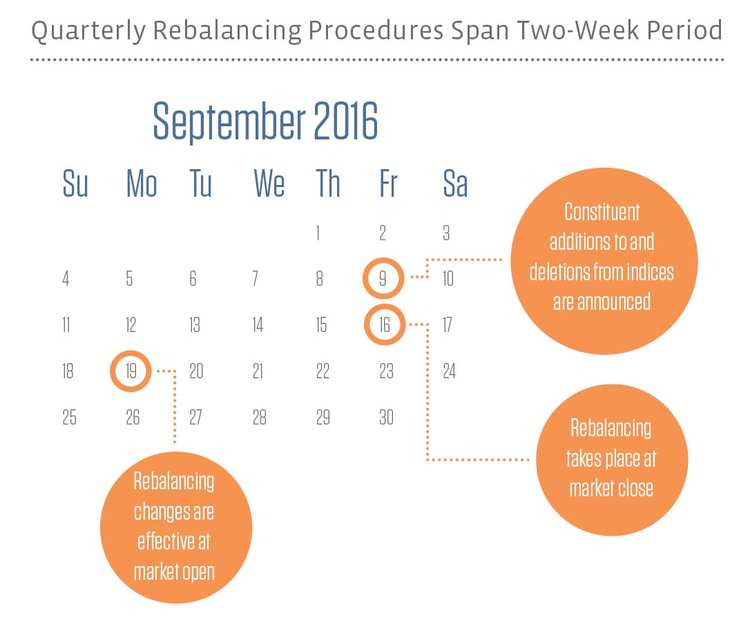

Quarterly rebalancings to the Alerian Index Series occur every March, June, September, and December. Results are announced on the second Friday, actual rebalancings take place on the third Friday after market close, and changes are effective at market open the following Monday. Special rebalancings are reviewed on a case-by-case basis; thus, we are unable to offer an easy-to-follow calendar because they are triggered by corporate actions.

The study period for the charts discussed in this post run from the 2011 Q1 rebalancing to the 2016 Q3 rebalancing. The data includes both quarterly and special rebalancings, but please note that under our current methodology names are no longer added to the indices during special rebalancings.

An MLP that is added to the AMZ or AMZI typically outperforms the index it was added to on the day the announcement was made. This is somewhat to be expected as about $3.6 billion of linked product tracks the AMZ and $12.3 billion tracks the AMZI. Investors expect the product providers will need to purchase a certain amount of the MLP’s units, thereby increasing demand and price of the MLP’s units. MLPs new to the AMZI tend to outperform by 307 bps compared to AMZ names’ 156 bps likely due to more AUM tracking the AMZI.

Performance on the date of announcement is one way to look at the Alerian effect. If you took a longer time frame, such as from the announcement date until one trading day after the rebalancing date, the results get more perplexing.

Keep in mind the numbers during this time period represent relative outperformance/underperformance versus the index, not the absolute performance of the MLPs over the time period. The trouble here is that the results don’t make that much sense. While the average over the time period is outperformance of 44 bps, constituents added to the AMZ actually (on average) underperform the index through the day after rebalancing by around 100 bps, whereas constituents added to the AMZI outperform by 368 bps. The “X”s in the chart below signify the relative performance of an entering MLP on the day of announcement, while the diamonds represent how an MLP performs relative to the index on the day of announcement through the close of the trading day after the rebalancing.

Now, while the average underperformance for the AMZ is a bit confusing, when broken out on a per MLP basis, the majority of MLPs in both the AMZ and the AMZI outperformed on the announcement date and through the day after rebalancing during the 1Q 2011 to 3Q 2016 study period.

In looking at the results of this study, we’ve searched for possible trends behind the data. Is it possible that although the Alerian indices are rules-based and formulaic, this medium-term effect could be due to investors mistakenly believing that adding a company to an index implies Alerian approval or recommendation of that MLP? Or, could it be because investors understand the methodology and believe any MLP that qualifies for an Alerian index has passed a minimum bar for investment? Another possibility with MLPs that experienced significant outperformance or underperformance is that the market incorrectly speculated the results of the rebalancing.

In reality, we may never know the exact reason the chips fall as they do. What we do know is that if you have questions surrounding the Alerian rebalancings, please make sure you’ve read our methodology guides (AMZ and AMZI). If you still have questions, check out this great post our CEO wrote that walks readers through a portion of the 2Q 2016 rebalancing. And if you still have lingering confusion, remember that you can always email me at index@alerian.com.

Next week, we’ll look at the same data, but for MLPs existing an index.