The analysts here at ETF Database analyzed the search patterns of visitors to our site during the week. Below, you’ll find our analysis of the top five trends. By analyzing these trends, we hope to unlock a better understanding of the investment themes trending on our site and in the market.

Financial Equities

The Financial Equities ETF list was a top-trending page on ETF Database this week, with a increase in traffic by 84% from the previous week. It looks like our readers were interested in ways to play a possible December interest rate hike. After the jobs report on Friday, with 271,000 jobs for October and a 90,000 jobs beat, it is clear that the possibility of a hike is high. Generally, if you believe the hike will come this year, you are short energy, materials and industrials, and long consumer discretionary and financials. Friday was a great day for the financial sector, with an increase of 1.5%.

Aerospace & Defense

The Aerospace & Defense ETF list continued its trend on ETF Database this week. The traffic to this page has increased by 43%. As we mentioned in our previous trends article, the three main ETFs in this industry are (ITA ), (PPA ), and (XAR ). These ETFs have high betas which means they are sensitive to market movements. Since the markets have been bullish in the past few weeks, these ETFs performed well.

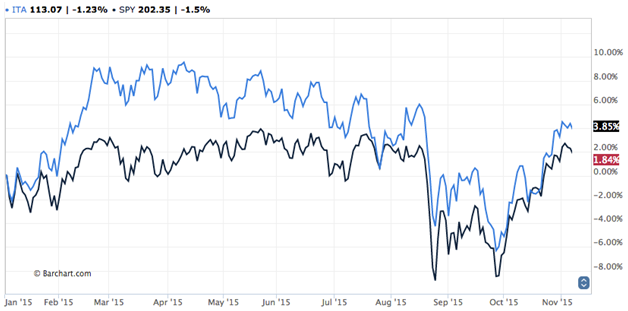

ITA has been outperforming the other two ETFs, gaining 3.85% YTD. That’s higher than the overall market gain of 1.84% YTD, as measured by the S&P 500 ETF (SPY ). Commercial aerospace is definitely doing well, especially due to the increase in the demand for travelling via airplanes in emerging regions, such as the Middle East and Asia Pacific.

The defense sector is underperforming the commercial aerospace industry, but, as many nations are equipping themselves with defense platforms these ETFs will not be left behind.

For more information read our article on Defense & Aerospace.

Chinese Equities

The Chinese Equities ETFs page was trending on ETF Database this week, with an increase in traffic by 26%. It looks like our readers were interested in ways to gain exposure to funds that invest in China-based corporations. There is no doubt that this year has been an eventful one for Chinese equities, with a huge sell-off this summer, the A shares rollercoaster, and the PBOC continuing to cut its one-year interest rate at the end of October. Although China so far has had a bad year, there is the possibility that the nation is re-entering a bull market rally as the Shanghai Composite index has rallied for the second day in a row this week.

At ETF Database we are not bullish on the Chinese economy as a whole, but there are some sectors worth looking at. The first one is the technology sector, with companies such as JD (JD) continuing to profit from an increase in internet consumption. Also, Baidu (Bidu) has performed well, with shares jumping 7% in after-hours trading in late October. At about $200 per share, Baidu is more expensive than Alphabet in both P/E and P/B. The main problem with the Chinese technology sector is that it trades at high multiples.

Another good way to play China is to invest in the health care sector via Asia Pacific. Asian health care stocks are currently in vogue, and the MSCI AC Asia Pacific Free/Health Care Index has return 16.4% YTD, compared to the overall Asian Pacific market which has had no significant return. China currently has a large health care spending gap; in the past two years health care expenditure has been 5.6% of GDP (2013) and 5.9% of GDP. From the demand curve there is also a gap, with an aging population over 20%. According to Deloitte, medical tourism is expected to become a growth industry in China, carried by government policies, low medical expenses and qualified medical personnel. Also, Mckinsey & Company forecasts that health care spending in China will reach $1 trillion by 2020. It is also important to notice that the younger population is becoming more health conscious, creating an explicit shift in the health care demand curb.

