The latest employment report showed 254,000 jobs were added in September. That’s well above forecasts of the expected addition of 147,000 new jobs. Meanwhile, the unemployment rate ticked lower to 4.1%.

Here is an excerpt from the Employment Situation Summary released this morning by the Bureau of Labor Statistics:

Total nonfarm payroll employment increased by 254,000 in September, and the unemployment rate changed little at 4.1 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in food services and drinking places, health care, government, social assistance, and construction.

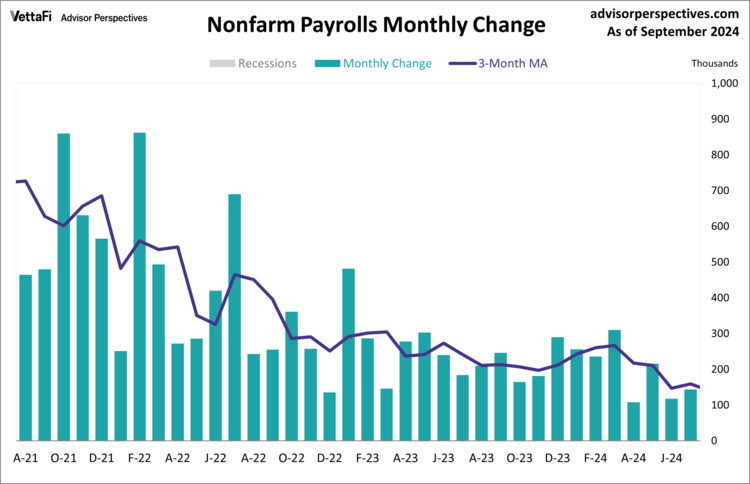

Here is a snapshot of the monthly change in nonfarm employment over the last 3 years.

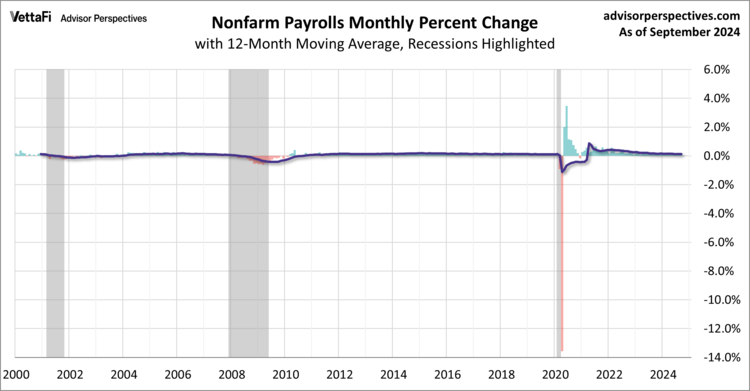

For another view, here is the monthly percent change in nonfarm employment since 2000. We’ve added a 12-month moving average to highlight the long-term trend. The latest 12-month moving average is at 203,000, unchanged from the prior month and its lowest level since March 2021.

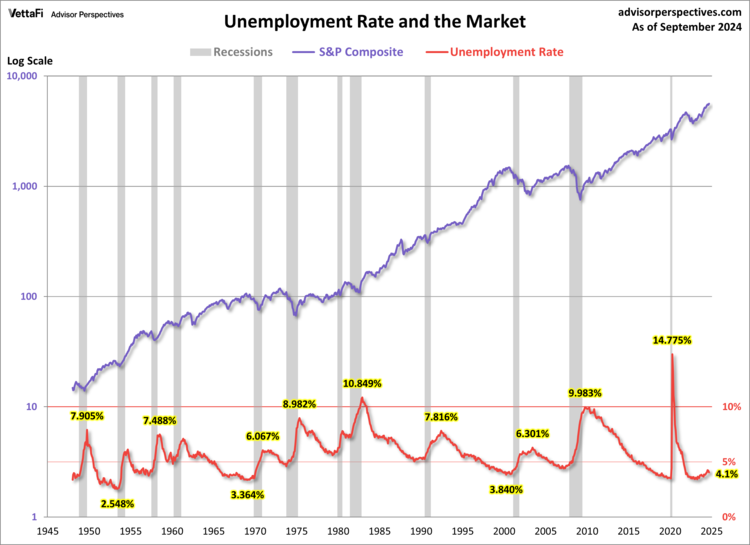

The next chart shows the pattern of unemployment, recessions and the S&P composite since 1948. Unemployment is usually a lagging indicator that moves inversely with equity prices (top series in the chart). Note the increasing peaks in unemployment in 1971, 1975 and 1982. The mirror relationship repeats itself with the previous bear markets. The COVID pandemic briefly showed the same type of relationship between equities and unemployment, though the impact was temporary and irrational exuberance took over once again.

