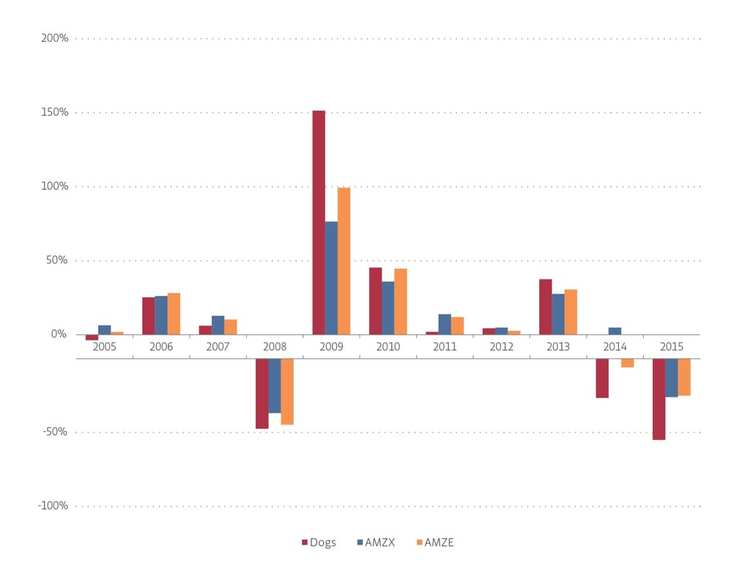

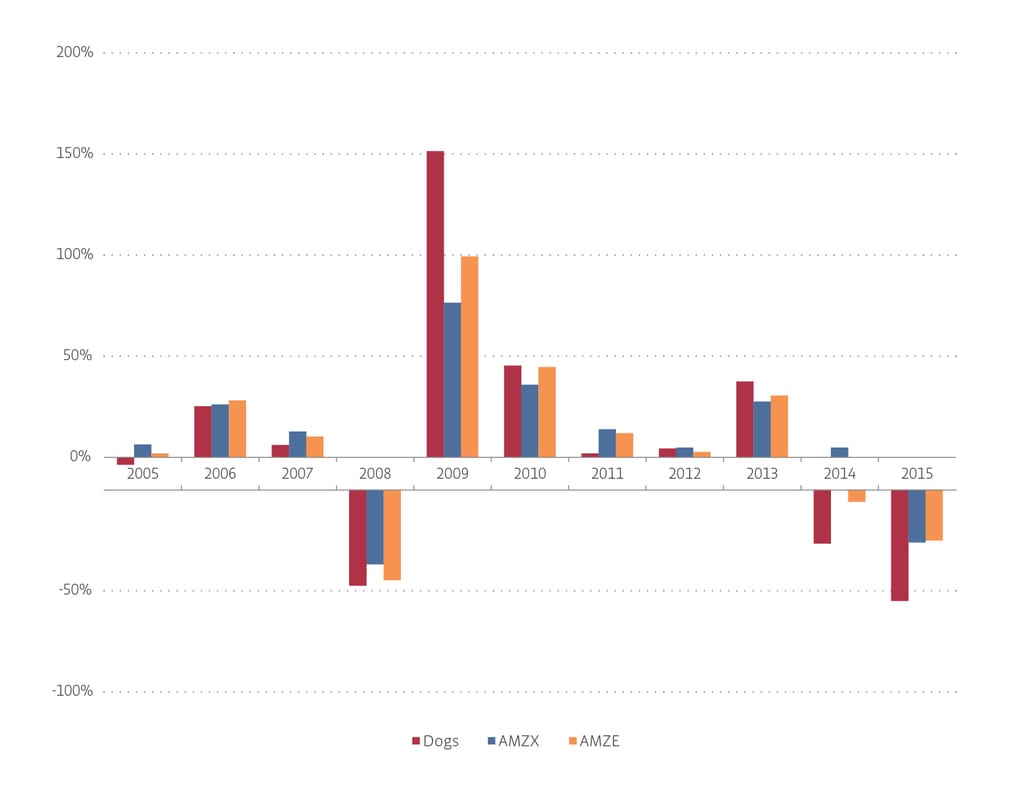

But looking at the past 10 years cumulatively, the dogs underperform the AMZ and the AMZE. In the past two years, as MLPs fell, the dogs fell considerably more.

