Money market mutual funds have long been a popular cash management tool for investors looking to park cash short-term, while preserving capital and picking up some return and yield. Now, there are money market ETFs for that, too.

Earlier this month, my colleague, Kirsten Chang, highlighted the arrival and appeal of money market ETFs. Texas Capital, led by Ed Rosenberg, pioneered the category, with the launch of the Texas Capital Government Money Market ETF (MMKT ) last year. BlackRock followed with two competing ETFs, the iShares Government Money Market ETF (GMMF ) and the iShares Prime Money Market ETF (PMMF ).

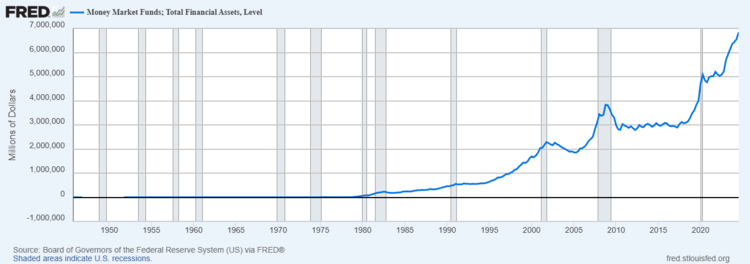

The potential asset growth for these funds is big, if you consider the pool. Assets in money market mutual funds have been growing significantly in recent years. That’s attributed to strong appetites for cash-like tools as well as higher rates, juicing up yields on the short-end of the curve where risk is muted.

At the end of 2024, they topped $6.8 trillion, according to Federal Reserve data. Look at that upward slope on the chart below. These new ETFs are looking to capture some of those assets, displacing them from mutual funds.

Product Choice

One of the challenges of that effort is that money market mutual funds and ETFs are very similar from a regulatory perspective. They all must abide by several rules aimed at protecting the safety-net, cash-like aspect of these strategies. They all invest in short-term high quality debt securities; they have very little sensitivity to duration and interest rate risk; they are very liquid.

So, why choose one over the other? The answer is that both are great tools, and serve investors well. But the ETF structure does bring a few unique characteristics to this type of cash management approach. Consider three:

#1. Tradability & Liquidity = Cash at Hand

ETFs trade throughout the day, and getting in and out of a position is easy, unlike mutual funds.

While transacting in a money market fund may not be the ultimate goal, with an ETF you can. And what’s more, you can immediately turn around and redeploy that cash, reallocating into another part of the market. The ETF wrapper offers liquidity at hand.

In practice, it may not matter too much for an investor who’s cashing out, say, $5,000 to fund a short-term need. But it could be meaningfully valuable for an advisor who’s moving, say, $100 million from cash into an equity position on a given day. Markets can move fast, and tradability means flexibility to transact and put money to work when best suits you.

#2. Floating NAV = Experience Hurdle

Money market ETFs have floating net asset values (NAVs). This means that the per-share value of the fund relative to its underlying securities and liabilities fluctuates throughout the day to respond to the market.

That’s not entirely unusual. In the mutual fund world, some money market funds — like municipal ones, for example — have floating NAVs as well. But most have a fixed $1 NAV. We associate that with the idea that, in a cash-like instrument, you don’t want to “break the buck.” Going below that $1 mark could trigger investor panic and runs on money.

A floating NAV, however, goes where the market value goes. It better reflects the value of the ETF’s underlying securities, as rates move and markets change. In a money market strategy, a floating NAV should not translate into notably different results for the investor, but it could be an adoption hurdle for traditional money market (mutual) fund investors, because that’s a departure from what they know.

As one asset manager put it, a floating NAV could “feel like” volatility in an instrument that’s perceived as practically risk free, meant to offer stability. That could require some getting used to.

In the prospectus for MMKT, the floating NAV is explained this way: “Because the share price and NAV of the Fund will fluctuate, when shares are sold on the Exchange (or redeemed, in the case of an Authorized Participant), they may be worth more or less than what was originally paid for them.”

#3. Access = Democratization

ETFs are a democratizing investment vehicle. They are typically low cost, easily accessible across multiple platforms to anyone with a brokerage account, and they don’t have investment minimums or require investor accreditation. All of that remains true with a money market ETF.

In the case of MMKT, GMMF and PMMF, each cost 0.20% in expense ratio, or $20 per $10,000 invested. In the mutual fund world, fees range. Vanguard seems to be the low cost provider, with fees in some of its money market funds below that level. But outside of Vanguard — in platforms like Schwab and Fidelity, for example — money market funds cost over 0.30%. Fees are the only thing you can truly control in an investment — the more you pay, the less you keep.

Why Now?

Money market ETFs are paying an attractive yield — 4.3% in the case of MMKT, which is just slightly above that of BlackRock’s money market ETFs, both yielding above 4% as well. Higher short-term rates have been a boon for the category. That meant, when MMKT launched in 2024, yields for the ETF had a five-handle.

The prevailing expectation is that rates will move downward from here. That’s not a great scenario for money market fund yields. However, a cautious Federal Reserve, ready to hold rates steady as a new administration gets its footing and inflation finds its way back into the conversation, should keep the near-term outlook for cash management tools positive.

What’s more, growing uncertainty about growth and the investment opportunity set could also compel investors to keep cash at hand, sidelined in money market funds and ETFs until they are ready to commit to something else. We keep looking for the great redeployment of cash, but assets in money market funds are proving really sticky. And now, there are ETFs for that as well.

For more news, information, and strategy, visit ETFDB.