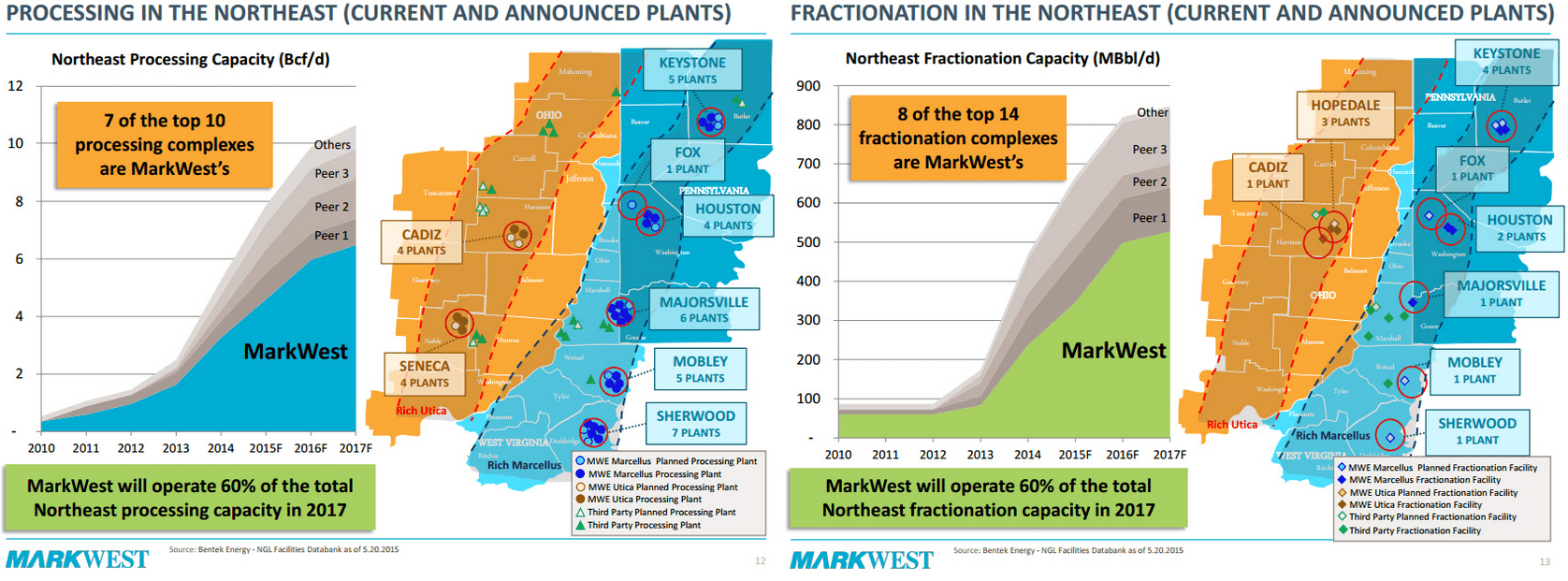

To cite some statistics about their positioning:

