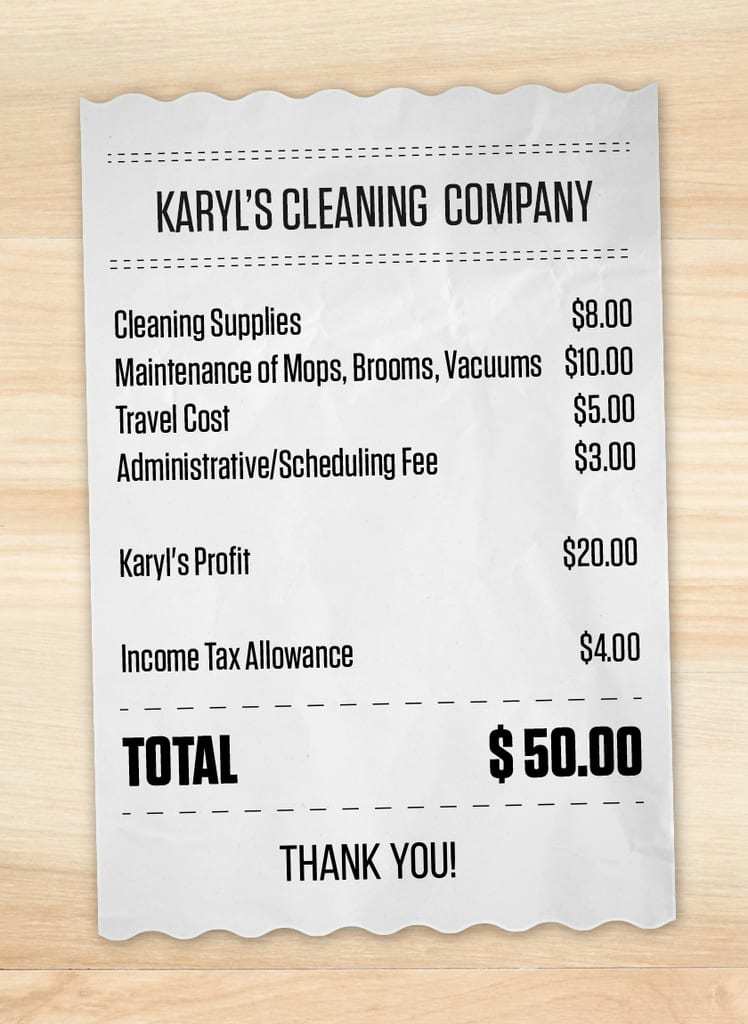

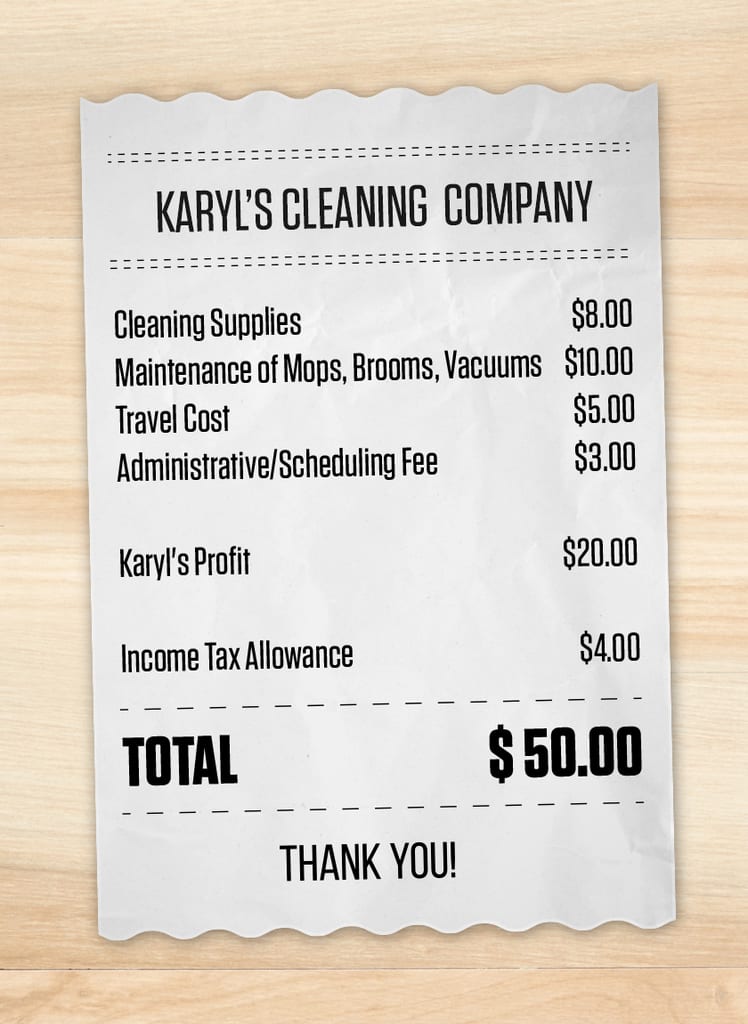

If Karyl’s Cleaning Company was an MLP regulated by the FERC, I could no longer charge that 20% (or $4) to the customer. It’s true that this doesn’t make anyone’s heart sing, but the reality is that there are several different types of rates and lots of MLPs have publicized that, due to diversification of rates charged, this announcement won’t have a significant impact on their overall earnings. Also, in keeping with the cleaning example, if I can prove that other costs have increased since the last time I decided to evaluate my prices, I could end up continuing to charge $50, or potentially even more. If you want to read about this topic in more detail, check out this blog post.

- I’ve heard that there have been a lot of simplifications and mergers happening in the MLP and energy infrastructure space, should I panic?

I’m pretty sure that panicking is never a reasonable reaction to anything (unless, obviously, you are being chased in the woods by a killer, then by all means…). It’s fair to observe there are several simplifications and mergers happening (or that have happened recently) in the MLP space. One thing to note, however, is that not all MLPs are rolling up into C Corporations. For example, in the NuStar Energy (NS) and NuStar GP Holdings (NSH) merger, NS (the MLP) will be the surviving entity. The same is true for the Alliance Resources Partners (ARLP) and Alliance Holdings (AHGP) simplification. ARLP, the MLP, will remain. My point in saying this is that although consolidations and changes are happening, it doesn’t mean it’s the end of MLPs as we know it. It just means that some company structures are “under construction” right now in order to improve long-term growth potential and overall stability. For more detail, check out Part 1 and Part 2 of our MLP Structural Simplifications series.

-

Why are MLPs performing like Fergie at the NBA All-Star Game?

There’s been a lot of noise in the MLP space with distribution cuts, restructurings, the shift to self-funding and moderating distribution growth. Arguably, these can all be described as causing short-term pain for long-term gain. At this point, we’ve just seen the pain and the aforementioned FERC announcement added insult to injury.

It’s worth emphasizing, however, that MLP fundamentals are still intact. According to the EIA, US oil and gas production is expected to see record annual growth in 2018 and this requires more infrastructure and more exports.

For MLPs to improve from here, we think a few things would help:

-

Oil price stability. The Energy Information Administration (EIA) expects West Texas Intermediate (WTI) to sit in the high $50’s for the next couple of years, though WTI crude is higher today at almost $69 per barrel.

No bad headlines. If we can go a stretch without any new announcements from governmental agencies or distribution cuts, that would be great! Operational execution should help shift the focus back to MLP’s growth projects and underlying business fundamentals.

Inflows into the space. Comfort with investing in energy would be helpful and could be supported by the improvement in oil prices.

Do you have any more questions for us? Reach out to us at [email protected] and we’ll do our best to answer your questions about the MLP and energy infrastructure space.

{kind=link}