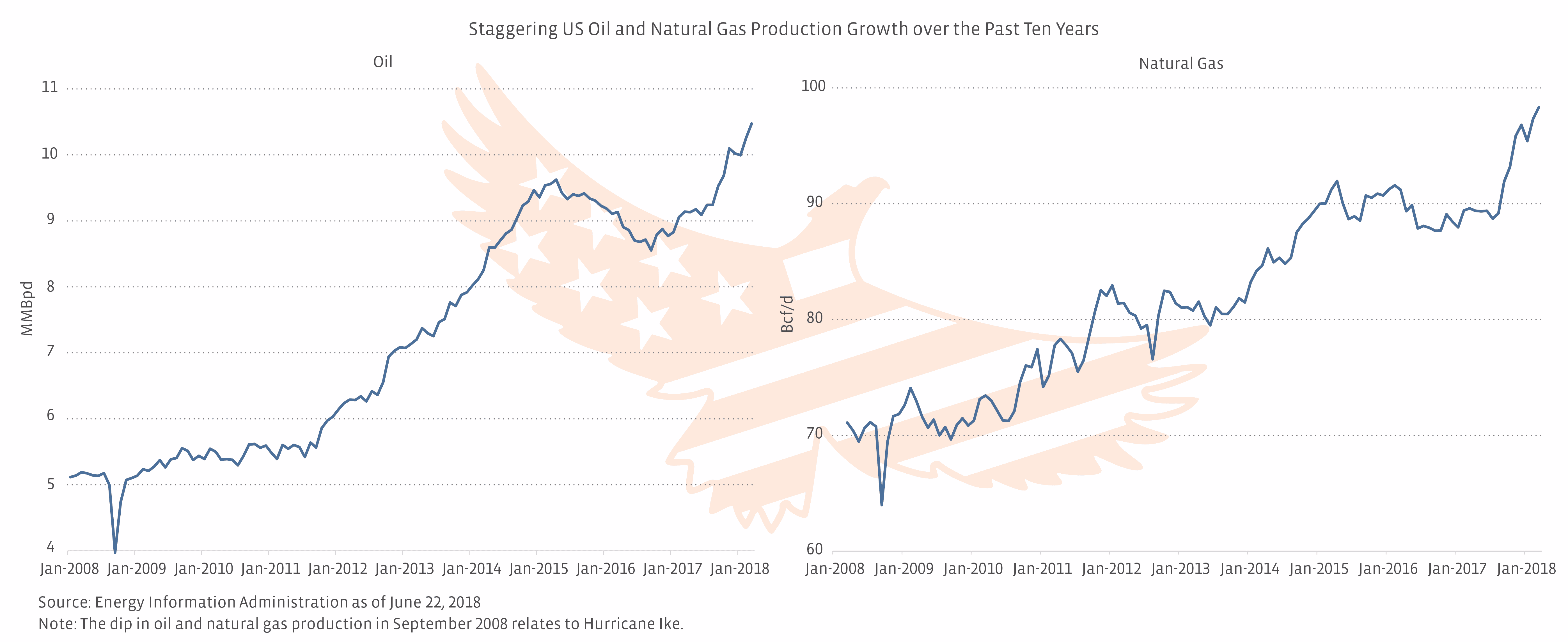

The US energy landscape has been revolutionized in just ten years.

Fast forward to today. US oil and natural gas production is at record highs. We still import a significant amount of crude (~8 MMBpd), but we’ve recently been exporting more than 1.5 MMBpd of crude. Ten years ago, crude exports were banned, but crude exports were not even practical given the low level of production. (The crude export ban was lifted in 2015.) Today, we’re a net exporter of petroleum products, with net exports exceeding 3 MMBpd recently. With the abundance of natural gas in the US, energy companies are focused on exports of liquified natural gas (LNG) as opposed to imports. In February 2016, Cheniere’s re-purposed Sabine Pass terminal became the first commercial facility in the Lower 48 to export LNG. Today, both Sabine Pass and Dominion’s (D) Cove Point terminal are exporting LNG, with additional terminals in various stages of development.

The role of midstream in the US energy revolution.

The change in US energy dynamics has led to a total change in energy flows, which has required adjustments to existing midstream infrastructure and new infrastructure. Crude imports used to be unloaded in the Gulf Coast and sent north via barges or pipelines (Cap Line from Louisiana or Seaway from Texas) to refineries in the US Midwest. Today, production from the US and Canada supplies those Midwest refineries. Additional oil production from the Mid-Continent of the US is shipped south to the Gulf Coast to be used by refineries there or potentially exported. The reversal of the Seaway pipeline to flow from Cushing to the Gulf Coast was a landmark event in reconfiguring US oil flows. A reversal of Cap Line has also been contemplated. Pipeline conversions have also facilitated changing flows. For example, Energy Transfer’s (ETP) Trunkline was converted from gas to crude service to facilitate the build out of the Bakken Pipeline, which moves crude from the Bakken to the Gulf Coast.

On the natural gas side, flows have also evolved due to the dramatic growth in production, particularly from the Marcellus. Take the Rockies Express (REX) pipeline for example. The gas pipeline was originally built flowing east from Colorado/Wyoming to eastern Ohio, supplying the Northeast with gas from the Rockies. In 2014, a portion of the pipeline became bi-directional, and by January 2017, the REX pipeline had significant bi-directional capacity from Clarington, Ohio, to Mexico, Missouri (referred to as Zone 3).

MLPs and energy infrastructure companies have played a vital role in allowing burgeoning US production to get to end markets by reversing and converting existing pipelines, in addition to building new pipelines. Just think of all the new crude and natural gas pipelines that have been added from the Permian Basin in recent years and all the pipelines being built today. As noted in the recently released INGAA study on oil and gas infrastructure investment (see our post from last week for more details), $115 billion was invested in oil, natural gas, and NGL pipelines in the US and Canada during the five-year period of 2013-2017. That’s an extraordinary investment in just five years.

Finally, the unsung hero of the US energy revolution: the EIA.

In the US, we’re extremely fortunate to have timely energy data from the US Energy Information Administration. We often take for granted the vast amounts of information we have on US oil and natural gas production, consumption, movements, inventories, etc. and the frequency of that information (weekly in several cases). Analyzing these same energy trends in many other countries would face a much greater challenge. Thanks to the data from the EIA, we’ve been able to observe these remarkable changes in the US energy landscape in an accurate and timely manner.

{kind=link}