- MWE produces 80% of the purity ethane recovered in the Northeast

- MWE markets approximately 75% of the NGLs in the Northeast

- MWE processes 75% of the total rich gas production from the Marcellus/Utica

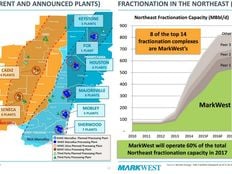

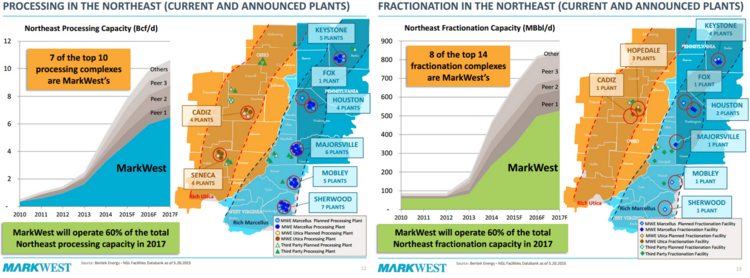

- By 2017, MWE will operate 60% of the total Northeast processing capacity

- By 2017, MWE will operate 60% of the total Northeast fractionation capacity

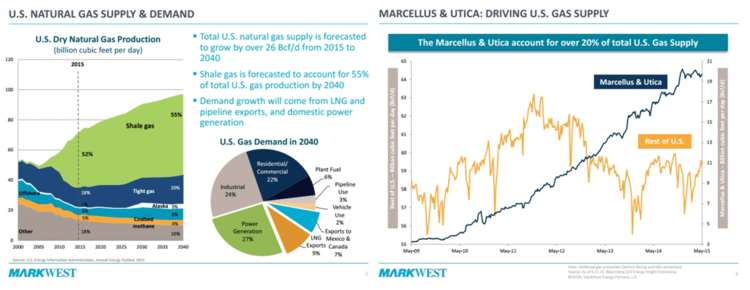

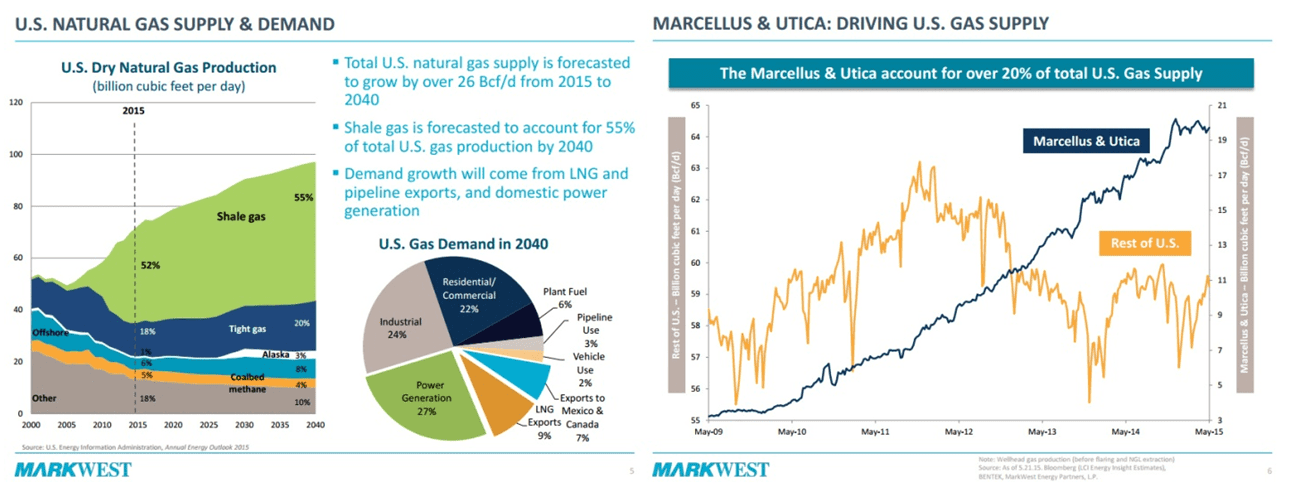

To sweeten the pot, the majority of growth in US gas production over the next 25 years will come from shale gas and 20% of the current US gas supply is from the Marcellus/Utica.

Appalachian producers (and associated G&P companies) may be doing better than their Mid-Continent peers, but capex budgets are being cut across the board. Right now, both MWE and its customers are working to weather the storm. First, MWE has moved to a just-in-time model for building processing plants. Normally employed in the management of inventory, MWE’s management is using the concept to prevent processing plants from sitting empty. Thanks to weekly conversations with producers about expected volumes, MWE is able to adjust the completion times of these facilities such that a plant is coming online just as the previous plant begins running at full capacity. As soon as the capex is spent, it begins earning a return. Now, for management to make good on their growth promises, they’ll need to balance this concept with the necessity to deploy capex.

