The bears are at it again in Shanghai as the Chinese stock market suffered its worst single-day drop since 2007 on Monday morning.

The headlines across financial news media outlets are bracing everyone for the worst as selling pressures in China spill over onto Wall Street. Following an encouraging rebound after a stretch of unprecedented government intervention, vicious profit-taking pressures have returned to the Chinese market that are leading many to believe we are far from the bottom. Even worse, many are predicting that developments in China will be the straw that breaks the U.S. bulls’ back, sparking a major correction at home.

For many domestic investors, the question at hand is whether or not the sell-off in China is a real reason to worry? Or does it fall under the “noise list” of things we read on a daily basis?

Follow the Leaders

We’re all bombarded with changing information and opinions every minute of the day. The trick is developing a “lens” that allows you to filter out what matters from distractions that don’t matter; you don’t want to react to every piece of news, but you also don’t want to miss out on any important turning points. One way to make this challenge easier is by focusing on determining whether or not the given development (be it meaningful or noise) has had an impact on the market. In other words, we want to see how various asset classes have performed, in relation to a broad-based benchmark, since the beginning of the development we are analyzing.

In market trend analysis, keeping an eye on leaders and laggards is an insightful way to extract insights during volatile times; for instance, if sector leaders are holding up well during a sell-off, this gives you more conviction that the broader market will rebound. Likewise, if you notice market leaders getting crushed and breaking below key support during a market sell-off, you might be more worried about the fate of the broader market.

China Sell-off Hasn’t Mattered...Yet

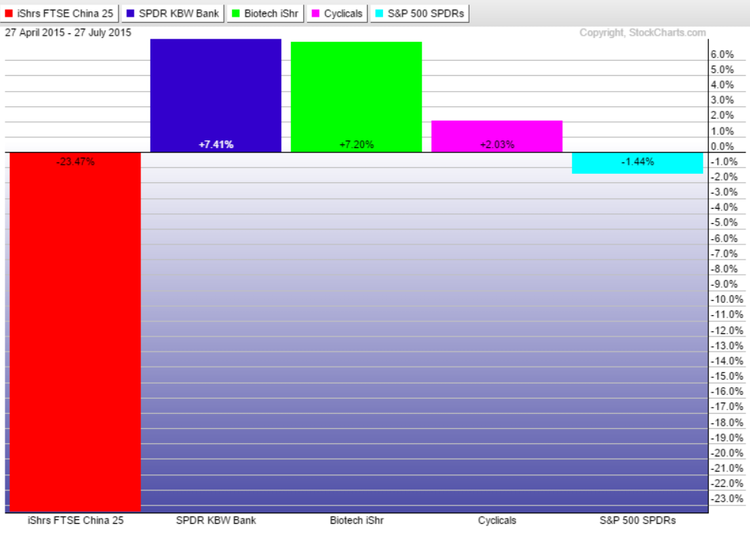

Let’s examine how the market leaders – banks, with the SPDR S&P Bank ETF (KBE ), biotech, with iShares’ Nasdaq Biotechnology ETF (IBB ), and consumer discretionary equities, with the Consumer Discretionary Select Sector SPDR ETF (XLY ) – have performed in relation to the broader market (SPY) since bullish momentum peaked in China (FXI) on April 27 (compiled with StockCharts, returns as of 7/27/2015):

Now let’s consider the returns from the table above along with the daily one-year price charts for the discussed ETFs. Since momentum peaked on April 27, FXI has come under stiff selling pressures, shedding upwards of 20%, and breaking all sorts of key technical support levels along the way. In this same time frame, the U.S. market, as represented by SPY, has managed to shed just under 1.5%. Furthermore, when we consult the charts, we see the security has largely traded sideways within a range, which leads us to believe that the China meltdown hasn’t truly rattled investors at home just yet.

Moving on to the leaders, we get further confirmation of the U.S. markets’ internals remaining firmly intact. Since FXI began its sharp descent, the bank (7.4%), biotech (7.2%), and consumer discretionary (2%) ETFs have not only managed to remain insulated from selling pressures, they’ve even raked in solid gains during an otherwise tumultuous period for global equity markets.

Going back to our original question – should we be rattled by the China sell-off? When we consider the fact that the broad market has yet to stage a meaningful reaction to developments in China, coupled with the fact that sector leaders remain in strong positions after the rout, we feel confident that bullish forces remain in control on Wall Street.

The Bottom Line

The sector leaders on Wall Street have yet to be rattled by selling pressures in China which leads me to believe that sell-off news spilling over from Asia is more “noise” than a real reason to worry.

Follow me @SBojinov