The first quarter of 2026 is shaping up to be one marked by heavy volatility. Sticky inflation, geopolitical conflicts, potentially overstretched valuations in mega-caps, and a weakening U.S. jobs report all helped to spike the VIX Index 40% in the first week of March alone. However, this creates ample opportunities for investors to embrace low-volatility ETFs amid the storm.

Because of these increased market fluctuations, investors are rotating from high-beta growth stories into low-volatility strategies. The Invesco S&P 500 Low Volatility ETF (SPLV ) and the iShares MSCI USA Min Vol Factor ETF (USMV ) capture this defensive pivot to perfection.

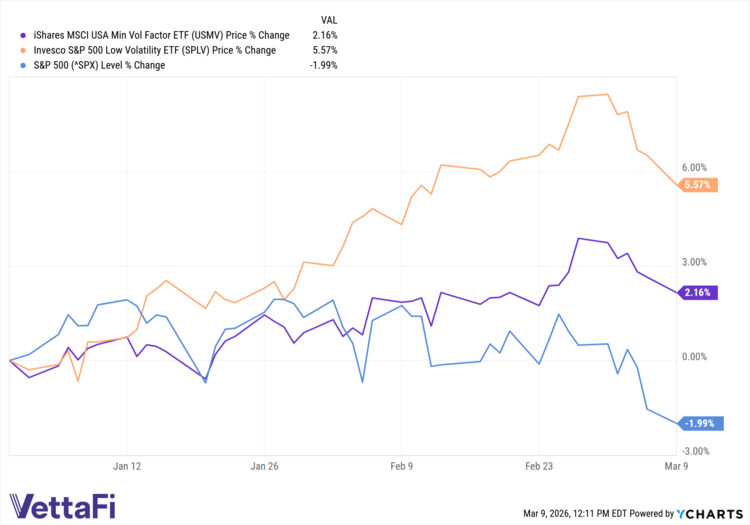

The strategy of both funds is simple — dampen the shock of any market bumps investors may encounter. So far this year, they’ve done just that. Both ETFs are in positive territory compared the S&P 500.

How are both able to weather the storm?

SPLV: Low-Vol Defense

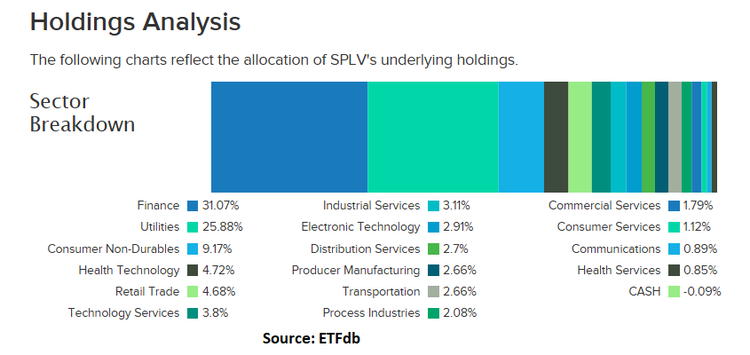

With an expense ratio of 25 basis points, SPLV tracks the 100 stocks within the broader S&P 500 that have exhibited the lowest realized volatility within the past 12 months. To ensure investor exposure to the latest volatility shock absorbers, the index tracks the S&P 500® Low Volatility Index (Index). The fund is then rebalanced and reconstituted in February, May, August, and November.

The fund doesn’t include any sector constraints. That means that investors get diversification across the board. The fund is currently exposed primarily to finance (31%) and utilities (26%), thereby avoiding a tech-led route. While the fund’s main motive is to lower volatility, it can also capture any upside in its sector exposure. Its almost 6% gain this year evidences that.

USMV: Optimized Minimum Volatility

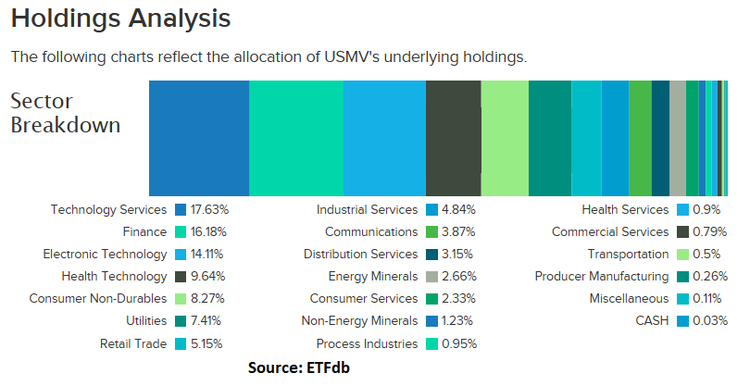

At an expense ratio of just 15 basis points, USMV’s complex mathematical model runs its low-volatility portfolio. The “sum of the parts is greater than the whole” approach results in a diversified mix of names exhibiting low volatility in the aggregate as opposed to individual stocks with low volatility profiles.

Given its strategy, USMV’s market resilience and gain of 2% year-to-date is driven by selection criteria, mathematical optimization, and a pivot towards more quality-oriented tech names as opposed to growth. As such, holdings will be primarily in the technology services sector (almost 18%). Meanwhile, the rest is spread among finance, electronic technology, health tech, consumer non-durables, utilities, and others.

The Performance Verdict

Up 40% in the first week of March and over 80% for the year, the VIX is flashing signs to investors that low-vol strategies need a closer look. The goal of funds like SPLV and USMV is to simply lose less than the broader market. In this case, though, they’re also up for the year.

The choice between the two funds can come down to various factors. While SPLV has been the better performer this year, it also comes in at 10 basis points higher than USMV. Those looking for heavier exposure to defensive sectors like utilities may opt for SPLV. Those looking for a more diversified, optimized approach to lower volatility will appreciate USMV.

For more news, information, and strategy, visit ETFdb.