With interest rates at home still hovering near record lows, and most central banks pushing forth with loose monetary policy, many investors have been left yield starved. Luckily, the ETF universe spans far and wide, and when it comes to generating income, there’s no shortage of dividend-paying instruments. MLP ETFs in particular remain a favorite among those looking to capture meaningful dividends amid the low-rate environment.

We recently had the opportunity to speak with Jay D. Hatfield, a seasoned Wall Street veteran and fund manager behind newcomer InfraCap MLP ETF (AMZA ). Hatfield offers his insights regarding the MLP space as a whole, in addition to taking a deep dive under the hood of AMZA.

ETF Database (ETFdb): There’s a bit of criticism going around that the MLP ETF space has been getting crowded in light of numerous product launches. As an issuer, what opportunity do you see in that space? What compelled you to develop AMZA?

Jay Hatfield (JH): We continue to see a tremendous investment opportunity in midstream MLPs, but we believe the MLP sector demands an actively managed approach. An actively managed ETF is a low cost, liquid way to provide this advantage to investors.

Our experience in MLP portfolio management has taught us that significant retail ownership in the space often leads to irrational market behavior that an active manager can exploit. Furthermore, my experience on the operating side, as a midstream MLP co-founder and general partner, has given me a respect and understanding for the evolving dynamics of the sector and the need for ongoing portfolio vigilance [see also Understanding the Nuances of MLP ETF Expenses].

Over the last 12 months, the total returns of the 30 largest midstream MLPs have been wide ranging, with some stocks outperforming others by well over 50% (Figure 1). Additionally, the market saw Boardwalk Pipeline Partners, at the time a component of many MLP ETFs, drastically cut its distribution, resulting in significant stock underperformance. While the outlook for midstream MLPs is very bright in our opinion, data points such as these strengthen our belief that the space demands an active approach. We are pleased to introduce the first actively managed ETF focused entirely on the midstream MLP space.

ETFdb: Building off the first question, what sets your offering apart from more established competitors in the MLP ETF space?

JH: We offer investors active management by a seasoned investment team at a comparable cost to leading, passive MLP ETFs. We take into account MLPs’ estimated total return and use it to optimize the weightings of the leading MLP index. We focus on MLPs’ ability to generate returns on invested capital in excess of their cost of capital and favor those with attractive organic spending opportunities. We also selectively invest in the general partners of these MLPs.

We believe that this approach lowers risk and provides the investor with the potential for superior returns. Our goal is to outperform passive MLP ETFs by 2% to 4% annually over time. We view our product as optimized MLP exposure.

ETFdb: When shopping for an MLP-focused product, what do you think are some common oversights among investors? How does AMZA address those?

JH: Not all MLPs are created equal, and investors should be aware of this. For example, in a search for yield, some products may take on risk by owning smaller or more commodity-sensitive MLPs. Investors must focus on the quality and content of the ETF’s underlying portfolio. Our investment selection universe is strictly the largest 30 midstream MLPs by adjusted market capitalization and the related general partners of those MLPs [see also ETFdb’s Energy Bull Portfolio].

We believe this limited universe provides our investors with exposure to the highest quality midstream MLPs available. These volume-based, ‘toll-road’ style businesses derive the majority of their cash flow from the gathering, processing, transportation, and storage of oil, natural gas, natural gas liquids, and refined products.

ETFdb: Aside from attractive dividend distributions, what else might investors find appealing about this asset class and AMZA in particular?

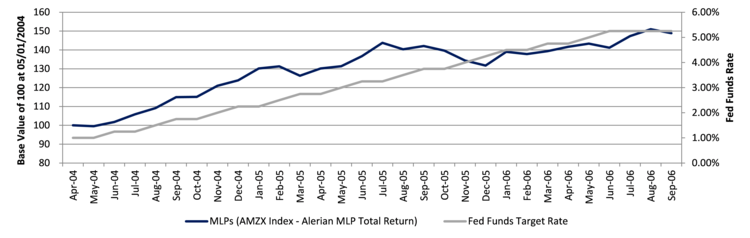

JH: MLPs are a total return asset class that has generated compound annual growth of over 15% over the past 15 years. These returns are due to an attractive distribution yield component, but are also largely due to consistent growth in distributions. This growth has allowed MLPs to perform well in rising interest rate environments. It is worth noting that the sector generated over 40% in total return during the last Fed Funds’ tightening cycle from 2004 to 2006 (Figure 2).

In our opinion, this continued growth in distributions makes MLPs a great total return investment in the current market environment.

