To help investors keep up with the markets, we present our ETF Scorecard. The Scorecard takes a step back and looks at how various asset classes across the globe are performing. The weekly performance is from last Friday’s open to this week’s Thursday close.

- U.K. GDP contracted 0.4% in December compared to the previous month, largely due to a fall in spending during the holiday period and Brexit uncertainty. The British economy grew by 0.2% in the last quarter of the year versus the prior quarter, disappointing analysts, who expected 0.3% growth.

- British manufacturing production slumped 0.7% compared with a forecasted 0.2% growth. Manufacturing production has been heading down for three consecutive months now.

- At the same time, a global deflationary spiral has hit Britain as well. The country’s consumer price index dropped to 1.8%, the lowest level since January 2017. As inflation receded, the country’s central bank is increasingly unlikely to raise interest rates.

- U.S. inflation dropped to 1.6% in January due to lower fuel prices, hitting a 19-month low. The decline came shortly after the Federal Reserve made a dramatic U-turn, strongly indicating it will not continue to raise interest rates.

- Crude oil inventories were up for the fourth consecutive week in the five-day period ended February 8, increasing by 3.6 million barrels. In the prior week, stockpiles were up by 1.3 million barrels.

- The Japanese economy grew by 0.3% in the final quarter of the year, or an annualized growth of 1.4%. The expansion comes after the GDP contracted in the previous quarter by an annualized 2.6%.

- Meanwhile, Germany reported no quarterly growth in the fourth quarter of 2018, showing that the largest European economy has been struggling of late. Year-over-year, the German economy rose by 0.9%.

- In the U.S., retail sales posted the largest drop in more than nine years in December, an indication of the economy’s weakness. The index collapsed 1.2% against expectations of 0.1% growth. Core retail sales declined more abruptly, down 1.8% compared with expectations of zero growth.

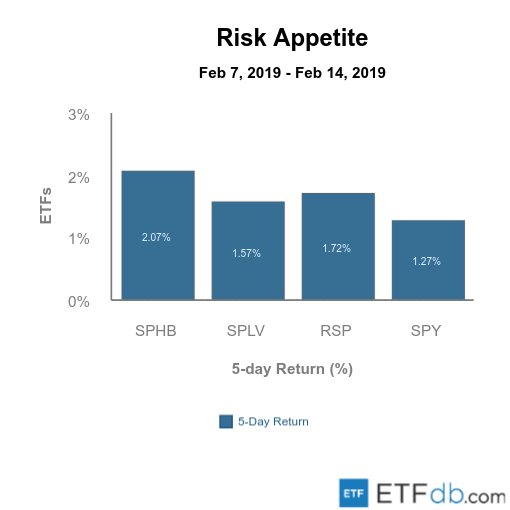

Risk Appetite Review

- Markets rallied again this week.

- Risk assets (SPHB ) reclaimed the best performer’s crown this week, advancing 2.07%.

- Meanwhile, the broad market (SPY ) was the worst performer, jumping just 1.27%.

Sign up for ETFdb.com Pro and get access to real-time ratings on over 1,900 U.S.-listed ETFs.

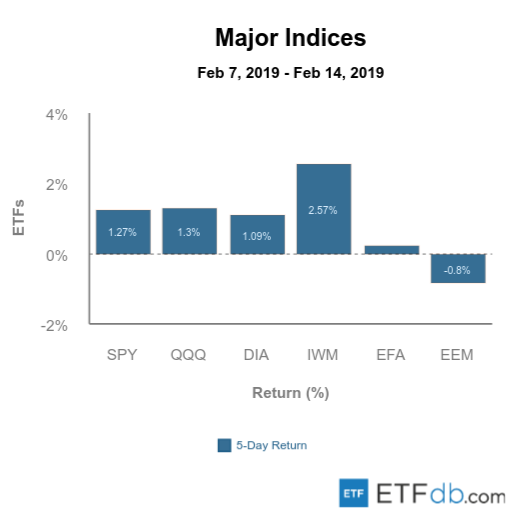

Major Index Review

- Major indexes were mixed.

- Small-cap stocks (IWM ) was again the biggest performer with a gain of 2.57%. (IWM ) rebounded the most in this year’s recovery, despite posting the biggest declines in the market rout at the end of 2018. Small-cap stocks have high leverage, and the Federal Reserve’s indication that it will refrain from raising interest rates further this year has improved investor sentiment.

- At the other end of the spectrum is emerging markets (EEM ), which declined 0.80% for the week, due to falling commodity prices and weakness in the Chinese economy.

To see how these indices performed over the past year, check out ETF Scorecard: February 8 Edition

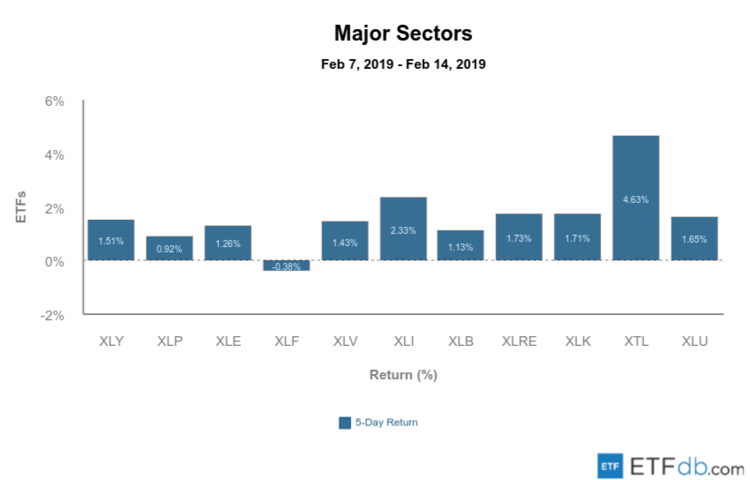

Sectors Review

- Sectors posted mixed performance.

