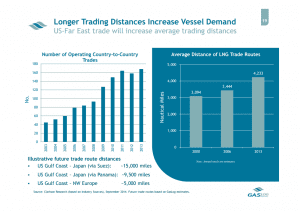

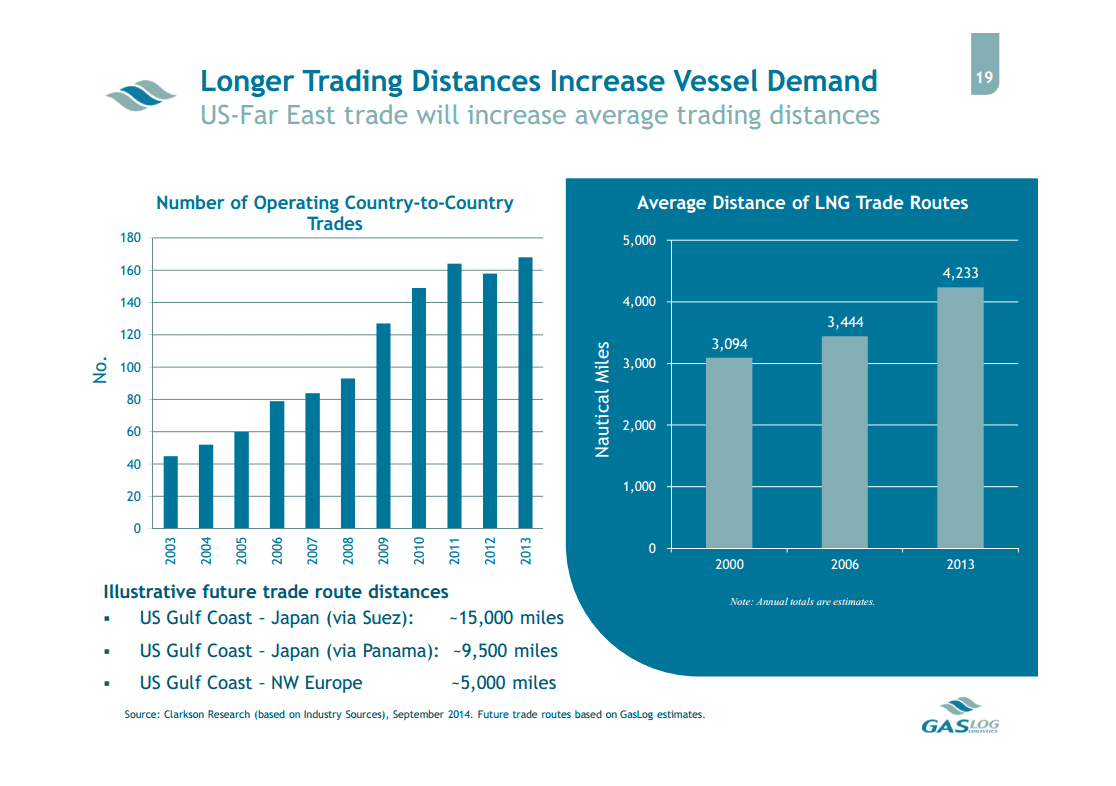

If you want to get excited about the long-term outlook for LNG shipping, look no further than slides 7 through 21. In short, growth in European and Asian demand alongside growth in North American and Australasian supply equals more vessels on the water. If that’s old news to you, perhaps the slide above isn’t, depicting a meaningful escalation in the number of operating country-to-country LNG trades over the past 10 years. With more routes comes more logistical complexity, which likely means more vessels, especially in conjunction with the supply/demand forecast for the LNG trade. The US will be adding to that number as Sabine Pass comes online in late 2015 or early 2016.

Every management team thinks its stock is undervalued and GasLog is no different. Where its executives are unique, however, is that they actually bothered to explain why.

