Robo-advisors are one of the newest and most rapidly growing innovations in the finance industry. And while some start-up FinTech firms have begun to make a name for themselves on Wall Street, industry veteran Charles Schwab has also entered the game, delivering its own fully automated investment advisory service.

We recently had the opportunity to talk with Tobin McDaniel, President of Schwab Wealth Investment Advisory, Inc., who took us behind Schwab’s Intelligent Portfolios and how robo-advisors are helping to evolve the financial landscape.

ETF Database (ETFdb): Why did Schwab decide to get into the robo-advisor business?

Tobin McDaniel (TMD): There is a real need to make investing more accessible to more people in order to help them reach their financial goals. What we’re trying to do with Schwab Intelligent Portfolios is remove many of the common barriers people face when it comes to getting invested and getting advice on how to manage an investment portfolio – barriers like costly fees, high minimums, complexity, and people’s inertia in terms of getting started.

A service like Schwab Intelligent Portfolios makes it easy for investors to get started because it is entirely online and takes just a few minutes to get invested. It makes it easy for investors to stay on track, because the portfolios automatically rebalance and adapt to market changes. And it’s very accessible with a low minimum investment and very low fees. Schwab Intelligent Portfolios doesn’t charge any advisory fee, commissions or account service fees, so the only thing an investor pays are the ETF fees which they would pay anywhere they invest.

ETFdb: What makes Schwab Intelligent Portfolios different from other robo-advisors?

TMD: We think our service has a unique combination of features compared to similar types of products in the industry. We’re not charging any advisory fees, our portfolios are sophisticated with up to 20 asset classes using both cap-weighted and fundamentally-weighted strategies, we have live investment professionals available 24 hours a day and 365 days a year, and our service is backed by the security and stability of a firm with $2.5 trillion in assets and 40 years of experience working on behalf on investors.

ETFdb: Who should use Schwab Intelligent Portfolios? Is there a specific type of investor or demographic you are targeting with this service?

TMD: We launched Schwab Intelligent Portfolios in March and by the end of June had grown to more than $3 billion in assets under management and more than 39,000 accounts, with a broad range of clients using it. We think an automated investing service like this can be appropriate for an investor who is looking for a different way to invest and who is comfortable using technology to make things more efficient. We have clients who are young and just getting started with investing – about half of Schwab Intelligent Portfolios clients are either Millennials or Gen-X. We also have older, more experienced clients using it – about half are Boomers or Matures and roughly 15 percent of Schwab Intelligent Portfolios clients have $1 million or more invested with Schwab overall.

ETFdb: Tell us about the methodology the Charles Schwab Investment Advisory team uses to build the Intelligent Portfolios.

TMD: Asset allocation and diversification are really the basis of the Schwab Intelligent Portfolios investment methodology. The portfolio asset allocations are built to reflect a client’s goals and risk tolerance while factoring in market changes and client preferences for loss aversion and income.

The funds for Schwab Intelligent Portfolios are selected based on objective criteria, with a focus on high quality and low costs. We look at the entire universe of ETFs and then filter based on a fund’s risk level, size, spread, and how consistently it has tracked its underlying index. Once those factors are met, we prioritize ETFs that have the lowest operating expense ratios.

Finally, Schwab Intelligent Portfolios uses a combination of market cap-weighted and fundamentally-weighted methodologies to further enhance the diversification of the portfolios since the two can perform differently across various market cycles.

ETFdb: How does the algorithm match investors with an Intelligent Portfolio? Can you give us an example of an investor profile and its matched portfolio?

TMD: To get started, an investor completes an online questionnaire that takes a few minutes and is designed to assess his or her goals along with financial and emotional capacity for risk. Using this information, the algorithm recommends an appropriate portfolio.

