MLPs and ROC Distributions

For MLPs, return of capital distributions are often seen as an attractive tax benefit. Though there can be variability, typically about 70%-100% of MLP cash distributions are considered a “return of capital.” This is because distributions exceed the investor’s portion of the MLP’s net taxable income. This does not mean the MLP is paying out more than it can afford. Most MLPs report earnings much lower than actual cash flows after accounting for non-cash depreciation. (If you recall, this is why earnings-based metrics are not typically used to value MLPs.)ROC distributions are tax-deferred, meaning they are not immediately taxable during the year they are received. Instead, the ROC distribution will reduce the investor’s cost basis and will result in a higher capital gain (or lower capital loss) when the investor sells the MLP. As long as the cost basis remains above zero, taxes on ROC distributions are deferred until the MLP is sold, and at sale, basis reductions are taxed at ordinary income rates (1). If the cost basis is reduced to zero, future distributions are treated as capital gains in the year received. ROC distributions allow an investor to receive income while deferring taxes until a later date and potentially a lower tax bracket (e.g., during retirement). From an estate planning perspective, if MLP units are passed on to heirs, the basis is stepped up to fair market value on the date of death, and the gains from basis reductions would not be taxed.Investors who do not want to file a K-1 may choose to invest in MLPs through an index-linked product like an ETF, which distributes a 1099 form. Generally, an ETF is able to retain the tax characteristics of the distributions from its underlying securities and pass those characteristics on to investors, resulting in tax-deferred income. Read more details about MLP and MLP investment product taxation here.Most ROC in CEFs is “constructive” …

For closed-end funds, return of capital can be more complicated and can vary across asset classes. ROC can also offer some insight on the health of a fund’s distribution (with some caveats). In most cases, paying ROC distributions is an acceptable strategy for equity and alternative strategy funds to convert unrealized gains to distributions without having to sell holdings. Many like to refer to this type of ROC as “constructive.”To illustrate, it is first important to understand the sources of both CEF distributions and returns. Equity funds invest capital into an underlying portfolio of equity securities—this initial investment is referred to as the fund’s Net Asset Value (NAV). The NAV grows as the holdings appreciate in value and generate dividend income. Dividend income and realized capital gains are distributed to shareholders; however, a large portion of the fund’s gains may be unrealized. Many fund managers like to forecast the fund’s annual gains and distribute it in fixed monthly or quarterly payments to investors (much like a fixed income payment). Because unrealized gains are considered part of the fund’s NAV, distributions paid from these gains are considered “return of capital” even if the NAV is well above its initial value. This type of ROC is typically viewed positively because it provides stable distributions without unnecessary selling of holdings.…But “destructive” ROC also exists.As most investors know, market volatility can easily cause an investment to underperform expectations. If a fund overestimates its capital gains or even incurs losses, then ROC is paid from the fund’s initial NAV. This can be exactly what investors are afraid of—a return of principal. But it’s not always an issue since the underlying equities can rebound and build back the NAV. So when is it bad? Hypothetically, a scenario could arise where a fund consistently pays distributions from its NAV without adequate capital gains (e.g., if a fund can no longer afford its distribution but does not want to make a cut). Additionally, CEFs which hold fixed income securities typically should not pay ROC. A fixed income CEF’s total return mostly consists of investment income, so if it pays distributions from its NAV, it does not have the same ability to make up the loss in capital gains as an equity CEF does. Both these situations are rare, however, and are more harmful over long periods of time. Generally, as long as a fund’s total return on its NAV exceeds its NAV distribution rate, it is not actually returning principal. But if the long-term NAV distribution rate exceeds total return, it can suggest that the distribution is eating into the NAV which can diminish long-term total return potential.Bottom Line:Return of capital distributions do not necessarily imply a true return of principal, but it is still important to understand how these distributions work to take advantage of their benefits. For MLP investors, ROC distributions provide tax deferral benefits, while CEF investors might also benefit from more stable cash flows.(1) The Tax Cuts and Jobs Act of 2017 allows taxpayers to receive a deduction of 20% on qualified business income (QBI) from publicly traded pass-through partnerships, which include MLPs. This deduction also applies to the basis reductions that are taxed at ordinary income rates.Alerian is not a tax advisor or investment advisor. This piece does not constitute tax or investment advice. Please consult your tax advisor or financial advisor for information specific to your situation. Alerian’s disclaimers can be viewed here.