Consumer Discretionary

One of the biggest trends this week was our consumer discretionary page. The Consumer Discretionary ETF page had an increase in traffic of 26%. Currently, the sector is reporting the third-highest earnings growth rate, with more than 12% growth. This earnings season 19 industries reported growth (of the 31 industries in this sector). The main industries that lifted the sector were the automobile manufacturers industry, internet retail as well as general merchandise stores.

This week some big names in the consumer discretionary sector reported earnings. Honda Motor Co. (HMC) started the week off with earnings per share of $59 cents for Q2 of FYE 2016, compared to $61 cents a year ago, with EPS missing the analyst consensus of 63 cents. Sales of $30.19 billion also missed the consensus of $30.22 billion. However, Tesla had a very good week after beating expected guidance. Tesla (TSLA) rose more than 10% after hours. The company also delivered 11,603 new vehicles in Q3. Going forward Tesla plans to deliver 15,000 to 17,000 vehicles for Q4 FYE 2015. Another big name this week in the consumer discretionary sector was Disney (DIS), with Q4 revenue of $13.5 billion, in line with FactSet’s revenue consensus, and EPS of $1.2 vs. the $1.14 consensus.

The Consumer Discretionary ETF (XLY) hit a new 52-week high yesterday. The sector is the best performing sector this year. Going forward it seems that the sector is gaining a lot of momentum. For example, Amazon (AMZN) pushed the sector higher after its earnings were realized. In addition, the decrease in oil prices which leads to an increase in disposable income, as well as the improving U.S economy are making the sector a good place to invest heading into 2016.

The Euro

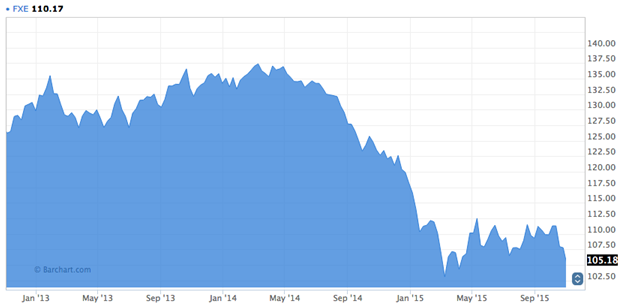

The euro has been trending recently, with traffic to the EUR ETF page increasing by 20% since last week. The eurozone is a hot topic of conversation across the markets and has been ever since the Greek crisis started in late 2009. Currently, the main focus is the ECB’s €1.1 trillion ($1.18 trillion) quantitative easing program which started this past March and should run until September 2016 or longer. On October 22, after the ECB’s policy meeting, Mario Draghi, President of the ECB, signaled that if needed the ECB stands ready to adjust size and duration of the QE program. Draghi’s remarks sent European equities higher and government bonds lower. The economy in the eurozone remains sluggish and the region’s main equity indexes are having a hard time remaining in positive territory.

The euro has decreased more than 10% YTD. Besides country-specific problems from Greece to Spain, the main problem with the eurozone is structural and based on simple economics; simply put, there is no matchup between economic policy and fiscal policy. The eurozone has a central bank but not a central fiscal institution. Given the fact that currency moves last two or three years and the euro has been down since May 2014, we believe the best way to play the euro is to go short going into 2016.

The Bottom Line

This week we saw two sectors outperform the market: the financial and consumer discretionary sectors were the clear winners. We continue to see an increase in interest in the aerospace and defense industry as well as a comeback for Chinese equities. At the same time, the euro has been lagging behind, not only this week but also during the past few months.

By analyzing how you, our valued readers, search our property, we hope to uncover important trends that can help you understand how the market is behaving so you can fine-tune your investment strategy. At the end of each week, we’ll share these trends for the week, giving you better insight into the relevant market trends that will allow you to make more valuable decisions for your portfolio.