…But pipelines are ultimately needed.

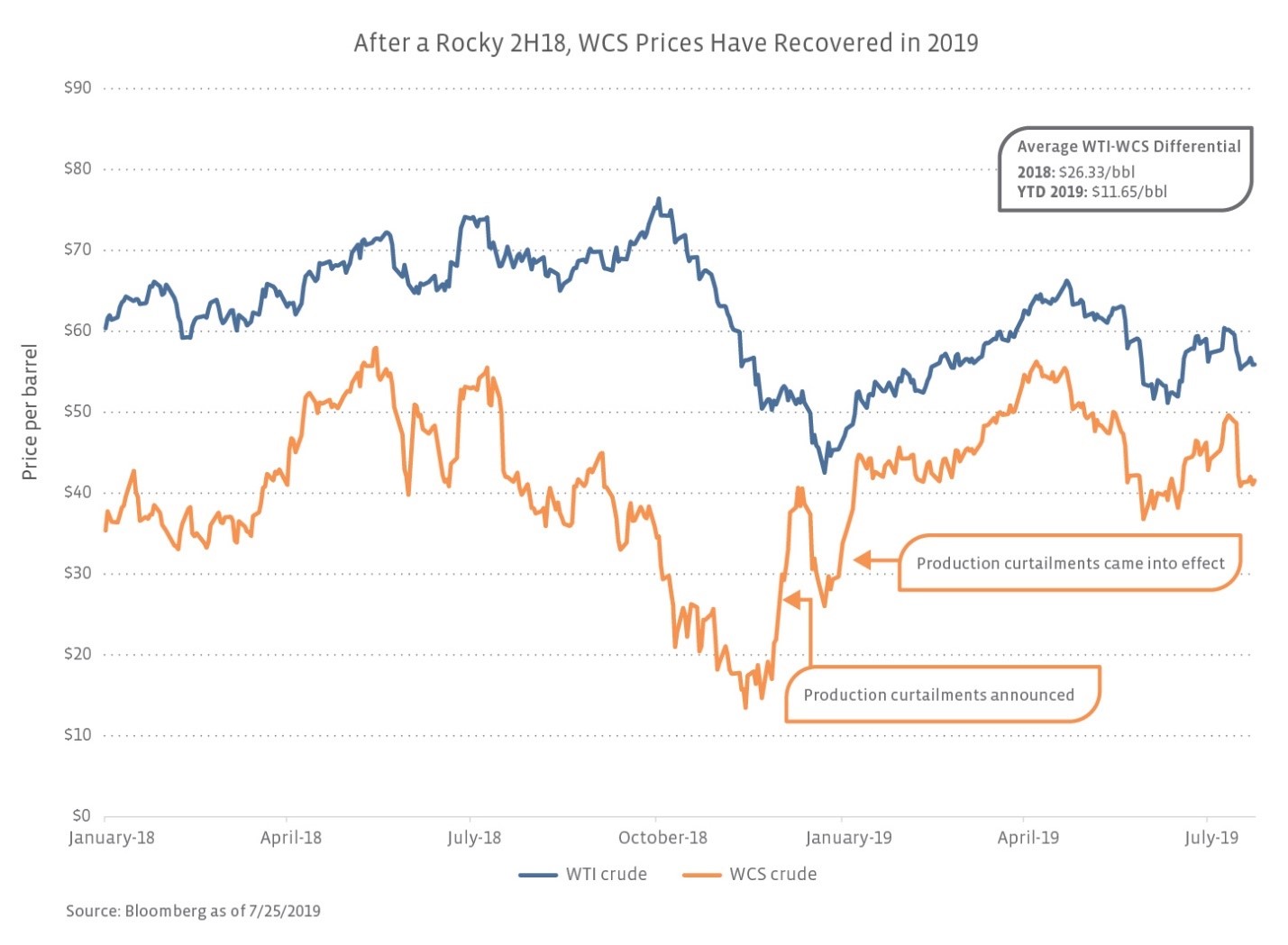

Production limits have supported WCS prices this year, but additional pipeline takeaway capacity is the best long-term solution for improving crude prices in Western Canada. Capacity additions have been challenging to say the least due to regulatory hurdles on both sides of the border. In addition to midstream companies working to add capacity, the US and Canadian governments as well as the provincial government in Alberta, have intervened.

