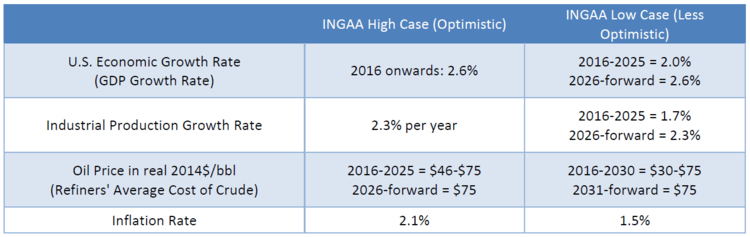

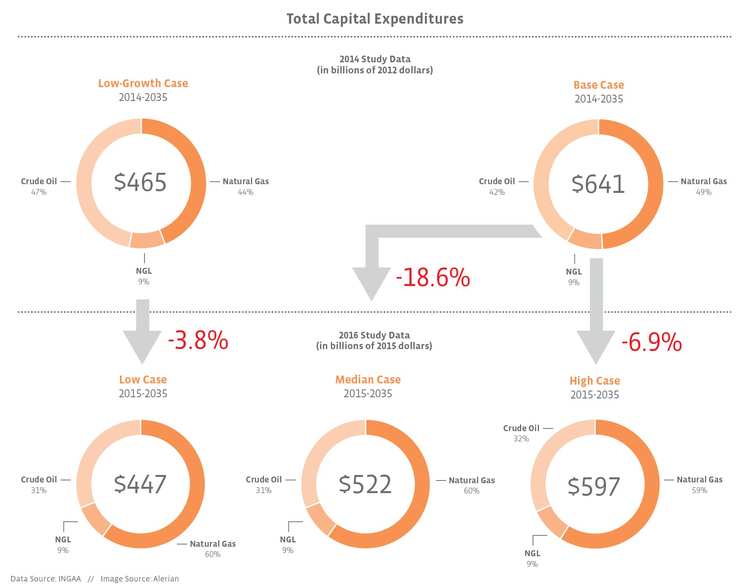

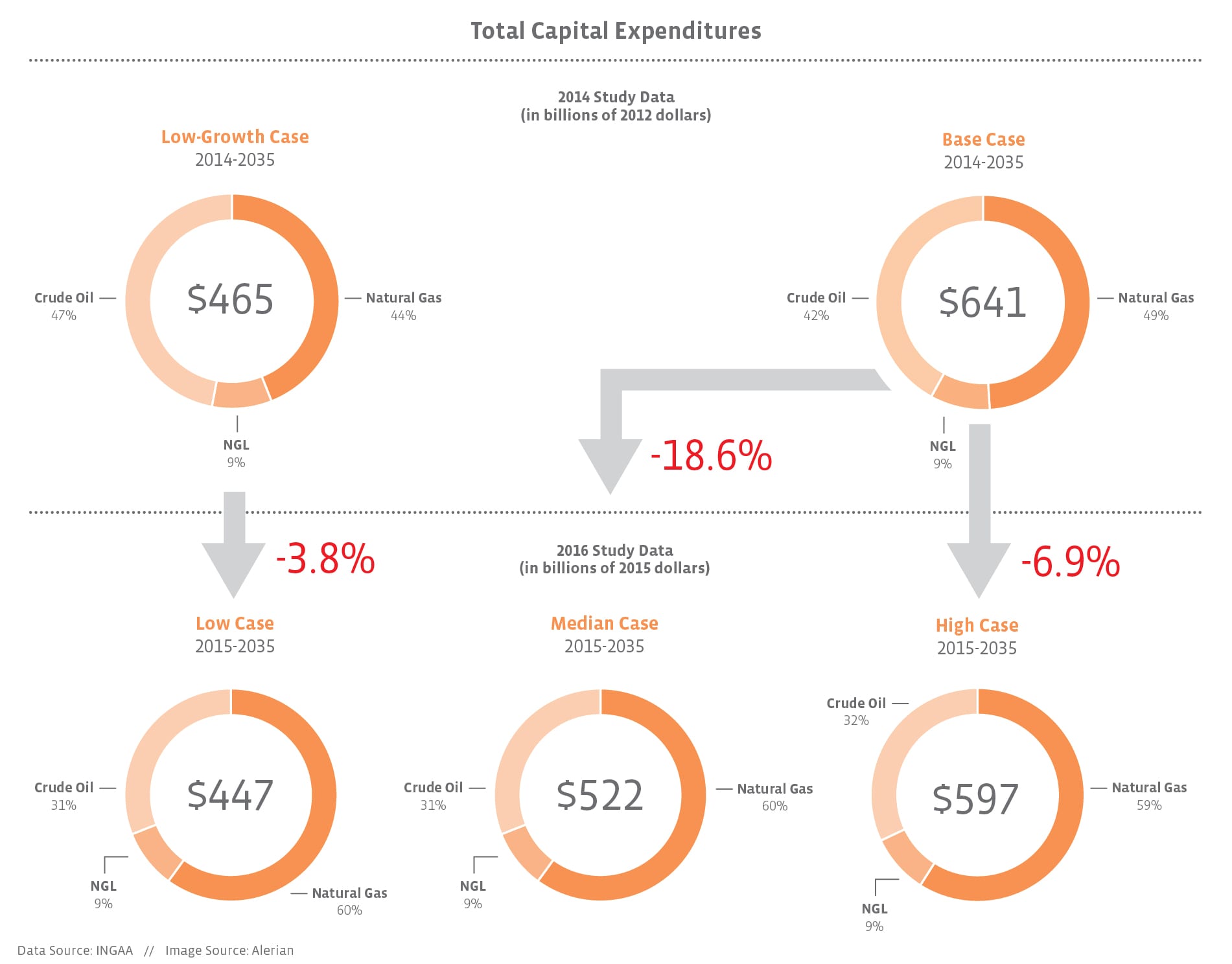

A direct comparison from 2014 to 2016 is a bit tricky because the authors decided against a base case this year due to the uncertainty of the current environment. So, in an effort to provide better evaluation metrics, we’ve included a median case. No matter how you slice it, the projections for new midstream infrastructure needed in the US and Canada have dropped.

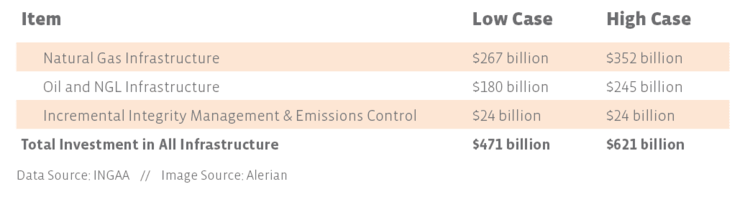

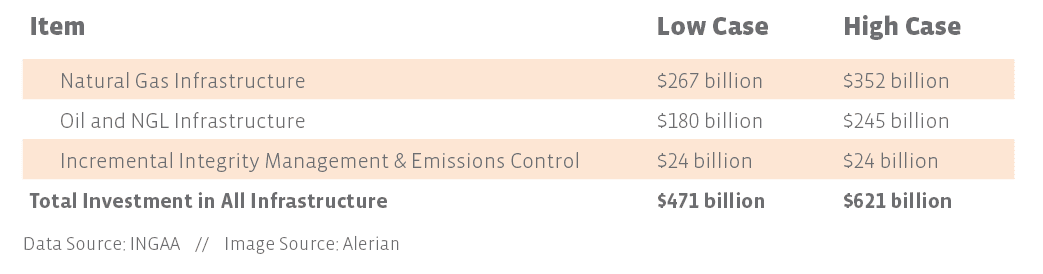

It’s worth mentioning, however, that in their final estimates, the authors of the study included $24 billion (in both the low and high cases) for integrity management. In the past, capital expenses associated with routine replacement and refurbishment of pipelines were already included in cost estimates, but recently released emissions standards have come with an eye-popping implementation price tag and added a new line item to pipeline expenditures. The new National Ambient Air Quality Standards that would require things like hydrostatic testing, in-line inspection, and valve testing are still in litigation, but are items the experts believe may be imminent for pipelines of the future. This undoubtedly has a significant impact, as adding this expense back to the 2016 figures provided in the chart above brings the numbers a bit closer to 2014 estimates. Please check out the table below to see the impact of including the new integrity management expenses.