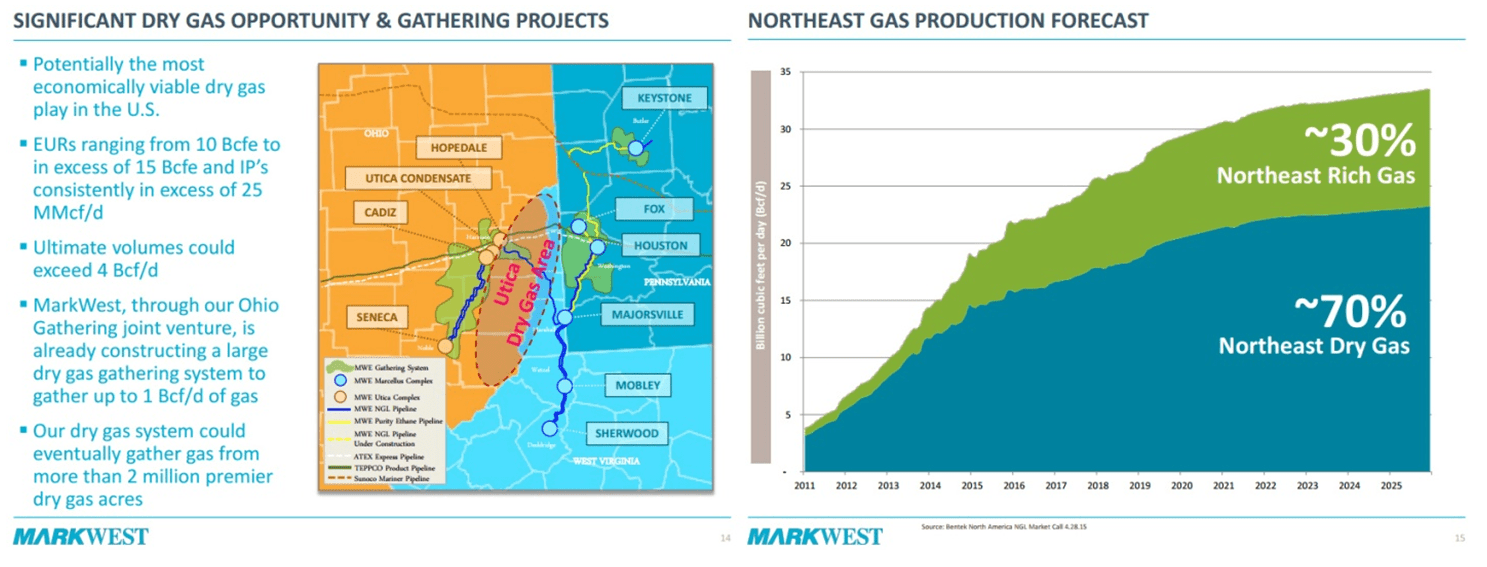

MWE is also following their customers to new areas and basins, often at their invitation. In the Utica, dry gas acreage abuts their dedicated rich gas acreage, and the customers are the same. Since their customers are allocating rigs to dry gas, MWE is also allocating capital to dry gas. On a smaller scale, they’ve gained a foothold in the Permian. Just before the analyst day, MWE announced a new plant in the Permian that will serve Cimarex Energy (XEC) and Chevron (CVX). XEC is a new customer, but MWE has worked with CVX before, and it was they who invited MWE to submit the bid.

