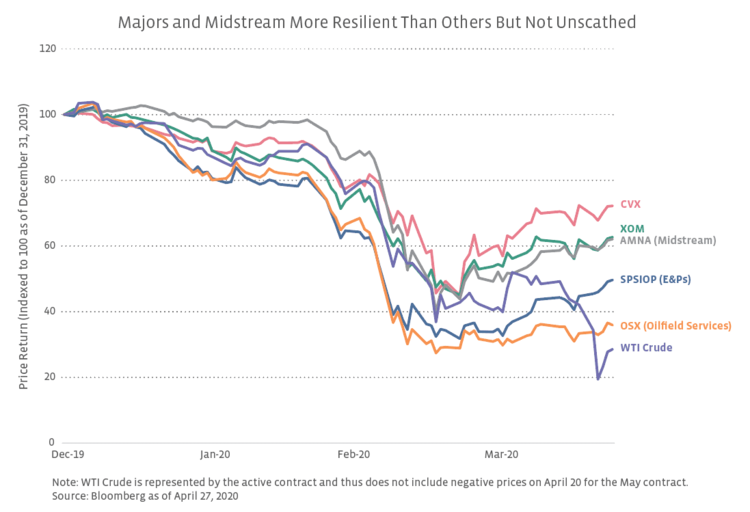

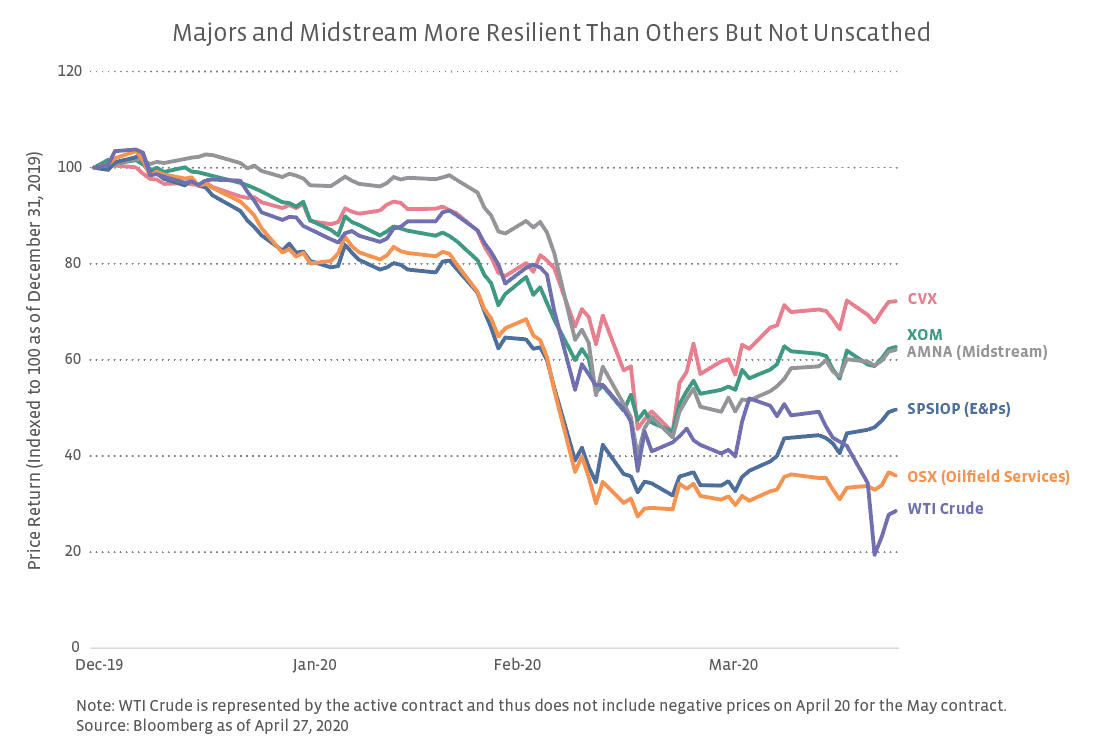

With oil prices falling by over 70% year-to-date through April 24, even defensive portions of the energy sector have experienced a significant sell-off, including the integrated majors like Exxon (XOM) and Chevron (CVX) and the midstream space. As discussed in the past (read more), both are considered more defensive sectors of energy but for different reasons. In short, the majors tend to be defensive given their size, diversification and integration (both upstream and downstream assets), balance sheet strength, and dividend track record. Midstream is defensive due to the fee-based nature of cash flows and contract protections like minimum volume commitments.