Highlighting the critical need for pipeline capacity, the Canadian government purchased the Trans Mountain Pipeline System from Kinder Morgan Canada (KML) in late 2018 for C$4.5 billion. The existing 300-Mbpd Trans Mountain Pipeline connects Edmonton, Alberta, to the coast of British Columbia. The potential expansion would triple the pipeline’s capacity, providing greater export optionality with access to markets beyond the US. On June 18, the federal government announced its approval of the Trans Mountain expansion with the expectation that construction would start in some areas this year. However, additional permits are required, and the timeline remains unclear. In February, the Alberta government under former Premier Rachel Notley entered into C$3.7 billion worth of rail contracts with plans to buy crude from producers and ship up to 120 MBpd to market by 2020. With Jason Kenney replacing Notley as Premier in April, the province is now looking to divest those contracts.

Turning to company projects, two major crude takeaway pipelines have faced significant delays. Enbridge’s (ENB) Line 3 Replacement would add 370 MBpd of takeaway from Alberta to Wisconsin, bringing total capacity to 760 MBpd. While construction of the Canadian portion of the project was completed in May 2019, regulatory issues have delayed the US portion. In June, the Minnesota Court of Appeals took issue with an aspect of the project’s Final Environmental Impact Statement. Investors will look for any project update with ENB’s earnings announcement on Friday, with the latest timeline targeting service in 2H20. TC Energy’s (TRP) Keystone XL pipeline, which would run from Hardisty to Steele City, Nebraska, has undergone more than a decade of reviews with obstacles still remaining. Despite President Trump’s permit allowing the project to avoid further environmental review at the federal level, hurdles to construction still exist at the state level, not to mention a challenge to President Trump’s permit from environmental groups.

Though smaller in scale, Plains All American’s (PAA) Canadian subsidiary Plains Midstream Canada recently announced an expansion to the existing Rangeland pipeline system, which transports light crude. PAA plans to increase southbound capacity from Sundre, AB to the US-Canada border from 20 MBpd to 100 MBpd. The expansion will be fully completed in 2021. Earlier this month, ENB announced an open season for both existing and expanded capacity on the Express Pipeline. The 280-MBpd pipeline from Hardisty, AB to Casper, WY can transport a range of crude types from light to heavy. These expansions would help provide an additional outlet for Canadian crude, but greater capacity additions will be needed.

Production growth challenged by takeaway constraints.