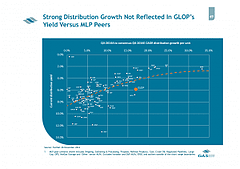

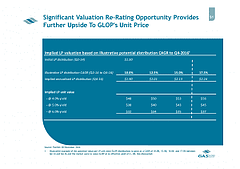

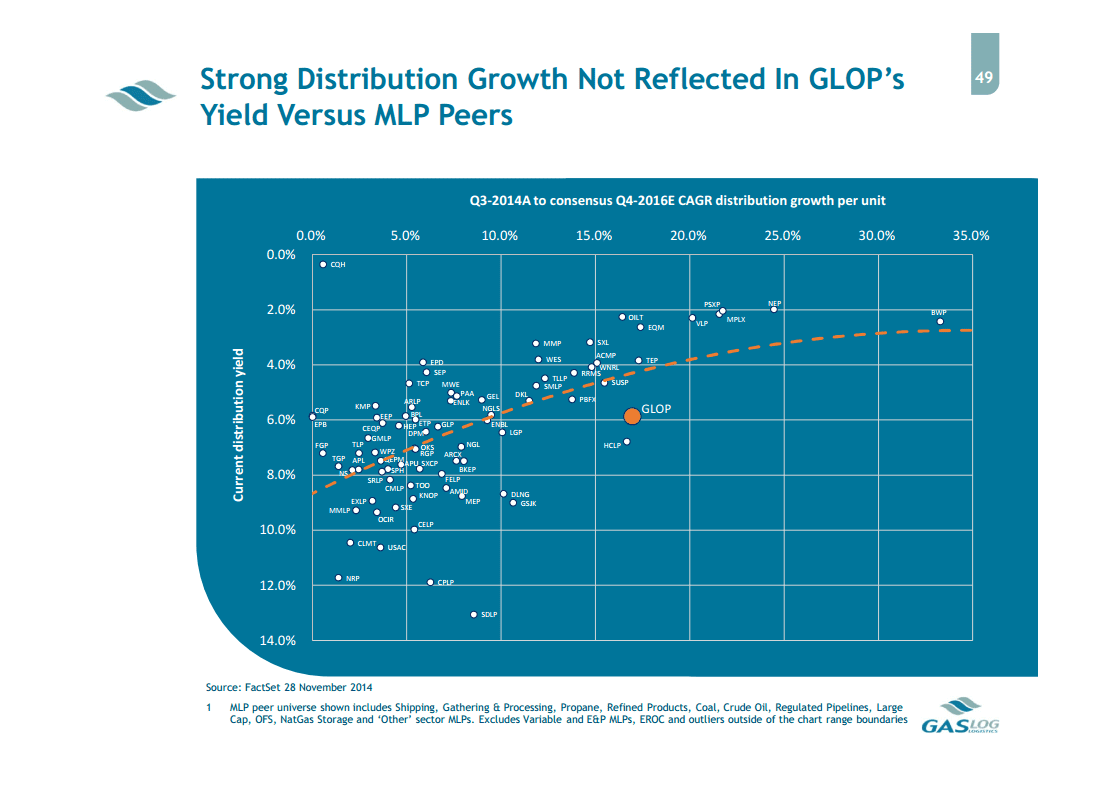

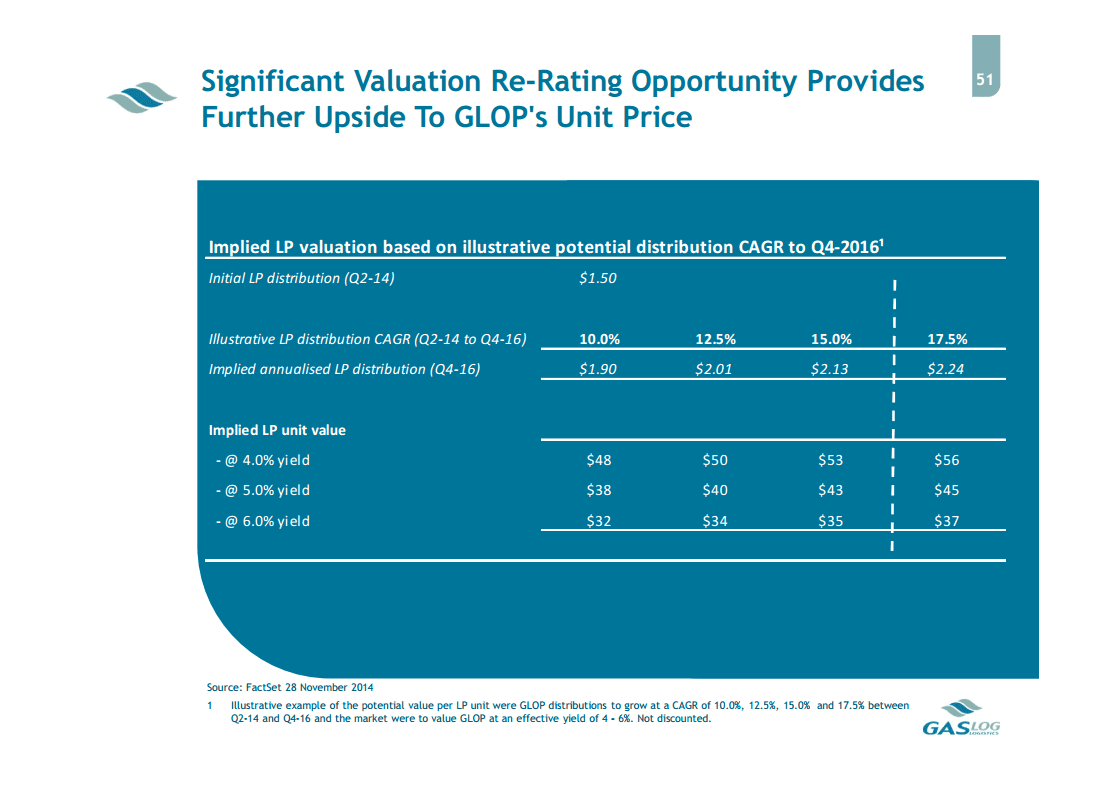

The company argues on the first slide that GLOP stacks up favorably against other MLPs in a scatterplot of current yield against expected growth. While this graph appears regularly in sell-side analyst reports and does a great job of explaining the inverse relationship between yield and growth for MLPs overall, it isn’t great for suggesting that a particular MLP is undervalued or overvalued because it lacks detail about each company’s business risks and financial situation. Few would argue, for example, that GLOP, despite higher expected growth, should trade at a yield in line with investment