Analysis

The Dogs of the Dow rests on the theory that all 30 names in the index are good investments and that a company with a yield higher than its peers is merely temporarily depressed. In a world where tail-risk never comes to pass, the dogs may be good investments. When it’s time to pay the piper, however, with MLPs, there are many reasons a company’s higher yield may not revert to the mean.

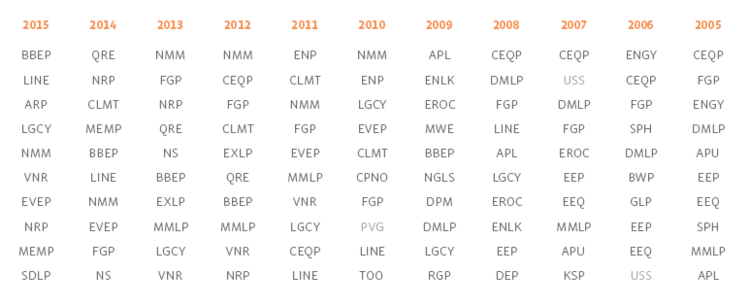

Higher yields can indicate more risk. Investors require more reward for taking on more risk. Not all MLPs operate fee-based, toll-road business models. A simple yield sort on our MLP Screener shows how those names with exposure to more volatile cash flows (e.g. Production + Mining and Marine Transportation) currently have some of the higher yields. Of those MLPs in the Dogs of the AMZ at the beginning of 2015, nearly all are Production + Mining companies.

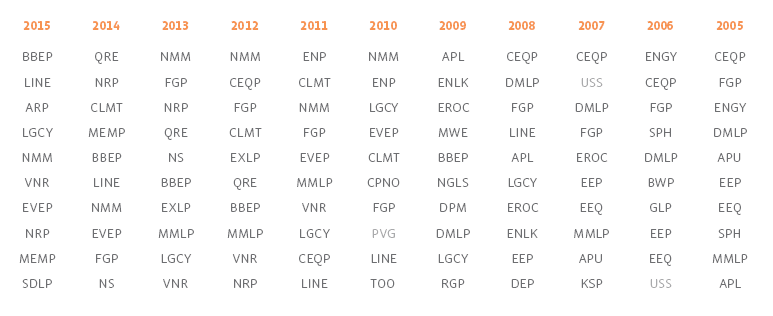

Higher yields can indicate low to no growth. In general, the MLPs with the highest expected and most visible distribution growth (such as dropdown stories) have the lowest yields. Whereas a company that is not expected to grow at all will trade to a higher yield. Only this past year has Ferrellgas Partners (FGP) broken its 20-year streak of $0.50 quarterly distributions. (President and CEO, Kenny Feng called this The End of an MLP Era.) In the 10 years (plus 2015) that the Dogs of the AMZ was calculated, FGP was the most common constituent. It was included in every year except 2009 and 2015.

Higher yields can indicate problems in the underlying company. A blind yield screen can ignore facts about underlying fundamentals that simple research would reveal. Perhaps a company issued a recent press release indicating bad news: key management leaving, cost overruns, facility downtime, disappointing guidance, or an uneconomic acquisition. Sometimes, a company can be trading at an extremely high yield because investors are expecting a distribution cut or that the company will not recover from an adverse event.

Conclusion

Just as high-yield bonds are not regular-bonds-but-better, high-yield MLPs are not simply the better MLPs . MLP investing continues to have a steep learning curve. There is no single explanation for recent underperformance, just as there is no simple way to make MLP money. Those investors who do the most due diligence and educate themselves will suffer the fewest surprises and have the most confidence going into the next cycle. We encourage you not to take shortcuts (however enticing or well-renowned the theory) with your MLP portfolio.

{kind=link}

{kind=link}

{kind=link}