Current Yields vs. History

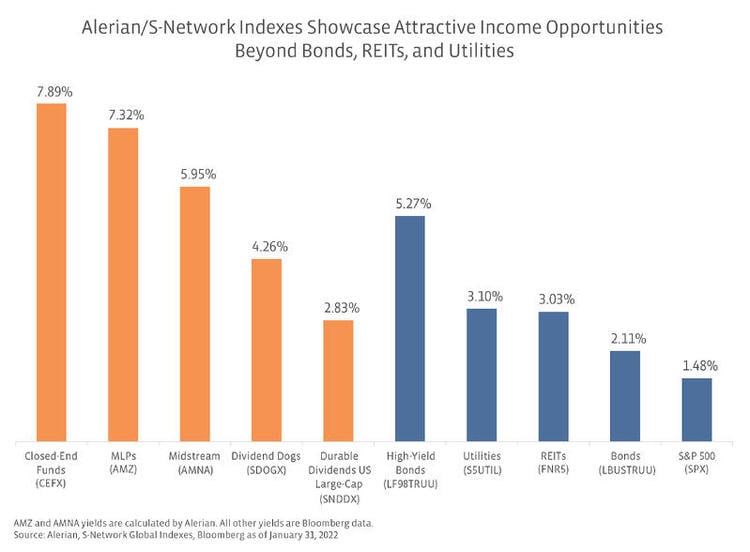

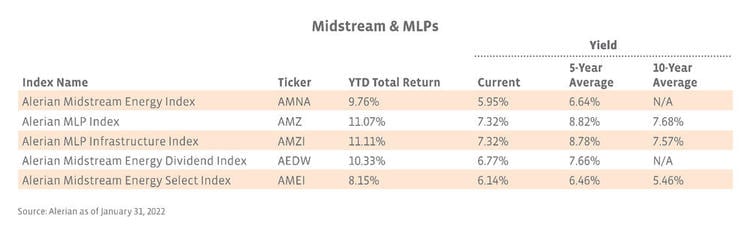

Midstream/MLPs offer both attractive yields and the potential for total return. Strength in energy prices and inflation concerns have contributed to a strong start to 2022 for midstream/MLPs. Yields are closely in line with ten-year averages.

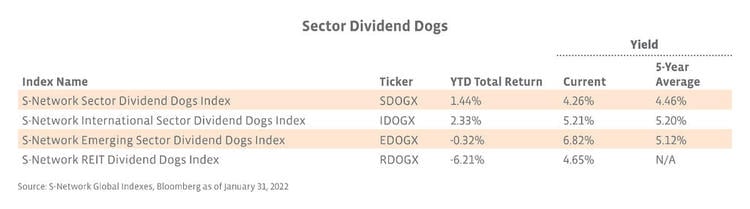

Yields offered by Sector Dividend Dogs are about in line with historical averages, with the yield for the S-Network Emerging Sector Dividend Dogs Index (EDOGX) a notable exception.

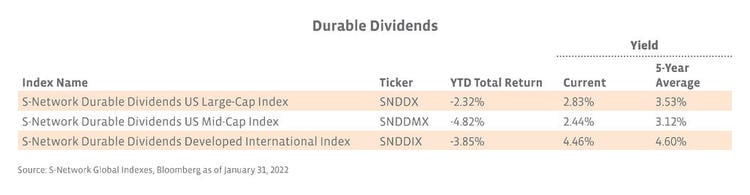

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes.

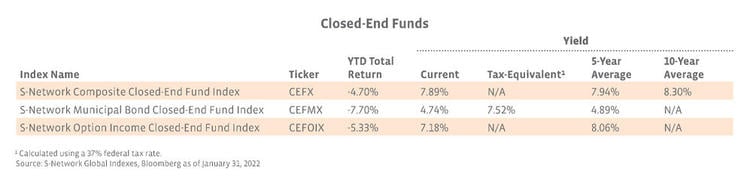

Though current yields are slightly below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio.

Related research:

MLP Exchange Traded Products Explained: ETNs and ETFs

MLPs, UBTI, ETFs, and IRAs: What You Need to Know

A Lesson on Leverage in Municipal Bond Closed-End Funds

Income Opportunities: Examining Price and Total Return in 2021

Income Opportunities with Real Assets

Income Opportunities: Finding Income in an Inflationary Environment