The latest unemployment rate is at 4.051% (to three decimal places).

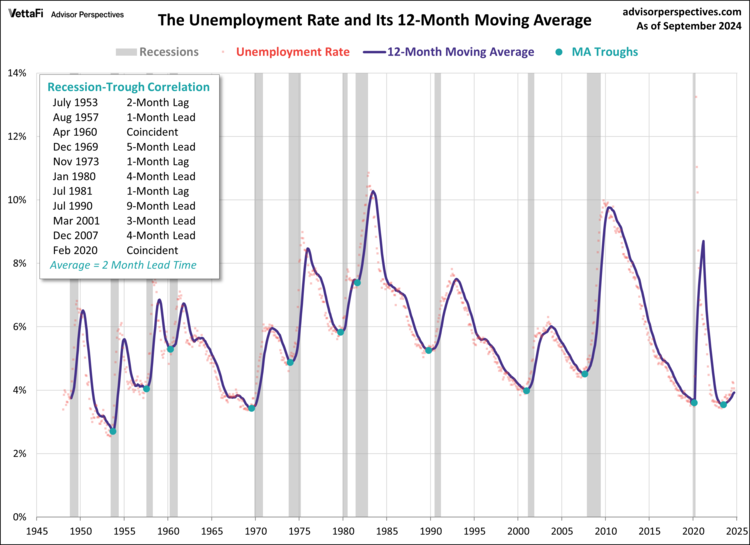

Now let’s take a look at the unemployment rate as a recession indicator or more specifically the cyclical troughs in the unemployment rate (UR) as a recession indicator. The next chart features a 12-month moving average of the UR with the troughs highlighted. The current unemployment rate of 4.05% (to two decimal places) is above the latest 12-month moving average of 3.92% (to two decimal places).

As the inset table shows, the correlation between the MA troughs and recession starts is remarkably close. The latest trough in the series occurred 12 months ago in June 2023, where the 12-month moving average of the unemployment rate fell to its lowest level since January 1970.

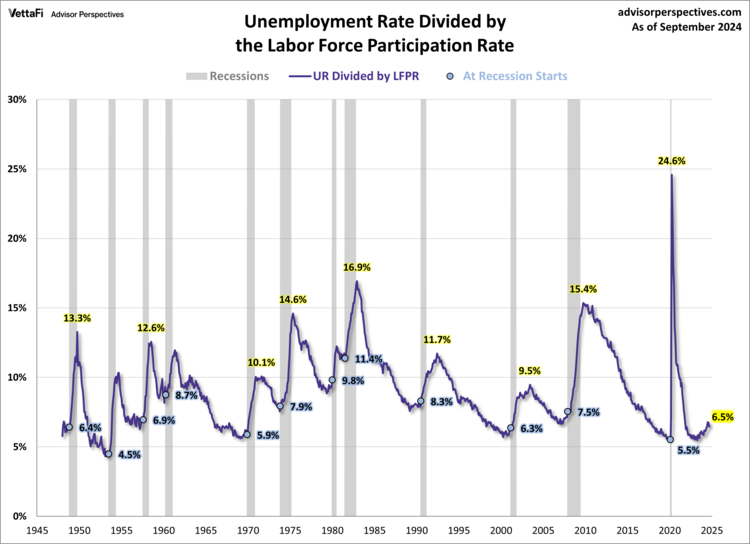

Here’s another chart to illustrate the reality of the unemployment rate – the unemployment rate divided by the labor force participation rate. We are currently at 6.5%, down from 6.7% the previous month.