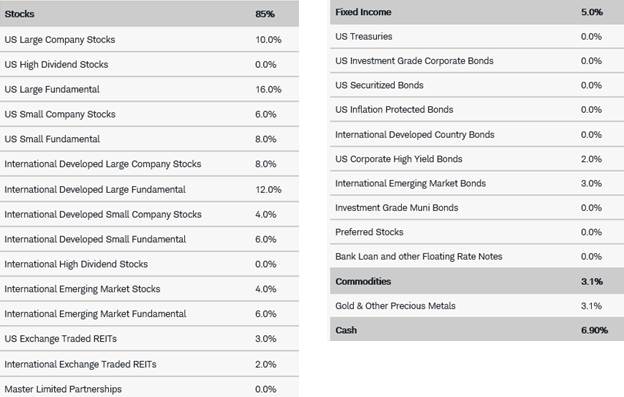

Below is a sample Schwab Intelligent Portfolios asset allocation for a 30-year old in an aggressive portfolio with a goal of saving for retirement:

ETFdb: Are the portfolios dynamic? Will they change allocations over time or shift based on short-term macro trends? How does this process work?

TMD: The portfolios are a set strategic asset allocation designed to meet an investor’s goals and risk profile, and the algorithm maintains that allocation over time through daily monitoring and rebalancing when the allocation drifts outside of the set parameters. For clients with longer term goals, such as retirement 20, 30, or 40 years down the road, we recommend that they periodically revisit their time horizon to determine the right allocation and level of risk for them. This is an instance in which some clients might find it useful to speak with someone, and we have investment professionals available for these kinds of 1-1 conversations.

ETFdb: What do you say to the skeptics?

TMD: Automated investing, or as it is often referred to, “robo-advice,” has actually been embraced by many pundits as the next big thing in investing. So, in a sense I might answer by saying some skepticism is actually a good thing. We think automated investing maximizes the power of technology, serves a great need and will grow dramatically over the coming years. But most investors want to have access to people at some point and the auto-investing is simply a tool within a larger set of resources that include a solid trusted relationship with your investment services firm.

ETFdb: How do robo-advisors perform against their human counterparts?

TMD: We’re still in the early innings when it comes to automated investing services, and we think of it as a tool for longer term investors. That said, we don’t see it as an “either-or” dynamic when it comes to so-called “robo” offers and human advisors. We think the majority of people, whether they are younger or older, will ultimately want a combination of the two over their lifetime – possibly using an automated service to efficiently manage their portfolio over time, but then working with an advisor when their financial picture gets more complicated or they need more specialized help. There’s a school of thought in the industry that Millennials will always be satisfied investing from their phone or sitting at their computer and they’ll never be interested in talking to a person, but we think that is a misconception.

We recently conducted a study that asked investors about their preferences for working with technology and people when it comes to investing. Interestingly, Millennials show the strongest preference for relying on people when their lives get more complex. 75 percent of Millennials we surveyed think they will want to talk with a professional advisor when their financial situation gets more complicated as compared to 72 percent of Gen-Xers, 71 percent of Boomers, and 64 percent of Matures.

ETFdb: What are some major robo-advisor and ETF industry trends you expect will dominate the space in the foreseeable future?

TMD: Frankly, we think of the introduction of automated investing services as an evolution in the industry as opposed to a revolution. For some time now technology has been evolving to make investing more accessible and efficient. The introduction of online trading is maybe one of the most obvious examples of a development that made a huge impact on how people invest. ETFs are certainly another innovation that comes to mind.

Automated investing is simply another step in that evolution, albeit an important one. We expect more people to learn about these services and use them over time, because something like Schwab Intelligent Portfolios meets a huge need in terms of making investing more accessible, more transparent, and less costly. As awareness and demand increase, we’re also likely to see more firms of all types and sizes offering some form of an automated portfolio product as part of a broader suite of advisory solutions. And that’s a good thing, because getting more people on track to meet their financial goals is critically important.

The Bottom Line

For those looking for an easy, cheap, and hands-free approach to investing, Schwab’s Intelligent Portfolios may be a compelling option. And with the expertise of an industry giant at the helm, it will be interesting to see how this robo-advisor will perform in the future..

Follow me on Twitter @DPylypczak.

Disclosure: No positions at time of writing.