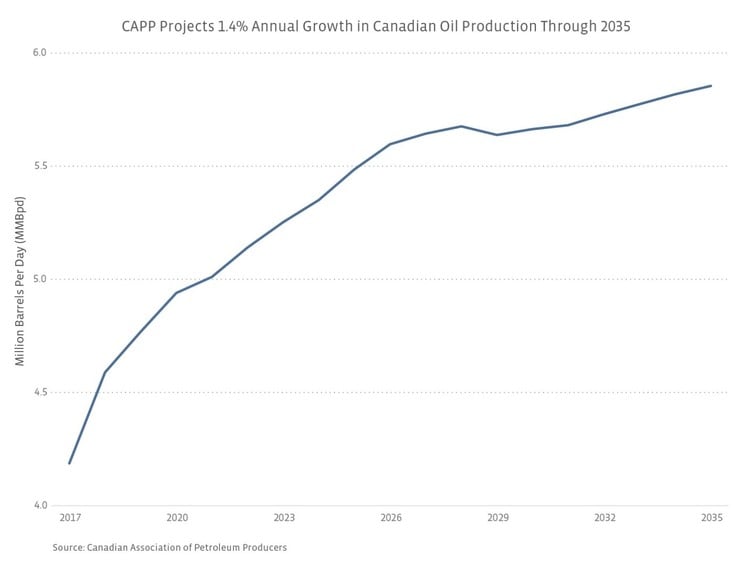

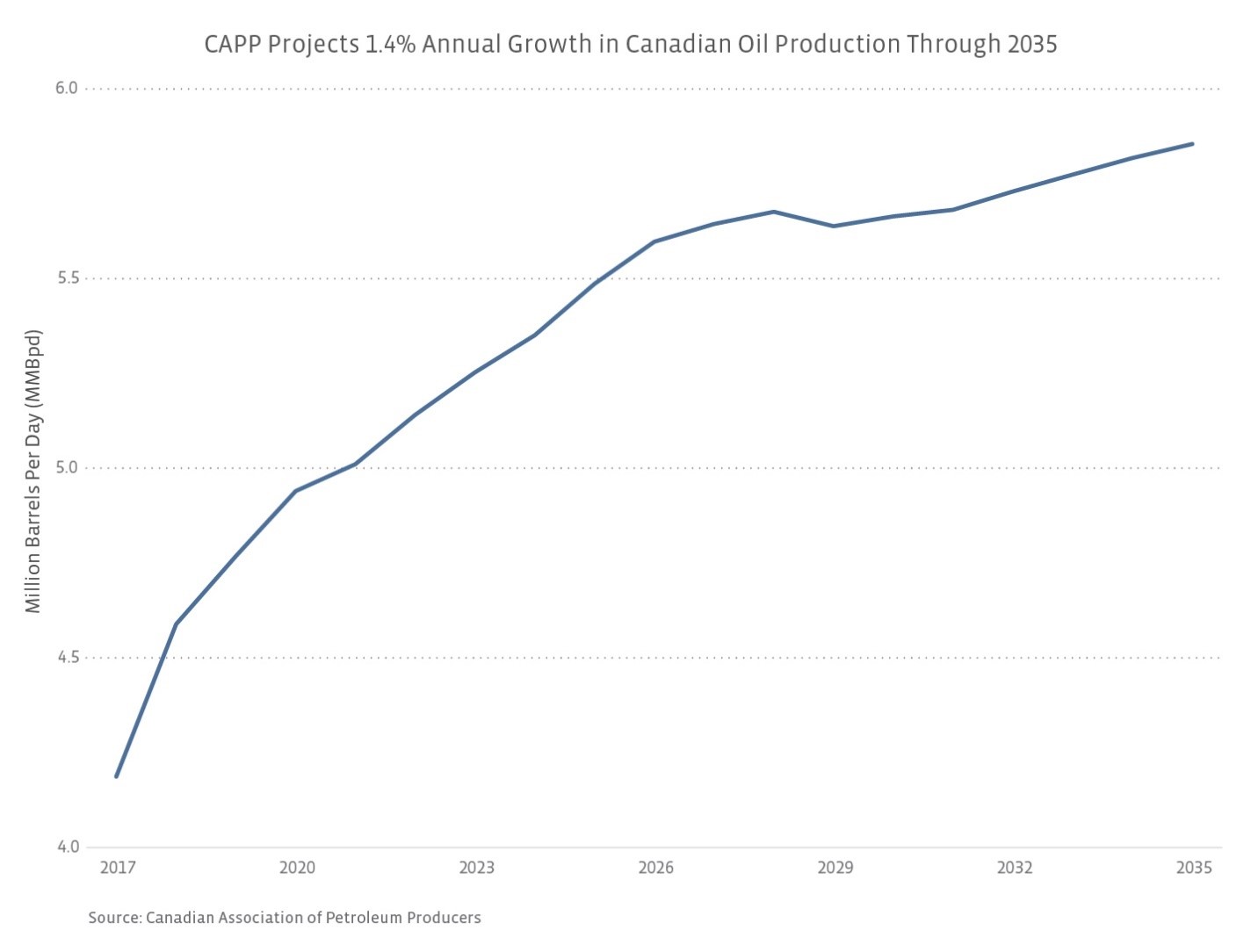

Pipeline capacity limitations have implications for long-term oil production growth from Canada, which boasts the third-largest oil reserves in the world thanks to the oil sands. Citing inefficient regulation and uncertainty surrounding additional transportation capacity, the Canadian Association of Petroleum Producers (CAPP) is forecasting annual oil production growth of 1.4% through 2035. While directionally positive, growth expectations have been tempered in recent years. CAPP had forecasted 4% average annual growth through 2030 back in 2014.