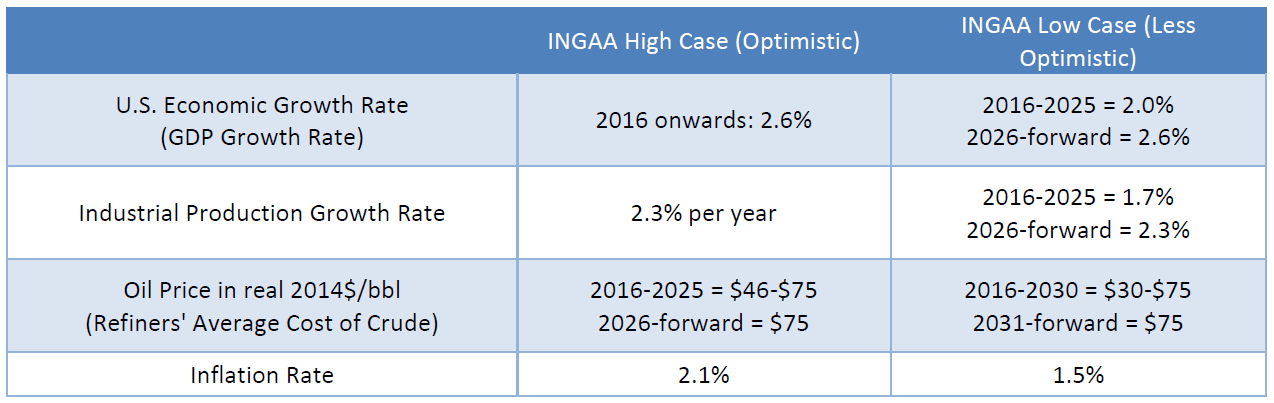

If you’ve read any of our previous blog posts, or read anything about energy over the past year, you’re probably pretty clear on why predictions have decreased. In addition to having a supply glut in the US, world oil supply has also increased. The lifting of sanctions on Iran and globally weakened demand have resulted in the perfect storm. The study also notes improved energy efficiency and renewable energy as potential factors that could impact demand. Given all of this, it’s difficult to predict if/when a recovery will happen and on what scale.

The study clearly incorporates one trend we’ve already discussed, which is natural gas coming to the forefront. If you look closely at the pie charts above, you’ll notice that a significant portion of predicted capex for new midstream infrastructure has shifted from crude oil to natural gas. Crude oil production growth (and the associated need for infrastructure) is predicted to slow because of the oil prices assumed. On the other hand, shale gas production has remained strong resulting in a predicted need for natural gas infrastructure.

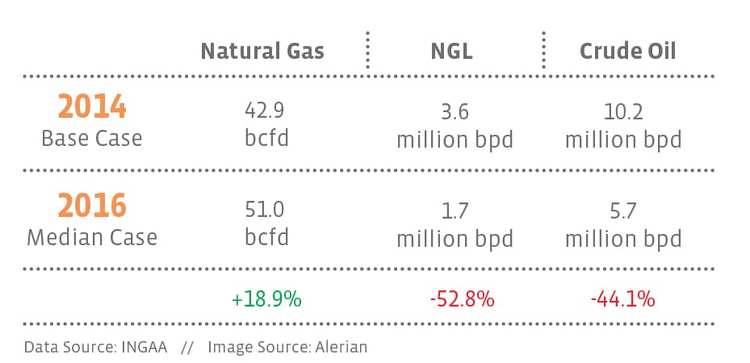

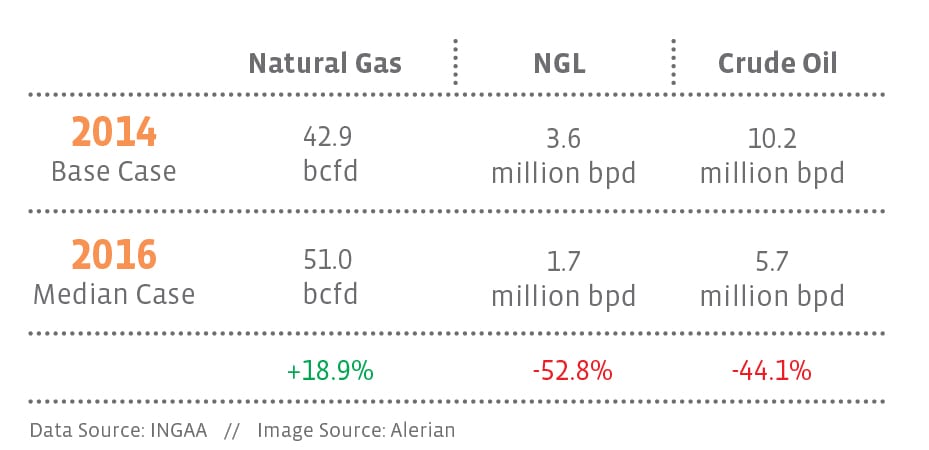

Just in case bcfd and millions of barrels per day are hard for you to imagine, the study tells us that in the high case, 329,000 miles of natural gas, NGL, and crude oil pipelines would be needed. The moon is 230,100 miles away. So if you can imagine pipelines to the moon and almost halfway back, it puts things in perspective.

If you’re interested in learning more about this topic, I highly encourage you to read the INGAA study. I’ve barely scratched the surface of all the information it contains, and it is actually very reader friendly. It’s clear from the study that the energy arena is more uncertain than perhaps it’s ever been. However, in considering the methodologies used to arrive at these numbers, it’s safe to say that traditional energy as we know it still has its place over the next 20 years. Even if you’re like me and feel more comfortable taking the low bet, $447 billion of infrastructure is still needed and that is nothing to shake a hockey stick at. Go Stars.

Edited to reword footnote regarding MLP market cap growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}