For a brief moment, volatility picked up in early August and again in early September. We saw some appetite reappear for low volatility ETFs, which have gotten no love in 2024.

A fund like the Invesco S&P 500 Low Volatility ETF (SPLV ), a strategy that owns the 100 least volatile stocks in the S&P 500, saw net asset flows turn modestly positive since Aug. 1 as investors refocused on risk management amid market turbulence. This is a fund that entered August with more than $1.5 billion in net outflows since January 2024. That made us stop and take notice, wondering if the money coming was signaling a meaningful change in investor behavior.

The question we are now asking is whether that change suggests a near-term, tactical opportunity in low volatility ETFs.

Risks abound, that’s for certain. There’s plenty of uncertainty ahead clouding market outlooks, from macroeconomic, geopolitical, and electoral perspectives, to name a few. Seasonally there’s a tendency to see a pickup in market volatility in September and October. That’s something that could underpin demand for low vol ETFs.

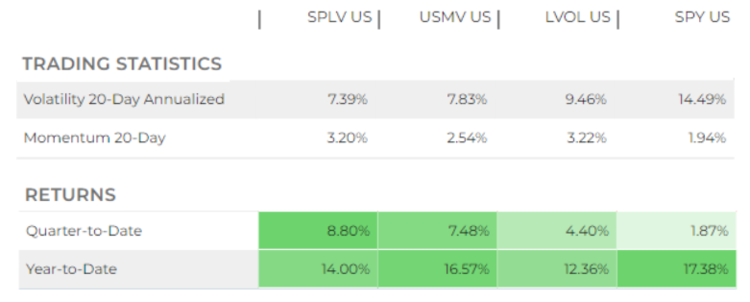

When we look at trading and return statistics, we see that in recent weeks, the low vol trade has delivered outperformance relative to the S&P 500. Consider how SPLV and the American Century Low Volatility ETF (LVOL ) — two examples of low vol plays — as well as the popular iShares MSCI USA Minimum Volatility ETF (USMV ), have stacked up versus the SPDR S&P 500 ETF Trust (SPY ) since July 1. They have delivered better returns, lower volatility, and enjoyed stronger momentum relative to the benchmark. SPLV even forged a new intraday record high earlier this month.

If recent performance were any indication of future results, we could say it’s been a strong quarter for low vol ETFs thus far. So prospects look good going forward. But we know it’s not that simple.

Looking for Clues in VIX Futures

Looking at the VIX tells a far less clear story about the low vol factor opportunity right now.

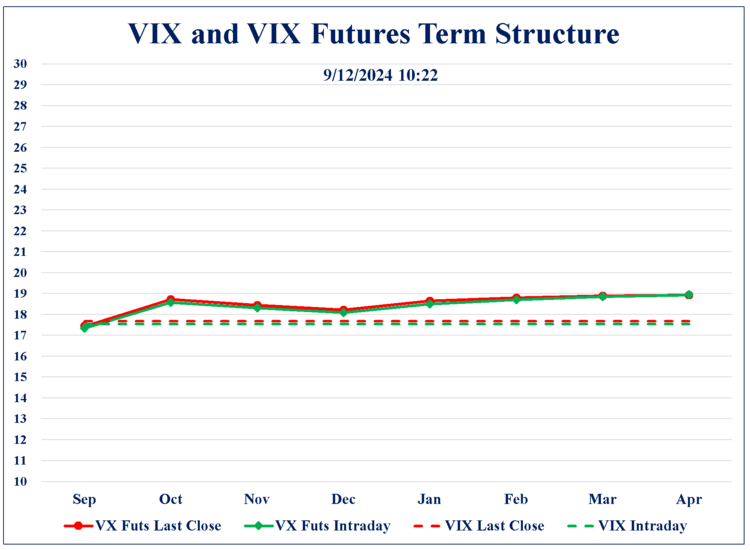

Consider the VIX futures term structure, charted below. According to advisor and volatility expert Jim Carroll, known in social circles as the @vixologist, it’s “flat as a pancake.”

The futures term structure — the curve — holds two important clues about the state of things. The first is tied to the shape of the curve itself. The second is tied to the absolute level of the VIX.

A flat, “pancake”-like curve tells us investors aren’t really too nervous about what the future holds as much as they’re concerned about the here and now. All eyes are on the Fed’s next move, the impact on the economy and markets, the upcoming election, China, etf. But according to Carroll, the flatness of the curve suggests we’re nervous now. But expect most of these key “unknowns” to be “knowns” by early 2025.

“Until we get beyond some of these key events, no one is selling the front end of the curve,” he said. He noted that a typical trade this time of year consists of shorting the front end and going long the back end of the VIX curve. But right now, no one is bidding up insurance for a later date in the same way no one is really selling near-term insurance.

Temperature Check for Vix

The second interesting thing the VIX futures curve tells us is that if we were to put a temperature on our level of nervousness, we are not exactly running very hot. On an absolute level, the VIX is currently sitting below 20. That is historically low for this time of year, especially in the face of so much uncertainty. The unknowns aren’t yet known. But we seem to be relatively comfortable with them. They are well-understood, to quote Carroll.

“This time of year tends to be hurricane season in volatility markets,” he explained. “But what the VIX futures market is telling us is that people aren’t terribly worried about the first part of 2025.”

That said, he noted, investors need to beware. It’s in periods like this when we can see volatility suddenly go up or down. And there’s a tendency for these sharp moves to “cluster.” That’s much like what we’ve experienced in early August and early September.

“As we get answers to all of these questions, from Fed action and messaging, election and policy — as things fall into place — we will get clearer direction," he said. "But what direction? I don’t know. No one does.”

So, what does this mean for low vol ETFs?

Outlook for Low Vol ETFs

Risk management never sleeps. And the potential for “clustering in volatility” and appetite for diversification through lower beta portfolios following the massive run-up in growth names could keep these ETFs supported here.

But, like any other ETF category, it’s important to remember there are many funds from different providers delivering many ways to access the low vol factor. Do a little digging if you’re going to jump in.

Consider that, SPLV, which picks the 100 least volatile names from the S&P 500, has financials, consumer staples, industrials, and utilities as top sector exposures. From a style perspective, large-cap value represents about 22% of the portfolio’s allocation versus 2% for large-cap growth. It’s names like Berkshire Hathaway, Coca-Cola and Walmart that are found among top 10 positions.

USMV's Secret Sauce: Mixing Stocks Together

It could be that its strong performance recently is tied to its tilt toward value and defensive sectors, and not just its focus on low volatility as a factor. By contrast, the actively managed LVOL, for example, looks to deliver a lower volatile ride in a portfolio heavily tied to information technology. That’s about 1/3 of the portfolio. It’s a somewhat surprising mix of names led by the likes of Microsoft, Apple, and Cisco. However, the strategy delivers on low-voltage access by focusing on companies with strong fundamentals, profitability, and low long-term business risks.

The biggest ETF in the low vol category is not even purely low vol. It’s minimum vol. iShares’ USMV can actually own highly volatile stocks. But its secret lies in mixing stocks together, looking for relative lower volatility among similar stocks within sectors. The fund tries to stay sector-aligned with the broader market, but it delivers a lower volatility ride that’s different from SPLV and LVOL.

These are just some examples of the many ways in which investors can access the low vol factor through ETFs. Ready to revisit this segment? Start your due diligence here in our comprehensive list of low vol ETFs.

For more news, information, and analysis, visit VettaFi | ETFDB.