Summary

- As competition increases from private capital for projects in areas like the Permian, midstream companies are focusing on growth with solid returns.

- Midstream companies are targeting unlevered rates of return in the low to mid-teens or multiples of 4-8x EBITDA on new projects.

- Integrating existing networks of assets creates efficiencies and tends to drive higher returns.

In contrast to a win-at-all-costs or grow-at-all-costs approach, energy management teams, including midstream, are being prodded by investors to prudently evaluate projects and focus more on returns. In today’s environment, energy investors desire capital discipline and growth backed by solid returns. For midstream, attractive project returns have resulted in increased competition for projects, further reinforcing the need for discipline. Today, we will frame what midstream companies are saying about project returns.

The competitive landscape for midstream projects requires a focus on returns.

The attractiveness of the double-digit returns generated by energy infrastructure projects has brought increased competition. The rise in private equity involvement within energy infrastructure has benefited midstream as a source of funding and as ready buyers with deep pockets for potential asset sales. However, private equity has also increased project-level competition, with newbuild pipelines out of the Permian and crude export projects as examples (read more). Private equity firms and utilities have also been active in developing LNG export facilities and often related gas pipelines. Understandably, many companies want to capitalize on the long-term, structural benefits of growing US energy production, as opportunities remain plentiful across hydrocarbons.

To use the Permian as an example, private equity companies are developing large pipeline projects to address takeaway constraints for both natural gas and crude. Private equity-backed NAmerico is developing the Pecos Trail natural gas pipeline from the Permian. Another private company, EPIC, is developing crude and NGL pipelines from the Permian to the Gulf Coast. Still other private equity firms are partnering with large public companies on projects. Prolific midstream opportunities have resulted in heightened competition among Permian projects, and not every proposed project will necessarily be built. As an example, Magellan Midstream Partners (MMP) announced that it would not proceed as initially planned with the Permian Gulf Coast (PGC) crude pipeline, proposed by MMP and partners Energy Transfer (ET), MPLX (MPLX), and Delek (DK). While media reports painted the PGC news as a negative, we would argue that the announcement is positive for the companies involved and the midstream space broadly. Why? Scrapping a proposed project demonstrates to investors that management teams are committed to solid returns and fiscal responsibility. It also helps to allay fears that midstream companies will overbuild pipeline capacity.

