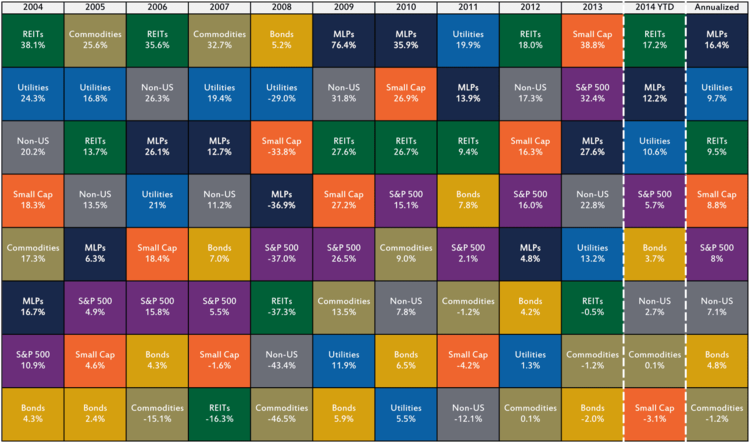

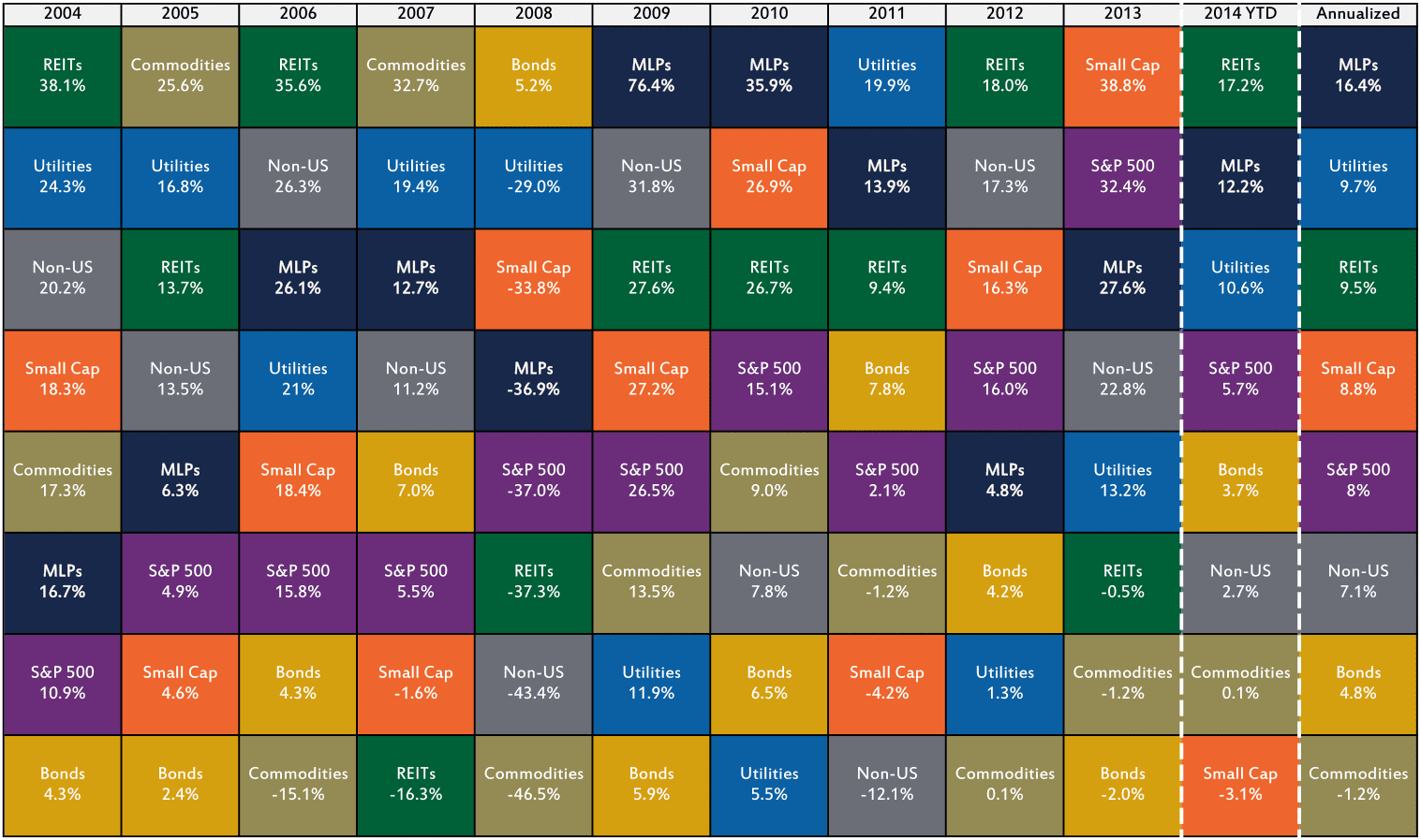

Past performance is no guarantee of future returns, but those who do not learn from history are doomed to repeat it. So many conflicting clichés, but no one has a crystal ball when it comes to investing. That’s one of the reasons diversification is so popular. So in this chart, we’ve presented 10 years of performance of the broader market, yield-oriented equities, and asset classes typically used for diversification.

When looking through this chart, it’s easy to scan and see how asset classes have performed against each other. That’s useful, but it’s easy to overlook the magnitude of their differences. For instance, in 2009, MLPs were up over 70%, more than twice as much as any other asset class. So far in 2014, there’s only a 20% spread between the best and worst performing asset classes.

Looking at the mustard yellow boxes representing bond performance, it’s easy to see why some income-oriented investors are considering replacing some or all of their bond exposure with MLPs. While both asset classes do have higher yields and lower correlations to the broader market, MLPs are equities, not bonds. They are not guaranteed to pay a dividend and may react more strongly to changing market conditions. This was most evident in 2008, when MLPs fell twice as far as bonds.

One smaller point of comparison is between MLPs and commodities. MLPs traditionally operate fee-for-service or toll-road business models that are generally agnostic to moderate changes in commodity prices. However, at some point, if commodity prices rise high enough, demand destruction could reduce volumes and negatively affect MLP cash flows. On the other side, if commodity prices fall far enough, the cost to get them out of the ground could exceed the price at which they can be sold. In this case, producers will shut in (or cease) production, which