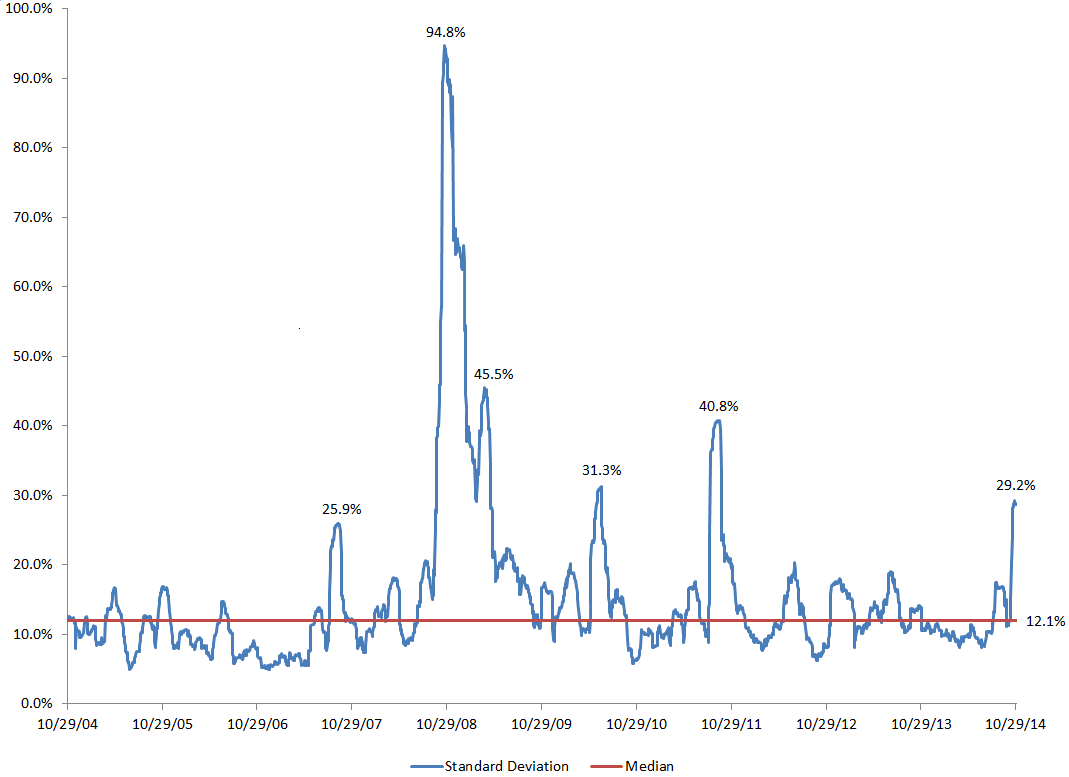

Volatility spiked during the month. Within the course of a week (October 8-16), standard deviation increased to 28.2% from 12.1% on a rolling 30-day basis. We’ve only seen volatility that high during three other periods in the past ten years: the financial crisis in 2008 (94.8%), when the market worked through fears of a double dip in June 2010 (31.3%), and during the European sovereign debt crisis in August 2011 (40.8%). The commonality in each of these periods (including October 2014) is broader market fear, generally unrelated to MLP fundamentals. The financial crisis was the exception: dramatic commodity prices changes, shifting demand for refined products, and lack of financing were all rational concerns during this period.

Rolling 30-day standard deviation of the AMZX over the past 10 years.

But let’s get down to brass tacks—what actually happened. The unifying theme for October involves hard data supporting MLP consolidation, the recognition of the value of the MLP asset class by the broader energy industry, and growth stemming from the North American energy renaissance.

First, MLP consolidation continues beyond Kinder. (By the way, Kinder set the date for the merger vote on November 20th. Mark your calendars.) Targa Resources Corp (TRGP) and Targa Resources Partners (NGLS) agreed to buy Atlas Energy (ATLS) and Atlas Pipeline Partners (APL), consolidating both companies’ Permian Basin and Gulf Coast gathering and processing assets. And Enterprise Products Partners (EPD) agreed to buy the general partner of Oiltanking Partners (OILT) and proposed a merger with OILT, enhancing EPD’s Gulf Coast presence.

If some MLPs are going away, they are being replaced by new IPOs. USD Partners (USDP) priced at $17 on October 8th. This rail terminal MLP is the first of its kind as a pure rail play. However, it has been trading below its offering price.

On September 29th, Dominion Resources (D) received final approval from the Federal Energy Regulatory Commission (FERC) for its Cove Point LNG export facility in Maryland. Following the approval, Dominion moved forward with the IPO of its MLP, Dominion Midstream Partners (DM), which owns a preferred interest in the facility as currently configured for imports/regasification. DM priced at $21 on October 14th and has traded into the $30s this week.

Perhaps of greatest consequence this month was Shell’s MLP deal, marking the first utilization of the structure by an integrated oil major. While the market expected demand for the offering to be strong, no one expected it to be this strong. Shell Midstream Partners (SHLX) priced an upsized deal at $23 on October 28th, above the expected range. On the first day of trading, SHLX traded up to $33.55, a 45.9% first-day return. It was the largest MLP IPO in history, and at current prices, it has a market capitalization of $4.4 billion, making it the 29th largest MLP.

Perhaps rather than making a comparison to Halloween, Thanksgiving, or autumn this month, it would be more appropriate to think about lucky kids on Christmas. Upon hearing from their friends that MLPs weren’t the cool investment due to their association with oil, some investors left the space. Savvier kids took advantage of the great deals offered by fickle disinterest at that time. When the shiny new investment appeared in store windows, everyone was very quick to jump on board.

{kind=link}