Canadian midstream companies still offer attractive investment characteristics.

While project delays have been frustrating for the midstream companies trying to add capacity, Canadian oil producers and the complex US refiners desiring heavy crudes are the primary parties that suffer from inadequate takeaway. In short, the challenges facing pipeline capacity additions from Canada should not be interpreted to mean that Canadian midstream companies are also challenged. In fact, Canadian midstream names provide attractive investment characteristics that differentiate them from the rest of the North American midstream universe. Our analysis focuses on the six Canadian companies in the Alerian Midstream Energy Select Index (AMEI): ENB, TRP, Gibson Energy (GEI), Inter Pipeline (IPL), Keyera Corp (KEY), and Pembina Pipeline Corp (PPL CN/PBA). Keep in mind that many Canadian companies own assets in the US and have growth projects in the US, with ENB and TRP having particularly large US footprints.

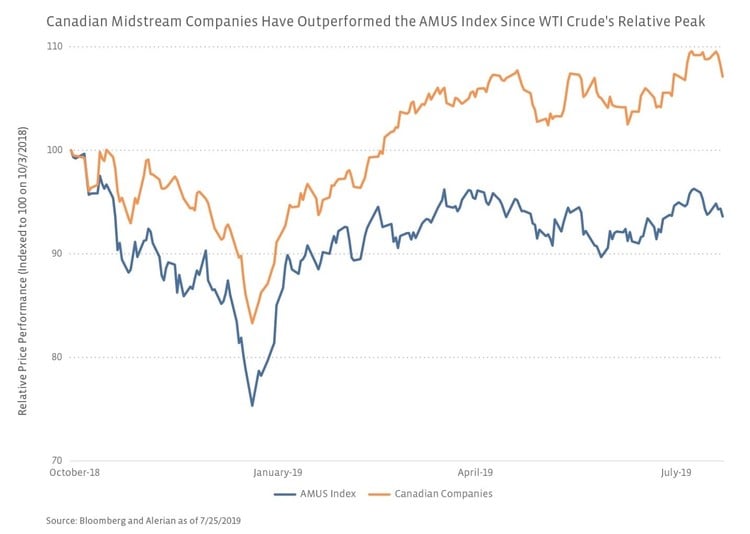

Overall, Canadian midstream companies can provide beneficial diversification to a portfolio of US midstream companies, as represented by the Alerian US Midstream Energy Index (AMUS). Canadian midstream companies have a five-year correlation of 0.28 with WTI crude, which is significantly lower than the 0.56 correlation between AMUS and WTI. Additionally, the Canadian energy infrastructure names have a five-year correlation with the S&P 500 of only 0.33 compared to 0.79 for AMUS.

