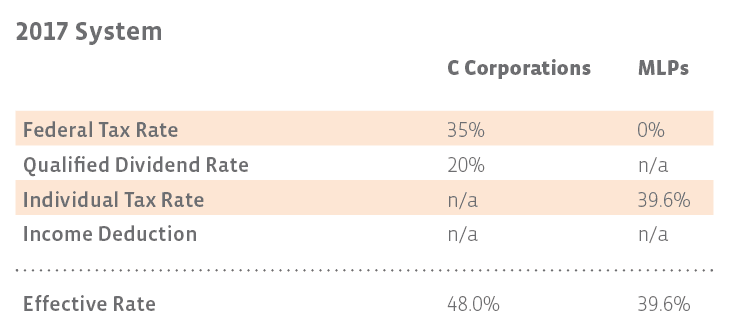

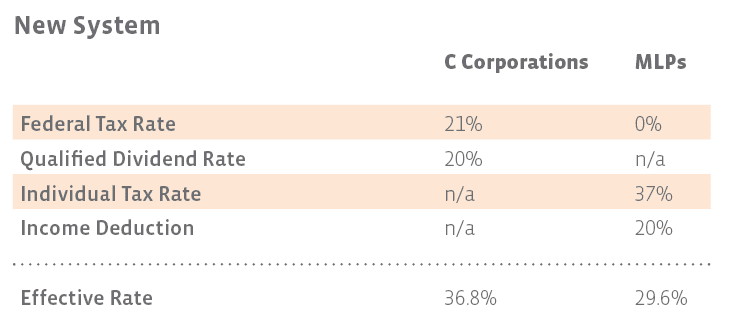

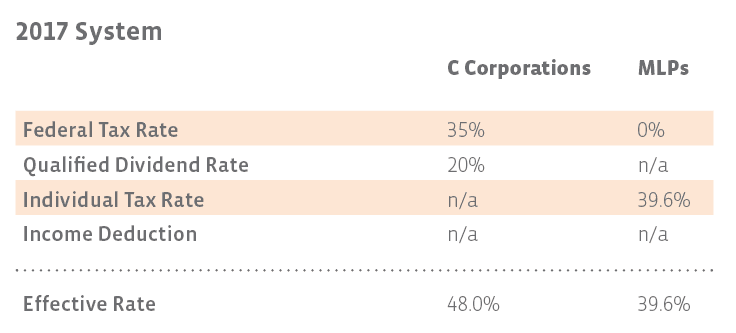

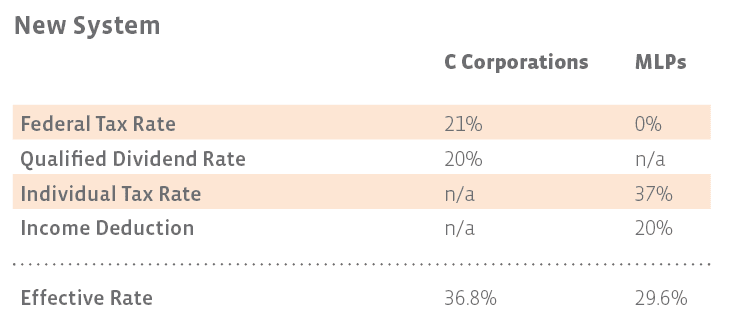

Tax advantage of the MLP structure: 7.2%

While the overall tax benefit to using the MLP structure has decreased from 8.4% to 7.2%, the costs of investing in MLPs remain the same: namely, filing schedule K-1s. This creates an additional accounting burden on the end investor and shrinks the pool of investors willing to invest, which hurts the company. Additionally, since partnerships are not included in the S&P 500, there are billions in linked assets that MLPs cannot access.

Result:

The tax advantage of organizing as an MLP remains, but the benefit is not quite as big as it used to be. Existing MLPs are unlikely to be tempted to change structures. While it might grant access to a larger pool of investors, it could potentially trigger an enormous tax bill for existing investors (a few of whom are in management positions). However, new companies thinking about becoming public may now have less incentive to use the MLP structure. The number of MLP IPOs may be fewer in the coming years than in past years.

Bonus Depreciation:

Under the old model, MLPs (and other companies) could immediately depreciate 50% of the value of property. This will be increased to 100% for property placed into service in the next five years. After the five-year period, the bonus depreciation percentage is gradually phased down for properties placed into service during the years 2023 – 2026. Plus, the company doesn’t even have to build the asset itself to take advantage. The bonus depreciation is available even for acquired property, as long as it’s the company’s first time using it. Notably, this bonus is not available to utilities.

Result:

While MLPs are always prolific builders of assets, they only very rarely speculatively build assets, so the likelihood of this change resulting in an overbuild of energy infrastructure is small. More likely, this change will enhance the project viability math, and projects that were previously only modestly profitable (or break even) might get built.

Interest Expense Deduction Limitation

Previously, large businesses, including MLPs, were able to fully deduct interest expense. Beginning in 2018, interest expense deductibility is now capped at 30% of adjusted taxable income. The limitation does not apply to Utilities, which will be able to deduct 100% of interest expense.

Result:

If the deduction proves to be more than the 30% limitation, it can be carried forward to future years (essentially lowering the cost basis). If the company is sold in the meantime, the deduction can be added back to the basis, so essentially, you never miss out on it.

Repeal of Technical Termination

These rules were a bit esoteric to start with. If 50% or more of a partnership was sold or exchanged, the publicly traded partnership (aka the MLP) would be treated as newly formed. This produced a very minor risk. After all, MLP units do trade in the open market, so there was always a possibility of triggering this rule.

Result:

Mostly, it will just simplify things for MLPs. Less lawyerly language in the SEC filings. Fewer subsidiaries when completing a transformative transaction. Now, MLPs will have more flexibility for their restructurings or reorganizations.

The uncertainty around tax reform and whether MLPs would continue to enjoy a tax advantage over corporations was likely an overhang on MLP units towards the end of last year, particularly in November. The tax reform question has now been settled, and investors are still able to enjoy the tax-deferred return of capital benefit that MLPs provide. Overall, tax reform hasn’t dramatically altered the MLP investment decision.

{kind=link}

{kind=link}