grade large caps like Magellan Midstream Partners (MMP), Sunoco Logistics Partners (SXL), and Western Gas Partners (WES). Per the second slide, it’s also unclear to us why investors would rerate the company’s valuation today based on fourth quarter 2016 annualized distributions.

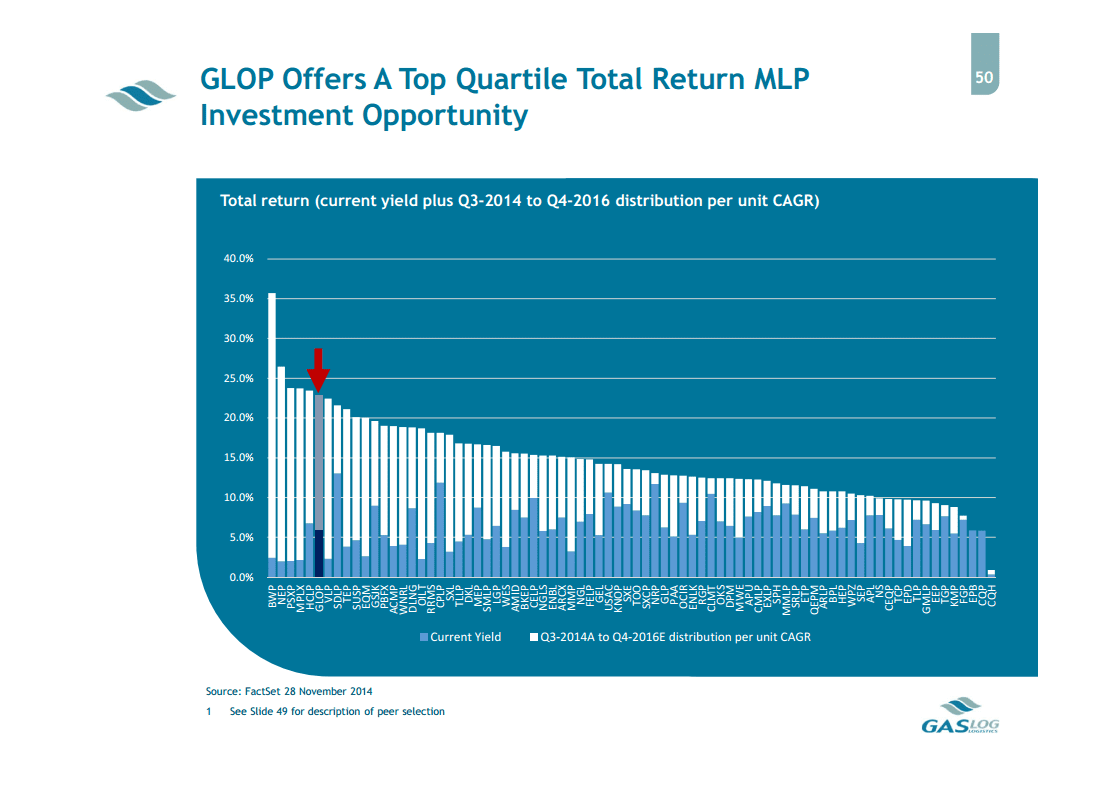

Where the company does a far more effective job of highlighting its value proposition is on the third slide, which simply adds current yield to expected growth to calculate a total return for each MLP. The reason this slide shines is that it doesn’t say anything about how to risk that total return for each company. It simply says, this time next year, we’ll have the sixth best total return in this field of 78 MLPs. Take it or leave it.

