When markets move, we can learn a lot from the outperformers. But we can also learn a lot from the underperformers — and maybe even find opportunities. This week’s note takes a look at some of the biggest underperformers in ETFs so far this year and a back-of-the-envelope look at cheapness.

Volatile markets can create opportunities

When markets are volatile (see last week’s note), there are three (rational) options for investors to take. Some investors may take all three. The first option is to leave everything alone. After all, short-term movements are often smoothed in the long term. The second option is to add more diversifiers to hedge performance. This could include asset classes like fixed income or gold or strategies like defined outcome. The third option is to embrace the volatility and add on opportunities. This can be short-term, extreme bets (e.g., leveraged products) or longer term (e.g., simply buying the dip).

Defining cheapness can be difficult

I want to talk more about the latter (buying the dip), because many investors are using the pullback as an opportunity. But how do you know what’s actually cheap and whether it’s worth buying now or waiting?

From a fund perspective, there are some layers to valuation. Certain funds — particularly closed-end funds — have large valuation gaps between market price and net asset value that allows for buying at discounts and selling at premiums. This is less relevant from an ETF perspective, but still exists.

There are several popular metrics that apply to equities that also apply to ETFs. Often that involves looking at valuation multiples like price-to-earnings (P/E) or EV/EBITDA. These are relative, which means they need to be viewed in context of either historical levels or peer levels.

But the truth is that valuation methods don’t always work. While historical valuations are based on some fact, forward-looking valuations are not only affected by forward-looking estimates, but also sentiment. Sentiment is almost impossible to predict.

So, for simplicity’s sake, we’ll just use returns to address cheapness. When using returns, it is still important to view these relatively. For example, just because an ETF is down 50% doesn’t mean the ETF is cheap. Cheapness is relative — and it’s relative based on several factors. The first question to ask is, is it relative based on its peers? The second question is, is it cheap based on its historical pricing?

Three interesting areas in ETFs

The first few paragraphs were my long-winded way of saying that sometimes underperformers can be as interesting (or even more interesting) than outperformers. Three categories of underperformers really stood out to me (note that these categories were all down prior to Liberation Day). I will leave it to the reader to decide if these are truly cheap or not, but all have the potential to be attractive to the right investor.

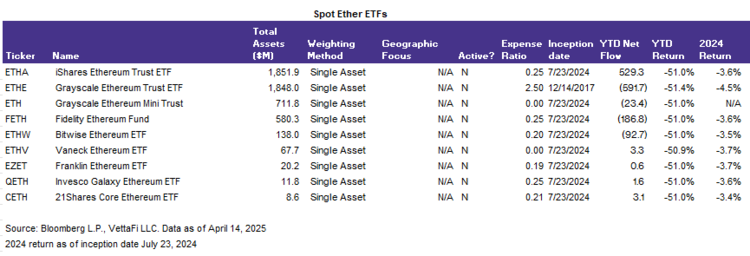

Ether:

At the bottom of the list of 4,000 ETFs are spot ether ETFs. The iShares Ethereum Trust ETF (ETHA ) and the Grayscale Ethereum Trust (ETHE ), for example, are both down over 50% year-to-date. Prices were pressured in early 2025 due to macro headwinds which evolved into a high volatility market. If tech stocks (including the much loved Magnificent Seven) pulled back, you can imagine why ether pulled back. Unlike its more popular cousin bitcoin, ether doesn’t really have a large inflation element to its story. Bitcoin has (debatable) characteristics as digital gold (but nonetheless, those characteristics are there). Ether, on the other hand, is more of a risk asset and has been trading lower along with the broader equity market.

There’s also been a lot of other attention to other tokens — but arguably more attention to crypto may also benefit all types of crypto ETFs. This has been a little bit hard to predict lately since the market has been more concerned with impact on the broader economic impacts. Derivatives-based ETFs for Solana and XRP were launched somewhat quietly — the Solana ETF (SOLZ ), the 2x Solana ETF (SOLT ), and the Teucrium 2x Long Daily XRP ETF (XXRP ).

Cannabis:

Performing slightly higher than ether is a small yet memorable category: cannabis ETFs. The largest ETF in the space — the AdvisorShares Pure US Cannabis ETF (MSOS ) and the Amplify Alternative Harvest ETF (MJ ) is down around 40% YTD. There’s not real evidence as to why there was an extreme pullback this year. But there simply hasn’t been a lot of positive news in this space and it has seen extreme drops over the past several years.

To clarify, I do like the investment thesis behind cannabis. I think it’s a good thematic story about untapped growth market when you think about the medicinal use (and also monetizing the recreational use). But unfortunately, there’s too much red tape and too many moving parts when it comes to both state and federal regulations. These products, however, still have a small but strong following — net inflows have been mostly despite the YTD underperformance.

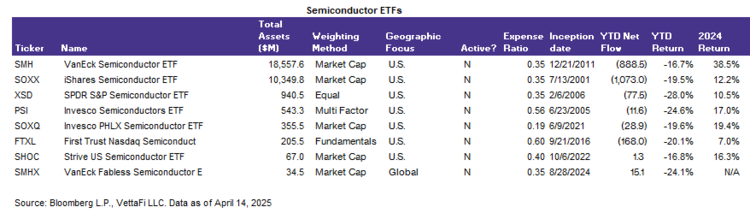

Semiconductors:

Uncertainty is the word of the year, and there is a lot of uncertainty surrounding tech supply chains. Initially, Apple iPhones were going to see tariffs implemented — there was talk of whether we’d have to pay $3,000 for an iPhone or be faced with inserting microscopic screws into the iPhones here in the U.S. Now iPhones are exempt. On the flip side, Trump initially declared that semiconductors would be free from tariffs, but now there seems to be some uncertainty. Regardless, there will be some sort of tariff on the supply chain and some sort of disruption that doesn’t bode well for semiconductor stocks in the near term.

This has caused a pullback in semiconductors prices. Stocks like Nvidia (NVDA), Taiwan Semiconductor (TSM), and Broadcom (AVGO) were some of the most well-loved stocks of 2024. And popular semiconductor ETFs like the VanEck Semiconductor ETF (SMH ) were up almost 40% year to date. This year, the pullback has caused SMH to fall 17%. Other ETFs like the SPDR S&P Semiconductor ETF (XSD ) have fallen even further and are down 28%.

Near term, there are a lot of concerns. But still, it’s hard to imagine that this is the end for semiconductors. Semiconductors have been a strong theme for years prior to tariffs or even the artificial intelligence boom. Computers, cellphones, televisions, our cars all use semiconductors.

For more news, information, and strategy, visit ETFDB.