- Financials (XLF ) was the only decliner this week, down 0.38%, as investors dumped banking stocks following the Fed’s signal it will not raise interest rates. Banks benefit from rising interest rates because they can charge a higher interest rate spread.

- The telecom sector (XTL ) gained 4.63% this week, the biggest rise from the pack, as 5G gets closer to industrial implementation. An ongoing spat between the U.S. government and Huawei boosted U.S. telecom equipment providers.

Use our Head-to-Head Comparison tool to compare two ETFs such as (XLF ) and (XTL ) on a variety of criteria such as performance, AUM, trading volume and expenses.

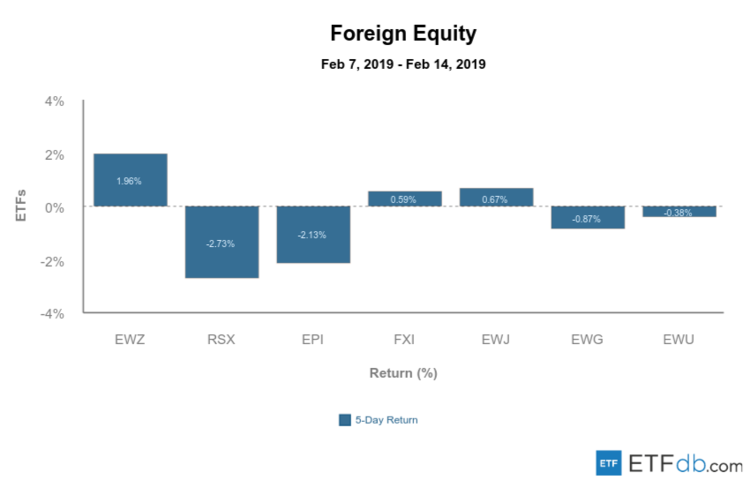

Foreign Equity Review

- Foreign equities were mixed.

- Brazil (EWZ ) gained 1.96% this week, the best performance from the pack. Investors have been flocking to the country’s stocks ever since Jair Bolsonaro promised to make market-friendly changes, including pension reforms, tax reforms and a privatization plan.

- Russia (RSX ), meanwhile, fell as much as 2.73% this week, as the prospect of fresh U.S. sanctions in relation to its meddling in U.S. elections spooked investors.

To find out more about ETFs exposed to particular countries, check out our ETF Country Exposure tool. Select a particular country from a world map and get a list of all ETFs tracking your pick.

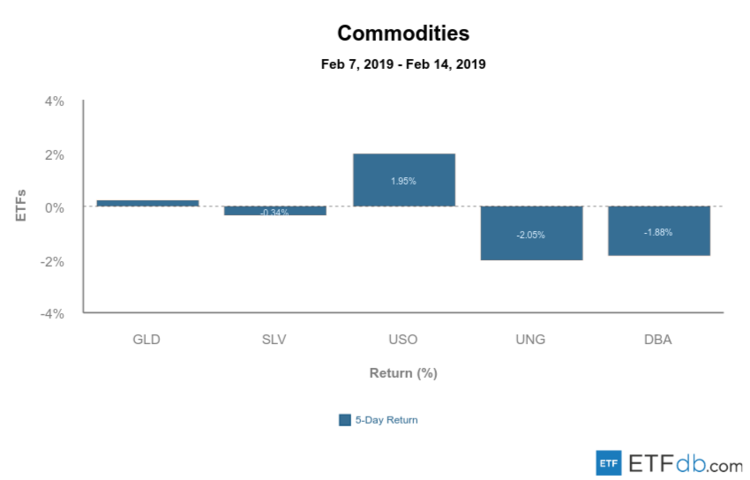

Commodities Review

- Commodities posted mixed performance.

- Crude oil (USO ) gained nearly 2% this week due to U.S. sanctions against Venezuela and Iran and OPEC supply cuts.

- At the same time, natural gas (UNG ) lost more than 2% for the week, despite a harsh winter in certain parts of the U.S.

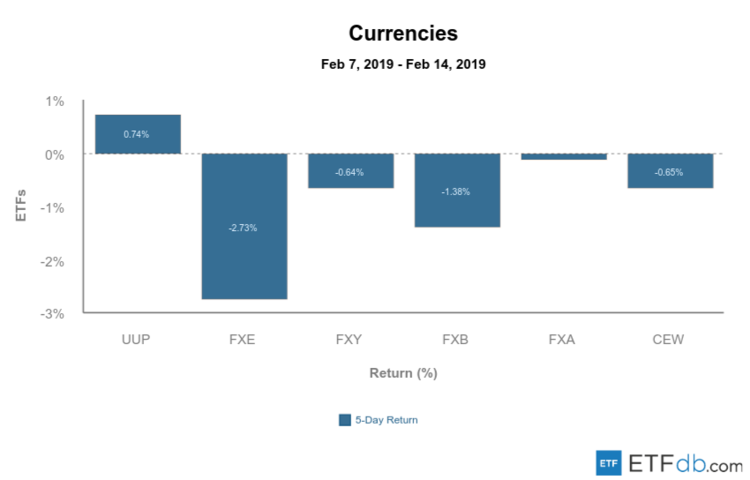

Currency Review

- The euro (FXE ) tumbled 2.73% in the past five days, as a string of negative economic data and Brexit concerns weighed negatively on the shared currency.

- The U.S. dollar (UUP ) is the king with a gain of 0.74%, despite the Federal Reserve’s pledge to keep interest rates at current levels for longer.

For more ETF analysis, make sure to sign up for our free ETF newsletter.

Disclosure: No positions at time of writing.