A prospectus can be an intimidating document for investors to read.

The SPDR S&P 500 ETF (SPY ) prospectus , for example, is an 86-page document divided into 32 different sections covering everything from dividends to a code of ethics. While many research tools provide a good summary of this information, including ETFdb, it’s important for investors to dig into a few areas in order to ensure that they’re not making any potentially costly mistakes.

In this article, we’ll look at three key tips for ETF investors to consider when reading a prospectus in order to avoid some easy to miss mistakes.

Look at Costs in Context

Most investors are aware of the impact that expenses can have on long-term returns, but few realize the magnitude of this impact. According to Vanguard, a $10,000 investment with a 1.2% expense ratio held for 50 years with a 6% annual return will result in $547,612 of returns kept and $616,296 of returns lost to fees. This is because fees taken early on reduce the potential for compounding over time, which creates very large opportunity costs.

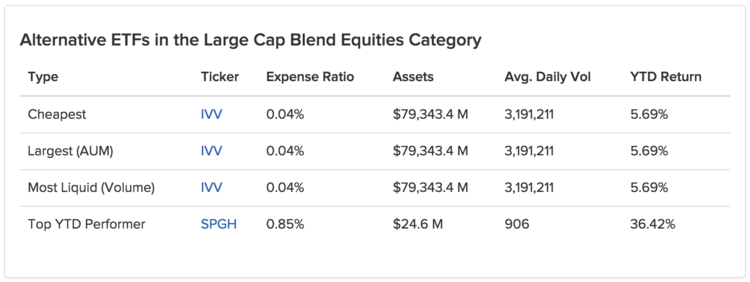

The Fees & Expenses section of a prospectus outlines these fees, but it’s important to compare and contrast these costs on a relative rather than absolute basis. For example, a 0.5% fee may seem low when looking at the hypothetical examples in a prospectus, but a similar ETF could offer a much lower 0.15% expense ratio. Investors can quickly find these comparisons using ETFdb’s Alternative ETFs section, which identifies the cheapest ETFs in a given category.

In addition to expense ratios, it’s important for investors to look into portfolio turnover. Higher turnover can result in increased commission expenses that aren’t included in the fund’s expense ratio. Investors can find turnover information in an ETF prospectus, although it may be broken down in a different section than Fees & Expenses in some cases. In general, investors should seek out index funds with low turnover in order to mitigate these risks.

Consider Tax Complexity

The introduction of ETFs made it easier than ever for investors to buy and sell funds, but it also made it easier for them to ignore complexity. For example, commodity ETFs may seem like a great idea to hedge a portfolio, but they’re often structured as ‘limited partnerships’ that require shareholders to report the fund’s gains and losses on a Schedule K-1 rather than a 1099, which could add some complexity to tax preparation and planning.

The Tax Information section of a prospectus spells out the tax implications associated with a given ETF. If the fund uses futures contracts, information on its K-1 statement will be listed for investors to consider as well. There may also be differences in how various types of funds are taxed. For instance, MLP ETNs are taxed at individual income tax rates, while MLP ETFs are taxed as a return of capital with a portion subject to corporate income tax rates.

Finally, investors should watch out for high turnover due to its potential tax implications. A fund with a high turnover rate may rack up a lot of short-term capital gains that will be taxed as ordinary income rather than long-term capital gains. Index ETFs aren’t immune to these dynamics either, since some indexes are rebalanced more frequently than others, which means that investors should carefully read the prospectus to understand the nuances.

Know Differences in Returns

The return on investment may seem like a pretty straightforward concept, but there are many factors that investors should consider when looking at them.

The most important thing to remember is that past performance doesn’t guarantee future results. After an extended period of low interest rates, bond funds may have one- and three-year returns that look very compelling, but it’s unlikely that this performance will continue if interest rates begin to rise. It’s important for investors to read the Performance Data section with a grain of salt, and understand that more context may be required.

There are also many different kinds of returns outlined in these prospectuses. The net asset value (NAV) performance is the return on the underlying assets (e.g. stocks or bonds), whereas the market value performance is the return on the ETF’s price. Some ETFs trade at a discount to NAV, which means that the NAV return may be lower than the market return. Fixed income investments also have several different types of yields to consider.

Finally, it’s important for investors to remember that risk-adjusted returns are the metric that matters most. A high-return ETF may seem appealing on the surface, but if it has significant risks involved, it may not be appropriate for an investor’s portfolio. A great calculation to adjust estimated returns for risk is the Sharpe Ratio, which looks at the average return earned in excess of the risk-free rate per unit of volatility or risk.

The Bottom Line

ETFs are an easy way for investors to build exposure to any asset class, but it’s just as easy to miss some of the potential risk factors. While reading a prospectus may be intimidating, investors should consider looking out for these three factors before investing in order to avoid making potentially costly mistakes that can easily be avoided.