The ever-expanding ETF universe continues to spawn innovative financial instruments, providing self-directed investors access to previously hard-to-reach strategies and asset classes. For fixed-income investors, the roster of exchange-traded funds has grown to include products that virtually mimic actual bond investing. That is to say, investors can now more closely replicate the bond investing experience while still taking full advantage of the cost efficiency and ease-of-use benefits associated with the ETF product structure.

We’re talking about target-maturity date bond ETFs, which span across the corporate, municipal, and high-yield debt markets. Below, we’ll take a closer look at how this increasingly popular breed of bond ETFs differs from traditional fixed-income funds by examining the real-life example of a BulletShares fund that matured in 2013.

The Difference Between Fixed-Income and Target-Maturity Funds

For starters, let’s consider the key difference between traditional fixed-income funds and target-maturity bond ETFs. Traditional bond funds, such as the iShares iBoxx Investment Grade Corporate Bond ETF (LQD ), operate by tracking a constant maturity index that rolls over debt holdings based on a minimum maturity rule. In essence, these types of bond funds move out of debt securities once their maturity reaches a certain point and buy into new debt securities with a maturity date further out in the future [see Q&A With Matthew Patterson: Are Bond ETFs Broken?].

Target-maturity bond funds, such as the BulletShares lineup issued by Guggenheim, operate by tracking an index comprising debt securities that mature in a defined year in the future. These bond funds behave like actual bond investments; once an investor purchases a target-maturity bond ETF, they receive coupon payments over the life of the debt note, as well as a return of capital once the defined maturity date is reached.

Target-maturity date bond ETFs separate themselves from traditional bond ETFs because they offer a scheduled return of the initial investment (think of it as the principal) upon maturity. Simply put, target-maturity bonds have a known termination date, whereas traditional bond ETFs operate indefinitely.

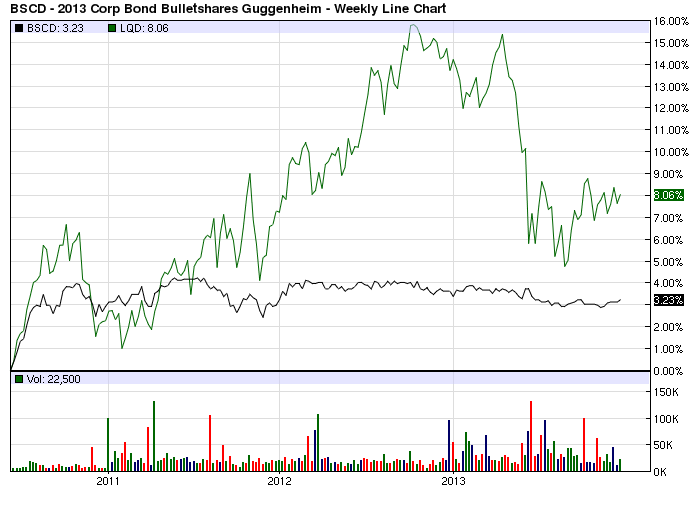

Examining the Life Cycle of the BulletShares 2013 Corporate Bond ETF (BSCD )

Now let’s consider a real example of how these two breeds of bond ETFs behave. The chart below compares the performance of LQD and the BulletShares 2013 Corporate Bond ETF (BSCD) during its lifetime. The latter target-maturity date bond ETF was launched on June 7th, 2010, and matured on December 30th, 2013.

Right off the bat, it’s quite clear that LQD was far more volatile than BSCD during its lifetime. The reason behind this is straightforward: BSCD was launched in mid-2010 with a maturity date at the end of 2013, giving it a much lower duration than LQD, whose underlying portfolio comprises debt securities with maturities well past three years. Unlike a traditional bond ETF, which maintains a relatively stable duration, the interest rate risk associated with a target-maturity date ETF should decline over time as the given maturity date approaches.

Next, let’s consider the dividend component of target-maturity bond funds. The chart below illustrates the interest payments that BSCD made to investors during its lifetime.

The distributions fluctuated from month to month, but overall they decreased as the fund’s maturity date neared. This is because more and more of the underlying debt securities matured, decreasing the size of the distributions as the cash level in BSCD’s underlying portfolio appreciated [see also ETFdb’s Better-Than-AGG Total Bond Market Portfolio].

The below is an aggregated representation of BSCD’s distributions.

BSCD’s Returns

Over its lifetime, BSCD paid out a total of $0.847 per share in dividends. Now let’s re-consider its performance. The line chart above shows it returned just over 3% from inception until maturity. However, this figure does not account for the distributions that it made during its lifetime. When we factor in the dividends paid, BSCD’s total returns come out to a much heftier 7.12%. Upon reaching maturity, and its subsequent termination, BSCD returned to shareholders their initial investment in the form of a cash payout.

So what’s the appeal of target-maturity date bond ETFs? If an investor has an upcoming liability, it makes more sense to utilize a bond ETF like BSCD, in lieu of a traditional fund like LQD, because the investment can generate a stream of current income, and will also be repaid upon maturity. Investors can use such a fund to generate a meaningful source of income, while still maintaining the peace of mind that their initial investment will be returned at a pre-determined date in the future when they might need it.

The Bottom Line

Target-maturity date bond ETFs differ from traditional bond funds in a variety of ways. Perhaps the most defining characteristic of these funds is that they have a known termination date upon which the initial investment is returned to shareholders. Along the way, investors receive coupon payments which mimick the cash-flow experience associated with an actual bond investment. As with all financial instruments, be sure you understand all of the risks and nuances associated with this type of product before pulling the trigger.

Follow me on Twitter @SBojinov

[For more ETF analysis, make sure to sign up for our free ETF newsletter]

Disclosure: No positions at time of writing.