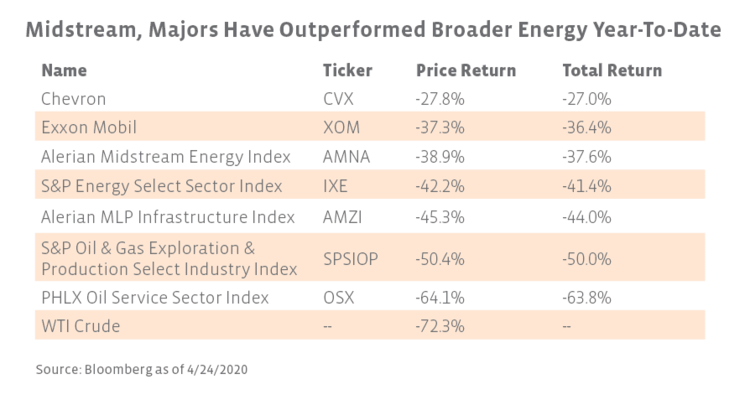

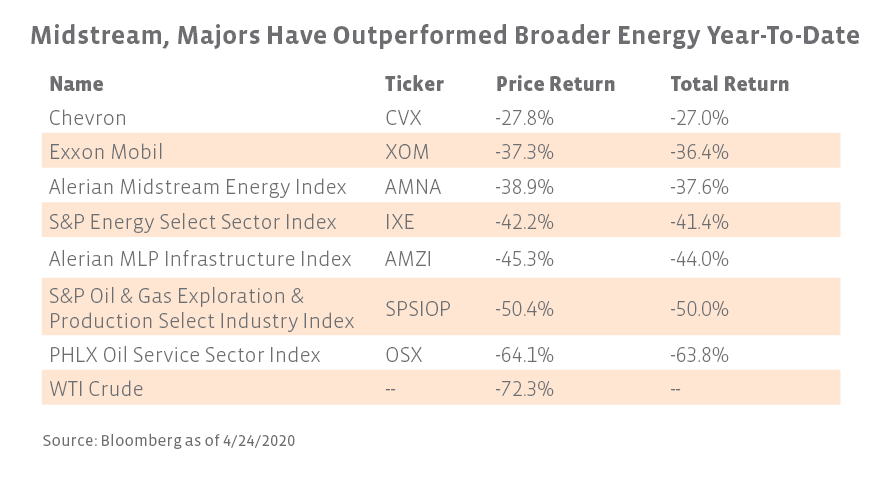

How have midstream and the majors held up as oil prices have plunged? CVX has been the most resilient, while the broad Alerian Midstream Energy Index (AMNA) has performed largely in line with XOM as shown in the chart. Turning to the more detailed table, midstream and the majors have outperformed broader energy as represented by the Energy Select Sector Index (IXE), which is significantly weighted to XOM and CVX (40%+ combined). For the majors, upstream and downstream can sometimes be a hedge with lower oil prices harming upstream profitability but typically helping downstream as demand increases. However, in today’s environment, both upstream and downstream are being negatively impacted by the demand fallout from COVID-19. In the case of midstream and MLPs, oil price weakness contributes to concerns around the financial health of producer customers, and counterparty risk has also come into focus. MLPs, as represented by the Alerian MLP Infrastructure Index (AMZI), have underperformed the majors and broader midstream but have noticeably outperformed other sectors of energy. Given their leverage to commodity prices, Exploration & Production (E&P) companies represented by the S&P Oil & Gas Exploration & Production Select Industry Index (SPSIOP) and Oilfield Services represented by the PHLX Oil Service Sector Index (OSX) have been the hardest hit. Notably, all energy sectors shown have outperformed the year-to-date move in oil prices.

While midstream and MLPs have not been completely insulated from the volatility in oil prices, their relative performance has been defensive, which reflects the fee-based nature of their business models and the benefits of contract protections in a challenging environment.

{kind=link}

{kind=link}