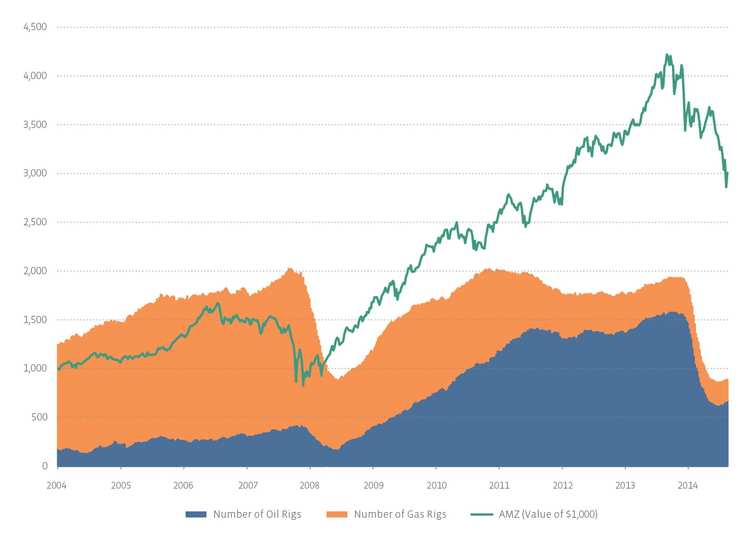

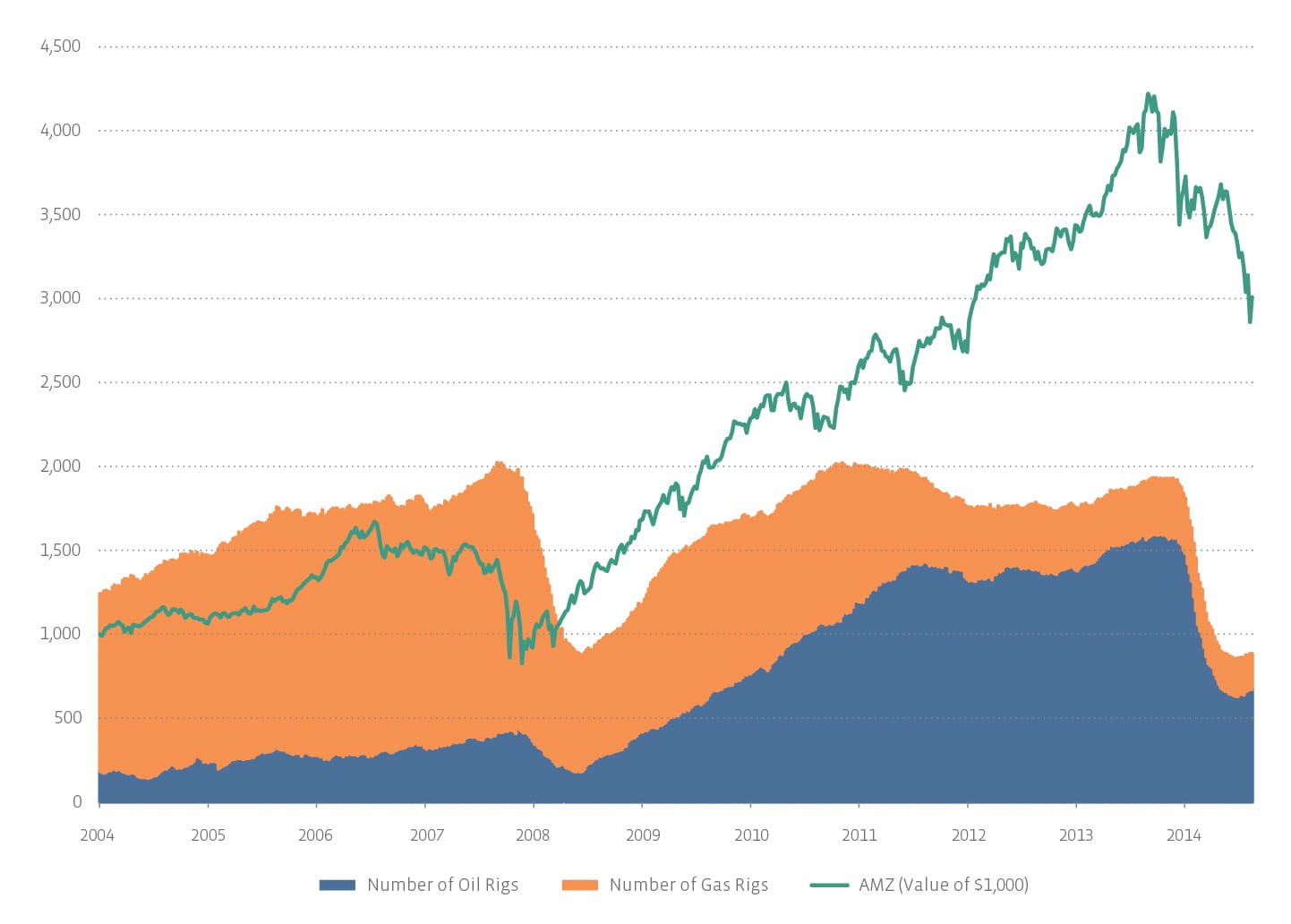

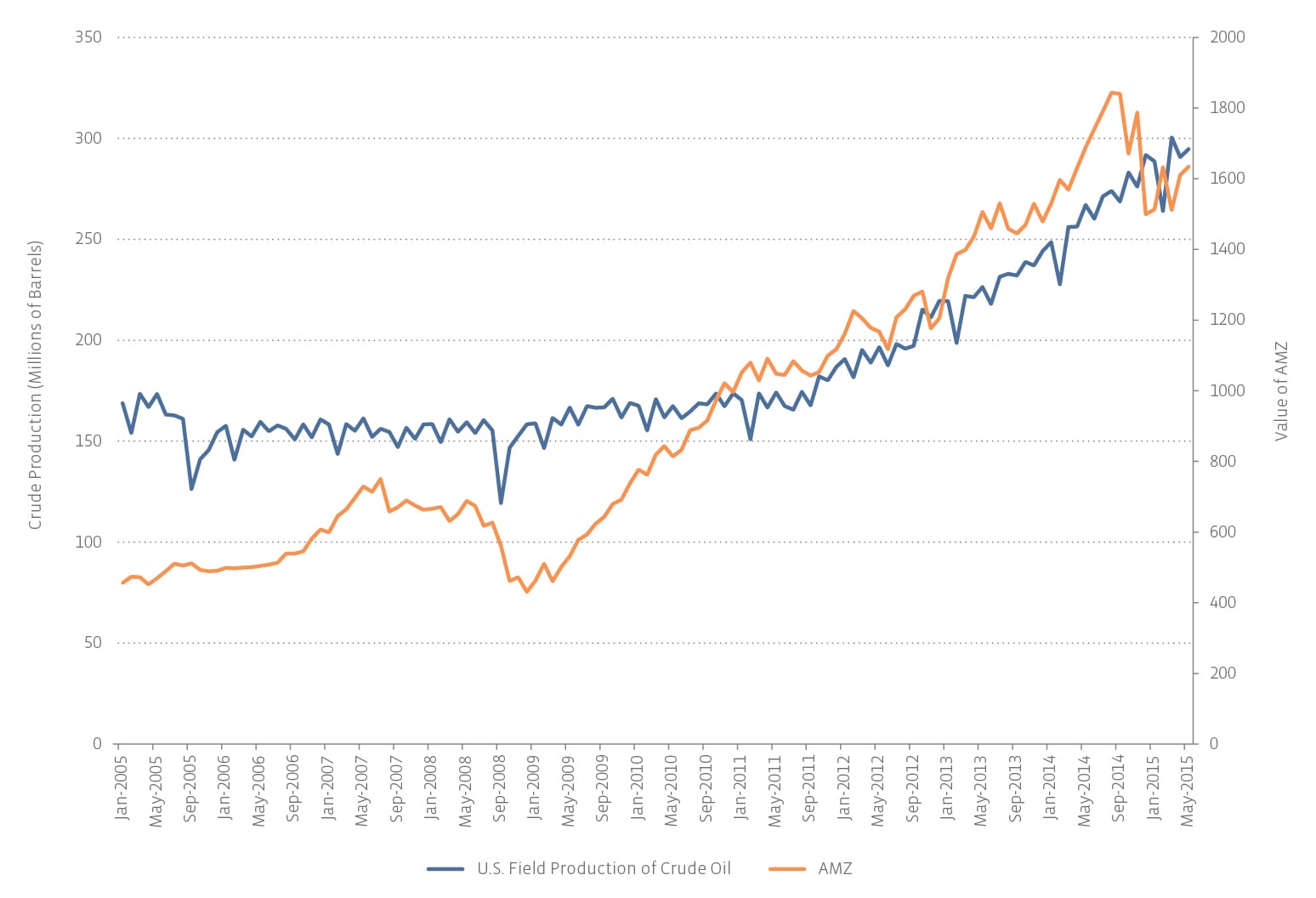

Most interesting is the 2009-2014 period, when rig counts remained relatively stable, and yet the AMZ continued to climb dramatically. During this time, wellhead spacing got tighter (more wells per acre), laterals got longer (horizontal drilling extends further), and frac stages got smaller (more fracs per well), resulting in significant increases in production per rig. So while rig counts were fairly constant, production rose significantly during the last five years.