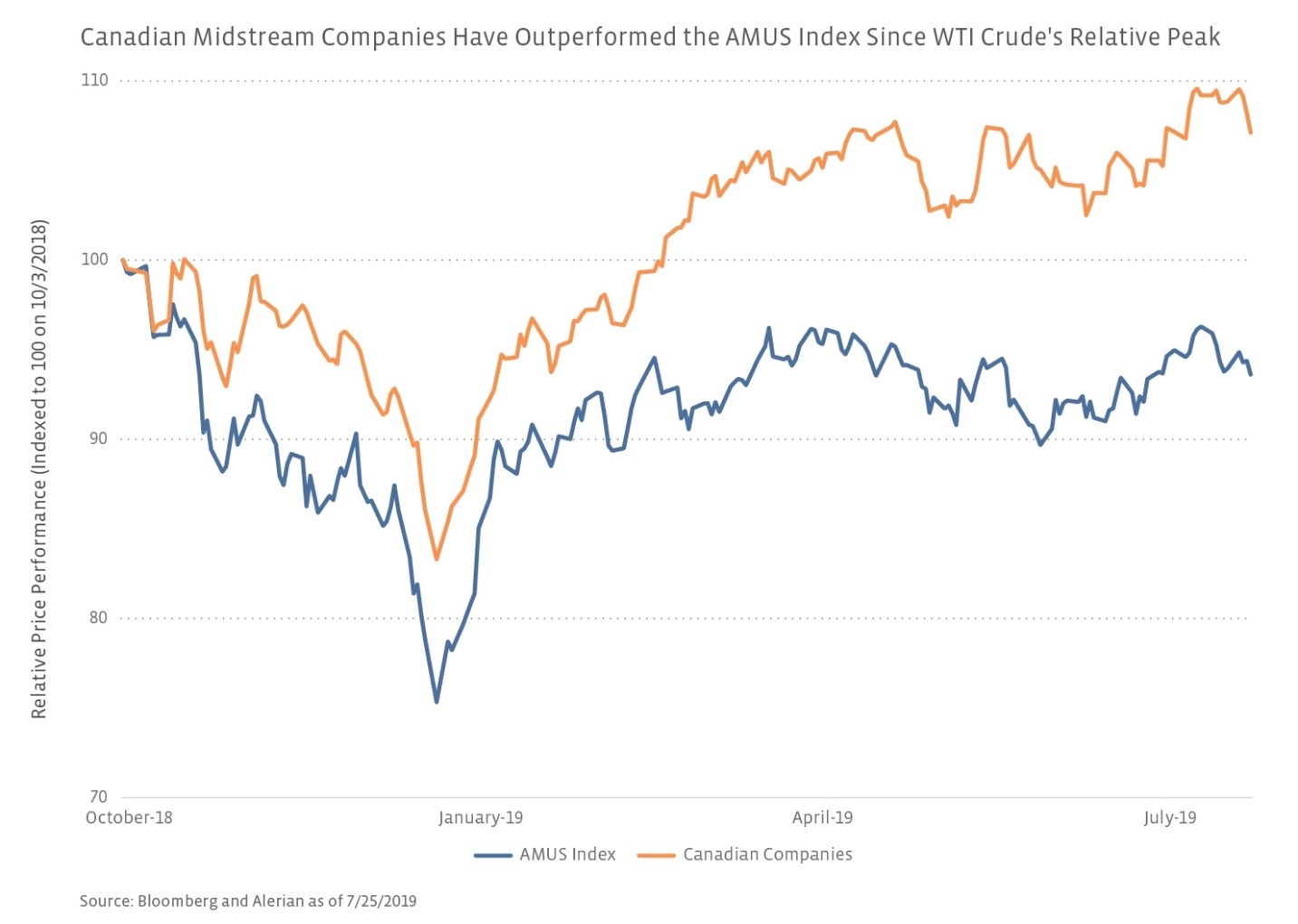

Canadian names also act more defensively than US C-Corps and MLPs in a falling crude price environment. As seen in the graph below, the Canadian companies outperformed the AMUS Index as WTI crude prices fell by 44.3% from their relative peak of $76/bbl on October 3 to less than $43/bbl on December 24. Additionally, Canadian names have outperformed US midstream names as crude prices have improved. Through July 25, AMUS gained 17.5% year to date, while the Canadian securities are up 22.9% on a price-return basis. For a further discussion of the investment considerations surrounding Canadian energy infrastructure companies, please see our Insights post from last September here.

Bottom Line

A difficult regulatory environment and the resulting takeaway constraints have come at a great cost to Canadian oil producers. Although production limits and Venezuela sanctions have helped support prices for Canadian heavy crude this year, additional pipeline capacity is ultimately the best solution for sustainable price improvement, and major projects bear watching as regulatory hurdles are navigated. Despite the high-level challenges surrounding takeaway capacity and oil production growth, Canadian midstream companies offer many attractive qualities, particularly as a complement to a US midstream portfolio.

{kind=link}

{kind=link}

{kind=link}