Höegh LNG Holdings and Höegh LNG Partners (slide presentation here)

Being linguistics nerds at Alerian, we love that Höegh brought its umlaut to the MLP community. The company also employed unconventional punctuation in its analyst day presentation, with an exclamation mark finding its way onto slide 6. Below we highlight two other unique slides of interest.

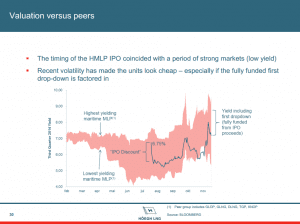

This is the first time we’ve seen a yield band time lapse in an analyst day presentation. But given that the peer group is only five companies, the graph might have been more informative if each company’s yield was shown. And though we like that management used a reasonable peer group to make the case that its stock is undervalued, we don’t believe that factoring in a dropdown at HMLP is appropriate without factoring in the dropdown plans of its peers.

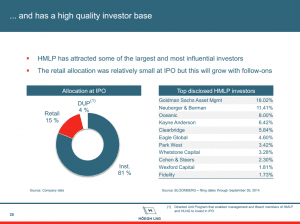

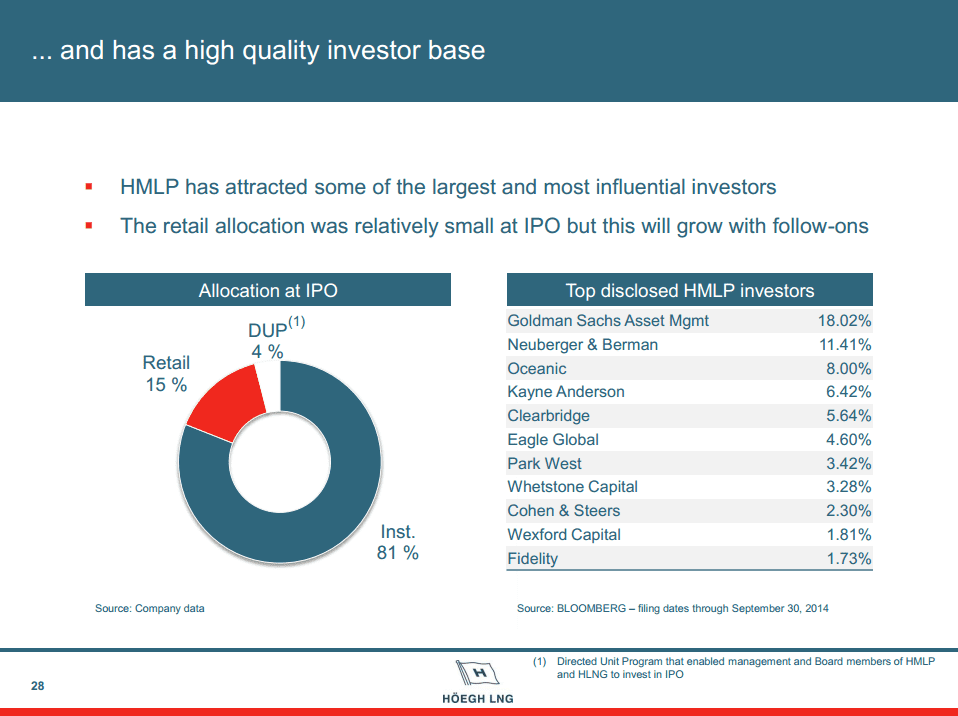

It’s rare for the general public to hear about how IPO allocations work, which is why we included the second slide. The company noted on a previous slide that 69% of the institutions that met with management during the roadshow indicated for units on the deal, the institutional book was 6.6 times oversubscribed, and 129 institutions received at least one unit in the offering. But we’re focused on the 81% institutional allocation because it’s a reminder of how much the MLP investment world has changed as compared to 10 years ago, when branch meetings were an integral part of deal roadshows and a heavy institutional book consisted of a 25% allocation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}