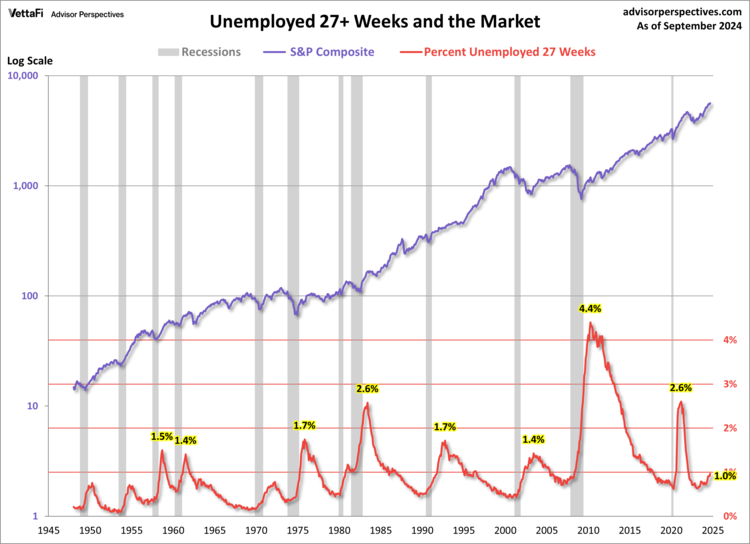

The next chart shows the unemployment rate for the civilian population unemployed 27 weeks and over. This rate has fallen significantly since its 4.4% all-time peak in April 2010. After the COVID pandemic, the rate reached as high as 2.6% but has since fallen. The unemployment rate for the civilian population unemployed 27 weeks and over is now at 0.9%, unchanged from the previous month and the highest level since March 2022.

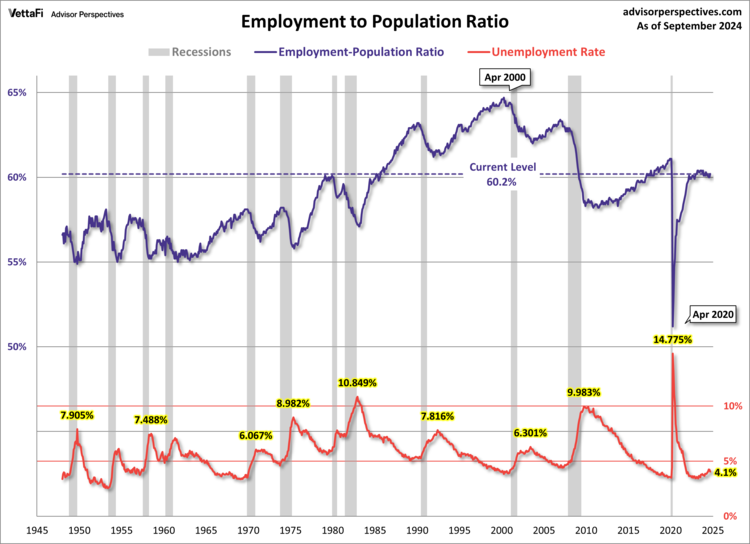

The next chart is an overlay of the unemployment rate and the employment-population ratio. This is the ratio of the number of employed people to the total civilian population age 16 and over.

The inverse correlation between the two series is obvious. We can also see the accelerating growth of women in the workforce and two-income households in the early 1980s. Before the COVID pandemic, the employment-population was range-bound between 54.9% and 64.7% — the lower end harkens back to when Eisenhower was president of a country of one-income households, the Korean War was still underway, and rumors were circulating that soft drinks would soon be sold in cans. In April 2020, because of the global pandemic, we saw the employment-population ratio drop to its lowest level in series history to 51.3%. Since then it has been gradually climbing to its pre-pandemic range, with the latest ratio at 60.2%, up slightly from the previous month.

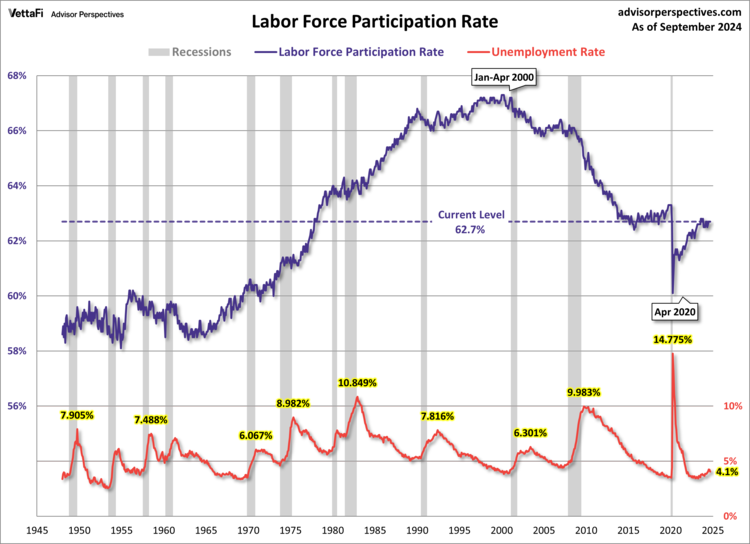

For a confirming view of the secular change the US is experiencing on the employment front, the next chart illustrates the labor force participation rate. We’re at 62.7%, unchanged from the previous month.