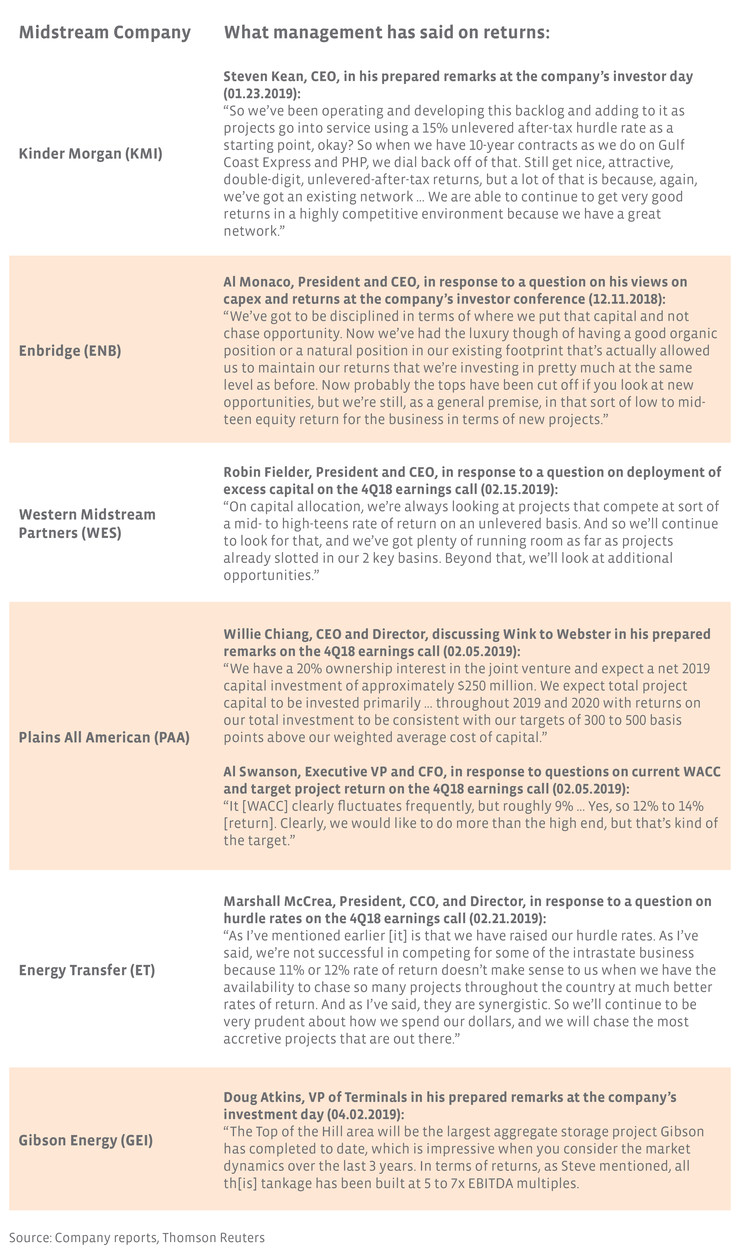

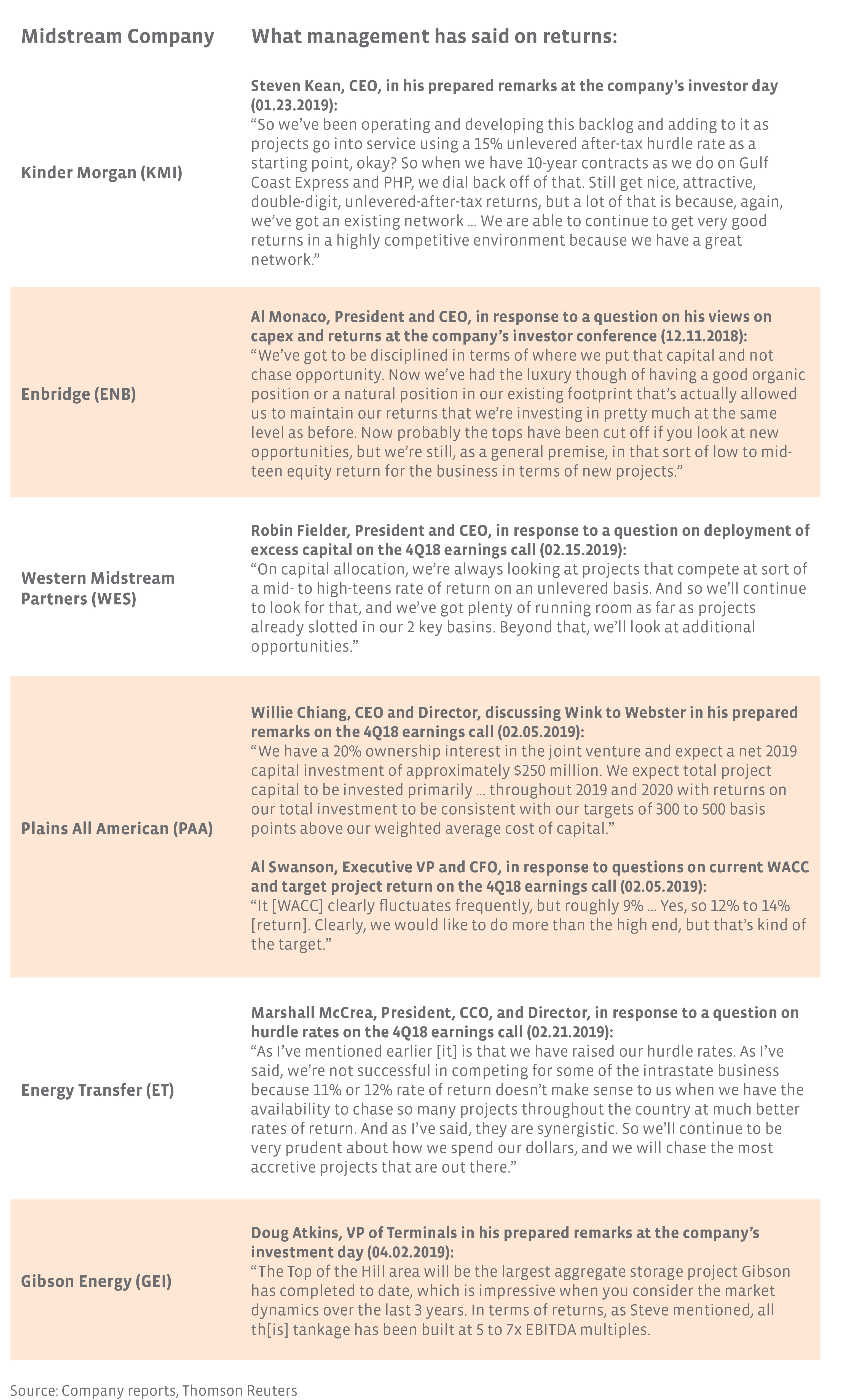

What are midstream companies saying about project returns and hurdle rates these days?

Like any company that ascribes to the basics of corporate finance, midstream companies are seeking a target return on projects that exceeds their cost of capital. Energy infrastructure companies generally frame project returns by looking at metrics such as EBITDA multiple and internal rate of return (IRR). IRR can be expressed on either a levered or unlevered basis. While most midstream companies utilize leverage (which enhances returns), unlevered returns were more commonly reported in the commentary in the table below. After examining transcripts and presentations from a number of midstream companies, we found that the general consensus for unlevered rates of return is in the low to mid-teen range, with some companies targeting a slightly higher return. We compiled management commentary on project returns from across midstream in the table below.

Some companies express their expected project returns as an EBITDA multiple. MMP stated in a recent conference presentation that it is targeting a 6-8x EBITDA multiple for its $1.25 billion growth capex backlog. ONEOK (OKE) expects to achieve a 4-6x adjusted EBITDA multiple for several projects slated for completion by 1Q20, including liquids pipelines and gas processing plants. To simplify EBITDA multiples, take for example a pipeline that costs $500 million to build with an expected 7x EBITDA multiple. The project would generate an estimated $71.4 million ($500 million divided by 7) in annual EBITDA. Directionally, the lower the EBITDA multiple for building a project, the better the implied return.

Notably, several management teams cited integration as a key driver of outsized returns on growth projects. Existing pipeline or terminal infrastructure may create a competitive advantage for a company pursuing a new or bolt-on project, enhancing returns relative to a standalone project. Leveraging existing assets is another means to realizing stronger returns. For example, the reversal of the Capline crude pipeline, jointly owned by Plains All American (PAA), BP (BP) and MPLX (MPLX), should drive higher returns than a newbuild project. With pipe already in place, PAA expects greater cost-efficiency and returns “significantly higher” than their typical threshold as discussed on the 4Q18 earnings call. Employing a network of existing assets or optimizing assets by combining them in strategic joint ventures should continue to improve project returns and capital efficiency.

Project returns look attractive given current company and asset valuations.

Given the relatively low EBITDA multiples for building energy infrastructure projects, the implied return is attractive and expected to create value for midstream companies. For context, the weighted average forward EV/EBITDA multiple for the Alerian Midstream Energy Index (AMNA) was 10.8x as of April 8, 2019. If midstream companies can build projects at a 4-8x EBITDA multiple, project backlogs should be expected to make a positive contribution on future company value. In addition, assets continue to be sold to private equity companies at a premium to the cost of building a project and a premium to where midstream equities trade. Recently, Williams (WMB) formed a $3.8 billion joint venture with the Canada Pension Plan Investment Board (CPPIB), with WMB contributing assets in the Marcellus and Utica. CPPIB is estimated to have paid 14x 2019 EBITDA for its stake in the venture. Similarly, SemGroup (SEMG) sold a 49% stake in its Maurepas crude pipeline system to Alinda Capital Partners at a 13x EBITDA multiple last year. Midstream companies will continue to create value if they can invest in assets at 4-8x EBITDA, whether or not they sell them at double-digit multiples.

Bottom Line

In contrast to investing in projects for the sake of growth alone, midstream’s focus on obtaining solid project returns while maintaining capital discipline should be a positive sign to investors. Increasing competition for attractive investments within midstream further enhances the need for a high level of discipline. As investors seek more capital-efficient companies across energy, midstream management teams that retain a disciplined approach to capital expenditures will likely be rewarded.

{kind=link}