Source: Enterprise Products Partners Analyst Conference Presentation

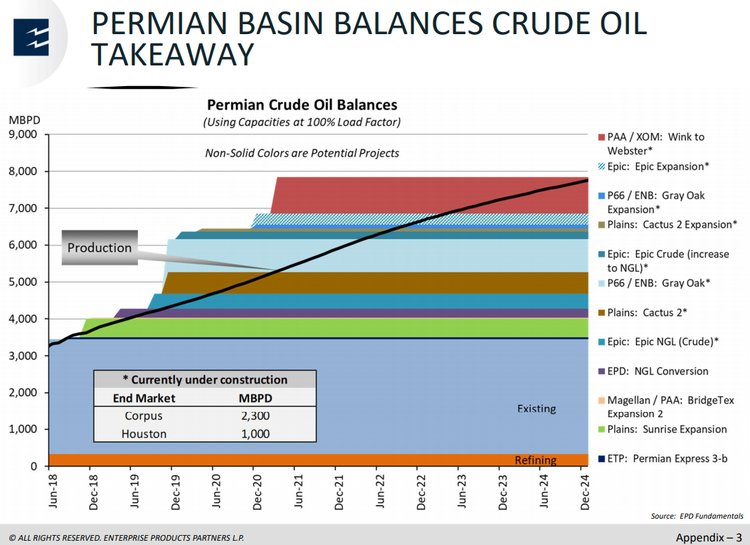

This production growth sets the stage for prolific export opportunities, though perhaps not every proposed project will get built (read more). For its part, EPD highlighted its access to 40 different grades of crude and 45 million barrels of storage in the Houston area as integral advantages for continued export success. With growing exports, Houston has become a more prominent oil price point (read more), as reflected in EPD’s partnership with CME Group on the WTI Houston Crude Oil Futures (HCL) contract. Management emphasized the transparency of the CME contract and EPD’s ability to ensure crude quality as advantages, particularly given recent media reports of US crude being rejected by foreign buyers.

Project backlog includes diversified revenue from petrochemicals.

EPD expects to spend $2.9 billion in growth capital expenditures in 2019, with $6.7 billion of projects to be placed into service this year or currently under construction. In total, EPD cited $5-10 billion of projects under development. Clearly, the fundamental backdrop of growing US energy production and EPD’s existing footprint create plenty of growth opportunities, including in petrochemicals.

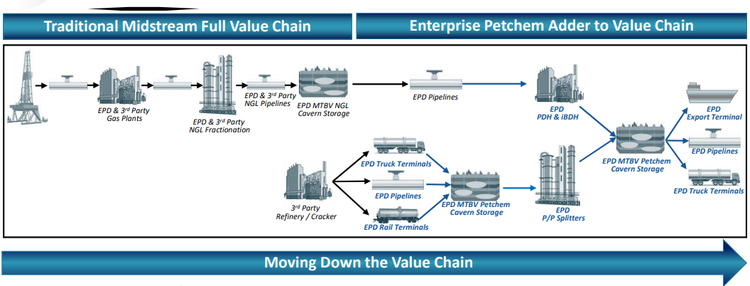

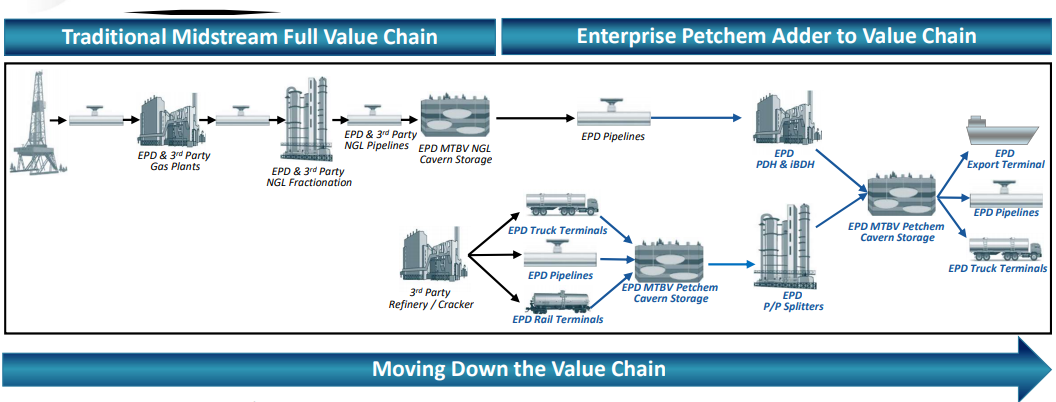

Petrochemicals featured prominently in the discussion of growth projects. Petchem is expected to provide a diversified source of fee-based revenue with insulation from competition due to high barriers to entry. By 2025 or sooner, the petchem business is expected to generate $1 billion in gross operating margin from a little over $600 million today. To summarize, the petchem business is essentially providing midstream services to a different set of customers. Roughly two-thirds of Enterprise’s petchem volumes are fee-based, and the remaining volumes are spread-based. As we discussed in our recent piece on petchem, EPD is leveraging its NGL value chain (see chart below) to construct a second isobutane dehydrogenation (iBDH) plant that will be completed in 4Q19 in addition to potentially developing a second propane dehydrogenation plant (PDH).

Source: Enterprise Products Partners Analyst Conference Presentation

Bottom Line

Among MLPs, EPD is one of the leaders in terms of transitioning from the historical MLP model to a more traditional financial model, which should be welcomed by both generalist and MLP-dedicated investors alike. Aside from positive strategic strides, investors will be watching to see how the company executes its growth project backlog and capitalizes on the combination of market opportunities and its existing asset footprint.

{kind=link}

{kind=link}