The employment-population ratio and participation rate will be interesting to watch going forward. The first wave of boomers will continue to be a downward force on this ratio. The oldest of them were eligible for early retirement when the Great Recession began, and the transition of the boomer cohort to full retirement age won’t end until 2030.

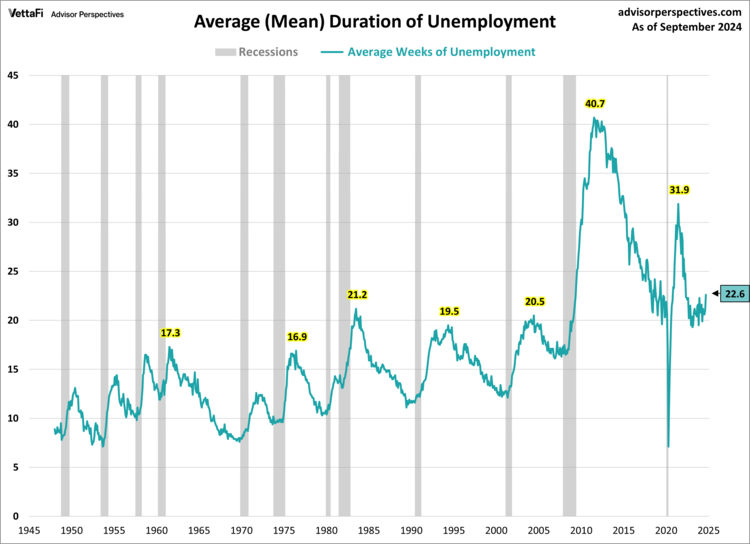

What is the average length of unemployment? As the next chart illustrates, we are perhaps seeing a paradigm shift. This shift is the result of global outsourcing and efficiencies of technology. The latest monthly figure shows the average duration is at 22.6 weeks, well below the 40.7-week all-time high in late 2011.

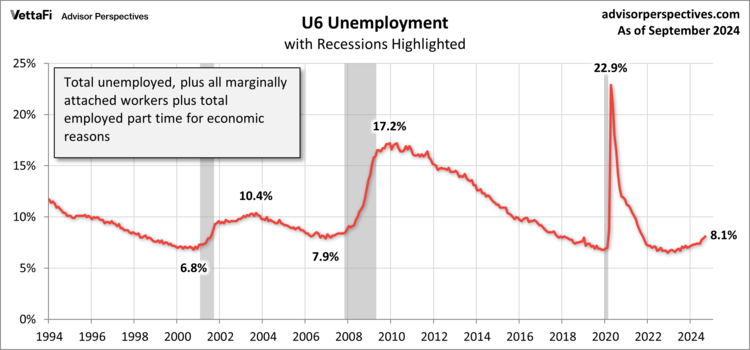

The Bureau of Labor Statistics’ broadest measure of unemployment is the U6 series. This series includes the total unemployed, plus all marginally attached workers plus total employed part-time for economic reasons. This series dates from 1994.

The U6 series is currently at 8.1%, up from 7.9% the previous month and the highest level since December 2022.

Notes: The start date of 1948 in the charts above was determined by the earliest monthly employment data collected by the Bureau of Labor Statistics. The best source for the historical data is the Federal Reserve Bank of St. Louis.

The S&P Composite is a splice of the S&P 500, which started in 1957, with the S&P 90, which preceded it. ETFs associated with the S&P 500 include: iShares Core S&P 500 ETF (IVV ), SPDR S&P 500 ETF Trust (SPY ), Vanguard S&P 500 ETF (VOO ), and SPDR Portfolio S&P 500 ETF (SPLG ).

Here’s our list of monthly employment updates:

Civilian Labor Force, Unemployment Claims, and the Business Cycle

Ratio of Part Time and Full-Time Employment

Workforce Recovery Since Recession

Originally published on Advisor Perspectives

For more news, information, and analysis, visit VettaFi | ETFDB.