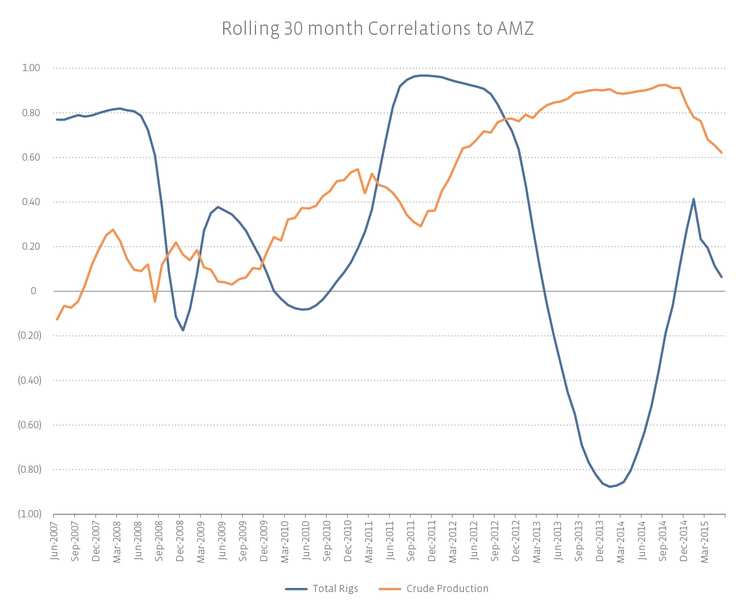

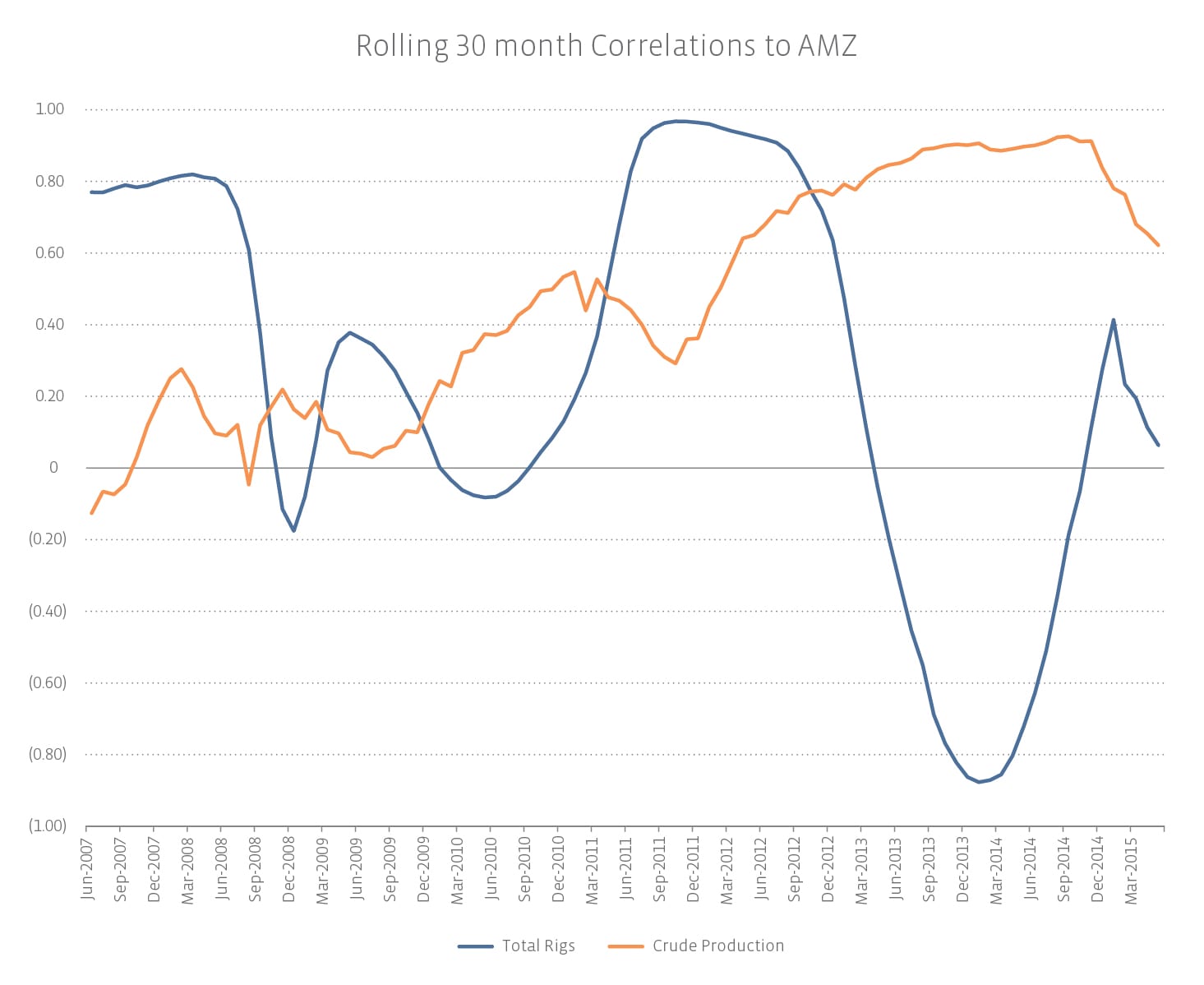

Since only one oilfield service company has ever been an AMZ constituent, it makes sense that the index has a lower correlation to rig counts (0.34) and a higher correlation to crude production (0.90). That high correlation number is quite striking, and I was tempted to label this the “Ah-HA!” moment and make it the whole point of this piece—that MLPs, having a price times volume business model, are heavily dependent on crude production. But when we examine correlations on a rolling 30-month basis, rather than over the entire 10-year period, a very different picture emerges.

The 0.90 correlation to crude production is actually not indicative of a steady, high correlation, but rather of a generally positive correlation that trended upward through a period of meaningful technological advancement, but has dropped off steadily in the last six months.

More surprising is the extreme fluctuations in rig count correlations. Sometimes, the correlation approaches one; a few years later, it approaches negative one. This volatility makes rig counts an exceptionally poor explainer or predictor of MLP performance.

Crude production could have explained MLP performance before the start of this year, but now, with a correlation of 0.62, it is not a dependable single-factor model.

These days, it seems like everything is volatile and unpredictable: the broader market, Greece, oil, MLPs. It can be hard to find a stable variable on which MLPs depend. Many investors view MLPs as alternative or defensive investments and appreciate that they are not correlated to any one factor. However, one element of MLPs has remained stable: distribution growth. In 2009, in the depths and wake of the financial crisis with capital markets closed, MLPs raised their distributions 2.5%. In 2010, they raised distributions 5.8%; in 2011, 5.6%. 2012: 6.5%. 2013: 6.3%. 2014: 6.3%. For the trailing 12-month period, MLPs raised their distributions 6.1%. One reason for this is that MLPs keep growing organically, as we’ll discuss tomorrow.

Everyone knows that the right thing to do in times of market volatility is to sit tight and stick with the plan, recognize that stocks are on sale, and not make any emotional decisions. Correlations spike close to one for almost all asset classes when the markets panic. But stability in cash flows and distribution growth, the hallmarks of the energy infrastructure sector, remain reliable.

{kind=link}

{kind=link}

{kind=link}