will also reduce volumes and negatively affect MLP cash flows. Fortunately for MLPs, meaningful swings in commodity prices are self-correcting mechanisms. It is also worth noting that as MLPs have become a better known asset class, and investors associate them with the energy sector in general, correlation to commodities has risen.

When speaking about diversification, MLPs and REITs are often compared to each other. However, comparing statistics from the AMZ factsheet, REITs have more volatility as measured by standard deviation, with less return. When looking at any data, it’s always best to look at the numbers in several different ways, as any one chart will not be able to tell the whole story.

We would be remiss if we didn’t acknowledge that this chart is known by the industry as the “EPD Blinking Slide”, a reference to Enterprise Products Partners’ use of a periodic performance table at its annual March analyst day to highlight the stock’s outperformance over the years. Their table looks similar to the one above, though with different colors and animation for EPD’s box in each column.

Master Limited Partnerships (MLPs) are represented by the Alerian MLP Index (AMZ). Utilities are represented by the S&P 500 Utilities Index. Real Estate Investment Trusts (REITs) are represented by the FTSE NAREIT Real Estate 50 Index. Small-cap equities are represented by the Russell 2000 Index. The S&P 500 is a capitalization-weighted index of 500 stocks designed to measure performance of the broad US economy. Non-US equities are represented by the MSCI EAFE Index. Bonds are represented by the Barclays US Aggregate Total Return Bond Index. Commodities are represented by the S&P World Commodity Index. Performance is provided on a total return basis. Annualized performance represents the period from July 31, 2004 to July 31, 2014. Year-to-date performance is as of July 31, 2014.

{kind=link}