Generating a meaningful stream of income amid the persistently low-rate environment has left many investors starving for yield. Luckily, the ever-expanding ETF universe has spawned dozens of options for those looking to beef up their portfolio’s dividend stream; below we dive into a compelling opportunity for anyone starving for yield that also wishes to stray away from traditional dividend-focused funds.

We recently had a chance to talk with Kevin Kelly, Managing Partner and Chief Investment Officer of Recon Capital Partners, and learn more about his firm’s flagship product, the NASDAQ 100 Covered Call ETF (QYLD).

ETF Database: What was the motivation behind launching the Nasdaq 100 Covered Call ETF (QYLD)?

Kevin Kelly (KK): In May of 2013, we were focused on bringing a strategy that would outperform, and capitalize in a post-quatitative easing, Fed intervention environment as the Taper Tantrum shook the financial markets. If you recall, the markets became extremely volatile on the premise that tighter monetary policy would push up borrowing costs in a way that wounds growth. Short-term interest rates and longer run bond yields surged as investors priced markets for the removal of central bank bond purchases and equities sold off.

We found that the best strategy would be a monthly covered call program. It would have lower volatility than the equity markets and would also generate high monthly income by selling options. The strategy could serve as a fixed income alternative or lower the volatility of an equity portfolio.

Mark Wolfinger states it best in his book the Rookie’s Guide to Options, “Covered call writing easily outperforms a buy and hold investment strategy most of the time: in down markets, in steady markets and in up markets—failing to outperform only during those strong upwards markets.” With that mindset, we needed to choose the appropriate portfolio of securities and technology and healthcare companies in the NASDAQ-100 proved to have great balance sheets, revenue growth, reinvestment in R&D, as well as leaders in their industry.

Furthermore, we found that the NASDAQ-100 has higher volatility, generating higher options premiums, than the S&P500 but still provides the diversification of quality, blue-chip, innovative, growing companies like Apple, Microsoft, Google, Starbucks, Costco, and Tesla.

ETF Database: Please explain the mechanics behind QYLD. Why does the ETF wrapper make sense for utilizing this sort of strategy?

KK: The Recon Capital NASDAQ-100 Covered Call ETF owns all the constituents in the NASDAQ-100 and sells the index call option against that portfolio every single month and then rolls the option on the third Friday of the month. The Fund generates monthly options premiums and when we take in that premium, we distribute it out to shareholders.

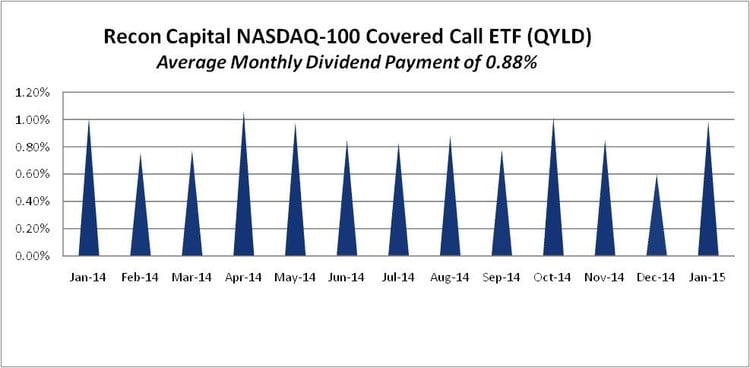

Every month, holders of record are going to get that monthly options premium in their accounts. If you look at last year, we distributed 10.4% from the monthly options premiums that came in. Options premiums tend to be fairly consistent in their volatility regime.

The ETF vehicle is beneficial to investors as it allows the ETF issuer, Recon Capital, to write the call options on the NASDAQ-100 Index, rather than an individual investor needing to undertake a potentially expensive, time consuming, and complex call writing process on the entire NASDAQ-100.

QYLD offers the benefits of professional options management at a 0.60% expense ratio, a relatively low cost when compared to a self-directed account. Covered call strategies can have higher transaction costs over traditional buy and hold strategies.

The ETF wrapper also makes sense because it allows the fund to trade at or around Net Asset Value (“NAV”) throughout the trading day as opposed to a significant premium or discount that can happen in closed end funds or getting out at NAV at close in mutual funds.

ETF Database: Aside from generating current income, what else might investors find appealing about QYLD in the current environment?

KK: Aside from generating high, current income, QYLD provides differentiated income. Other asset classes are susceptible to rising interest rates, duration concerns, and monetary policy but QYLD income does not have interest rate or duration risk. The income is derived from selling volatility. It’s a great fixed income alternative.

From the equity side, there has been a relentless search for yield, and investors have piled into dividend-yielding stocks, including utilities and REITs, making them extremely expensive from a historical basis, and only are compensated at less than a 5% yield. QYLD distributed 10.4% last year and that was unlevered. QYLD consistently distributes monthly income from options premiums.

Overtime, covered call writing programs provide similar returns to owning a diversified stock portfolio, but with much lower volatility, so it should be a preferred strategy for many investors. Investors need to look their portfolios and decide what type of covered call program would work for them.

ETF Database: Broadly speaking, what tailwinds do you see for the alternative-strategy product space on the horizon? What are some headwinds that may pose challenges for this corner of the exchange-traded market?

KK: The alternative strategy segment will continue to experience robust demand from retail and institutional investors. The first and foremost reason is that investors can get the same absolute return profile at a better price with the added benefits of transparency and liquidity. New ETFs in the alternative space post a serious threat to active managers, especially those who charge high fees for little added value or not generating alpha. Closet indexers will also have to take notice as well.

The key takeaway is that ETFs are a big competitive threat to mutual funds and hedge funds because there are now plenty of low-cost, transparent, and formulaic (or tilts) factor funds. In general, low-cost investing is the winning strategy for most investors and now it can be done in a ‘portable alpha’ way.

Another tailwind is the outlook for 2015 and the next few years suggest that bifurcation of economic outcomes will be playing out in the markets. During the financial crisis, global economies, and asset prices, tended to move in tandum during the immediate slump and the 2009 recovery. The alternative segment should benefit from correlations diverging and adding value to investment portfolio because they are designed to either improve return or alter risk relative to traditional market-capitalization-weighted indexes.

Headwinds are definitely education of the product strategy and the vehicle (ETF). There is a wide dispersion of risk and return among liquid alternative funds coupled with varied approaches by managers in varies asset classes. It will take time for adoption at the SEC level as well as in the marketplace.

The Bottom Line

There’s no shortage of dividend-focused strategies in the ETF wrapper. QYLD separates itself from the pack by applying a conservative income-generating options strategy to one of the most popular benchmarks on Wall Street. As such, this ETF warrants a closer look from anyone looking to collect consistent dividends all the while being favorably positioned for more upside in the equity market.

Follow me on Twitter @Sbojinov

[For more ETF analysis, make sure to sign up for our free ETF newsletter]

Disclosure: No positions at time of writing.