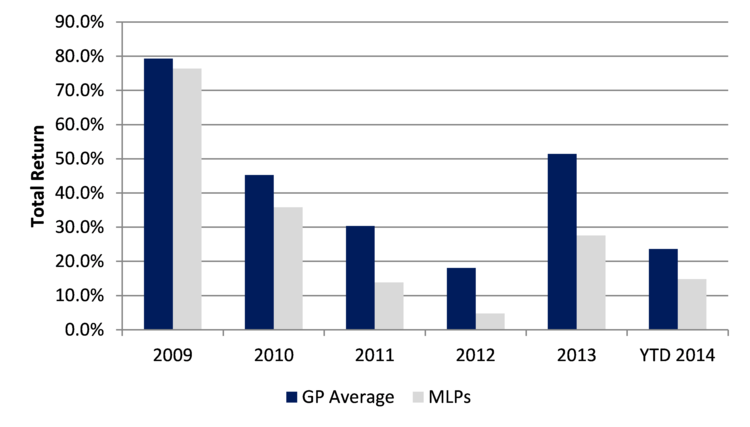

AMZA also invests in the general partners (GPs) of certain MLPs. GPs operate MLPs and typically earn a growing percentage of the underlying MLP’s cash flow over time. An increasing number of GPs have come public, and in certain circumstances these vehicles are more attractive investments than the underlying MLPs themselves (Figure 3).

As the GP of an NYSE-listed midstream MLP ourselves, we possess a deep understanding of this dynamic and believe that AMZA’s ability to actively invest in GPs provides investors the potential for superior returns over time as the space continues to mature. This dynamic has played out recently with Targa Resources’ (TRGP) acquisition of Atlas Energy (ATLS). ATLS is the GP of Atlas Pipeline Partners (APL). Given a strong valuation argument and compelling total return outlook in ATLS, we took position and reduced some of our weighting in the underlying MLP, APL. This choice has led to outperformance for our investors.

AMZA weightings also take into account total return outlook. This focuses on each MLP’s combination of yield and distribution growth expectation and also incorporates views concerning mergers and acquisitions and other capital markets activity. A great example of this is our overweight position in Access Midstream Partners LP (ACMP). Williams Companies Inc. (WMB), the GP of Williams Partners L.P. (WPZ) and ACMP, had proposed a merger between ACMP and WPZ in June.

After discussions with management and taking our own operating experience into account, we felt that there was a strong likelihood that before the deal could be approved, WMB would revise terms to be more beneficial to ACMP unit holders than originally announced. Our hypothesis was confirmed when WMB announced revised terms in October, and our overweight position in ACMP led to outperformance for our investors.

There are two other aspects of our actively-managed strategy that I want to highlight. We intend to use some options strategies, such as covered-call writing, to enhance returns and limit risk. In addition, we have the ability to use modest leverage opportunistically. We think this feature gives us additional flexibility to add incremental return [see also The Ultimate Guide to Screening Energy ETFs].

Lastly, we think investors will appreciate our targeted 8% dividend yield and tax reporting on a single form 1099 with no K-1s.

ETFdb: Broadly speaking, what are some of the longer-term trends that you are seeing in the domestic energy market? How about on the global scale?

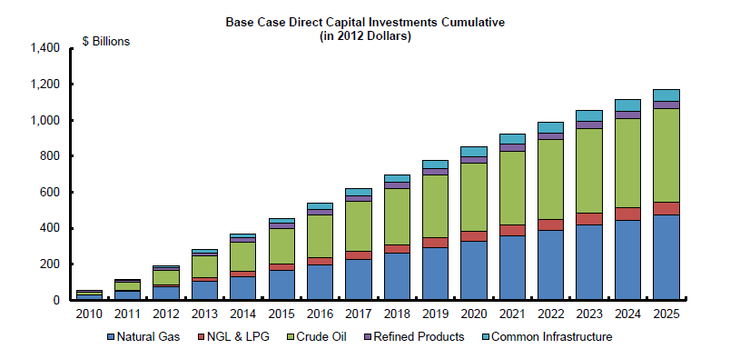

JH: Midstream energy infrastructure capital expenditures have totaled over $50 billion annually for the past few years, and industry studies indicate that this level of spending will continue well into the next decade as infrastructure is needed to support the prolific commodity production from shale plays in the U.S. (Figure 4). In our view, this spending, coupled with the likelihood of increasing exports adding to the infrastructure need, will continue to support attractive sector distribution growth over time.

We have also seen signs of industry consolidation in the space with two large players, Kinder Morgan and Williams, announcing transformative restructurings over the past year in part to better position themselves as acquirers going forward. We believe this trend may continue, and we actively monitor the MLP landscape for potential corporate events in considering our investments. A great example of this is our previously mentioned investment in Atlas Energy.

The Bottom Line

Generating a meaningful income stream, especially in the current environment, is no easy task. That being said, MLPs by nature offer a compelling opportunity for anyone looking to beef up their portfolio’s overall yield. However, simply going after the highest yielding securities is a less-than-ideal approach. As such, the recently launched AMZA warrants a closer look under the hood from anyone who is eager to jump into the MLP space but is wary of doing so through a “plain vanilla” index-based ETF.

Follow me on Twitter @SBojinov

[For more ETF analysis, make sure to sign up for our free ETF newsletter]

Disclosure: No positions at time of writing.