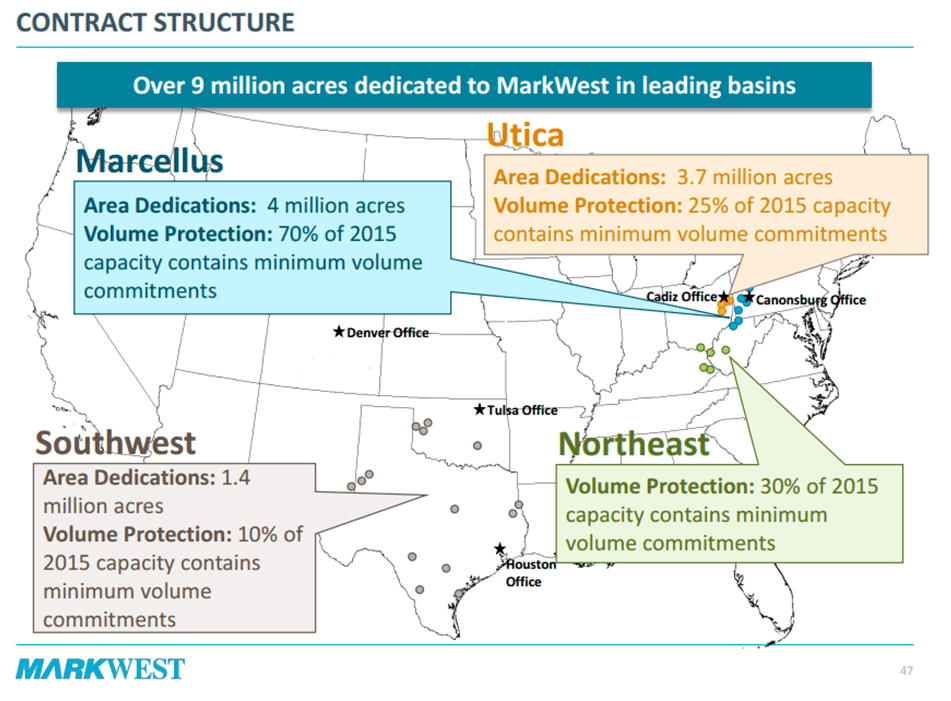

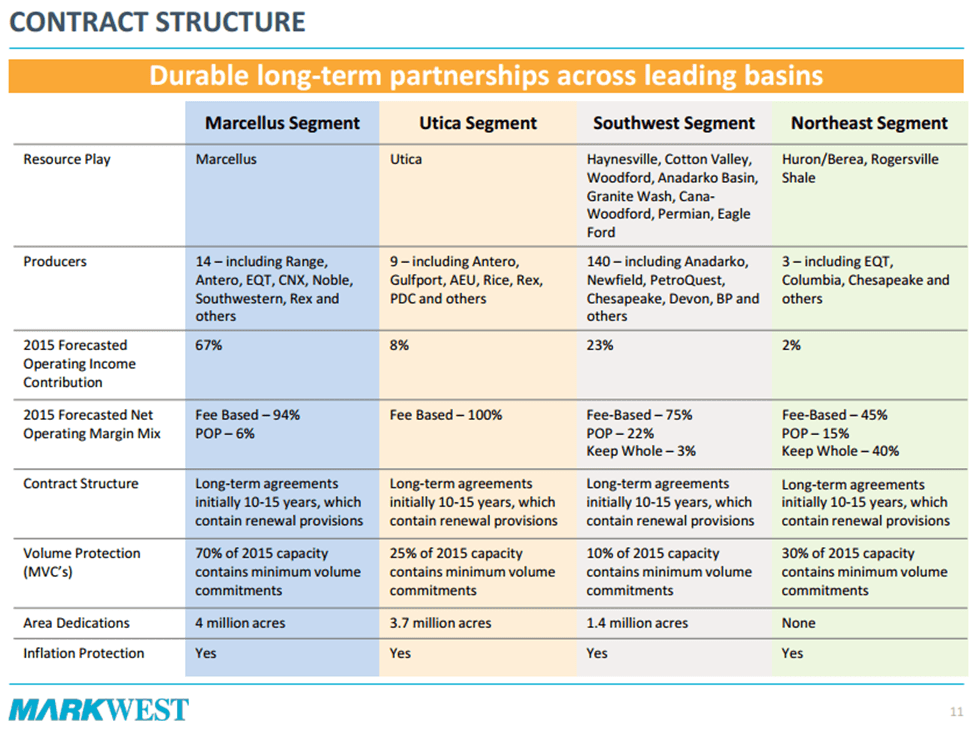

Management noted the volume of questions they get about minimum volume commitments (MVCs), but took the time to explain why they focus on dedicated acreage instead. Yes, in the short term, MVCs provide a dependable base cash flow, but negotiating hard on MVCs is not the way to get the next contract from the customer. MWE prefers to partner with its customers for the long term, and dedicated acreage makes a stronger partnership. In fact, the following is CFO Nancy Buese’s favorite slide:

As an aside, if you’re the kind of investor who wants all the nitty gritty details (aka my favorite kind), you’ll probably love my favorite slide. It has all the details: contract length, fee-based percentages, MVCs, dedicated acreage, customers, and so on, all in one handy little place:

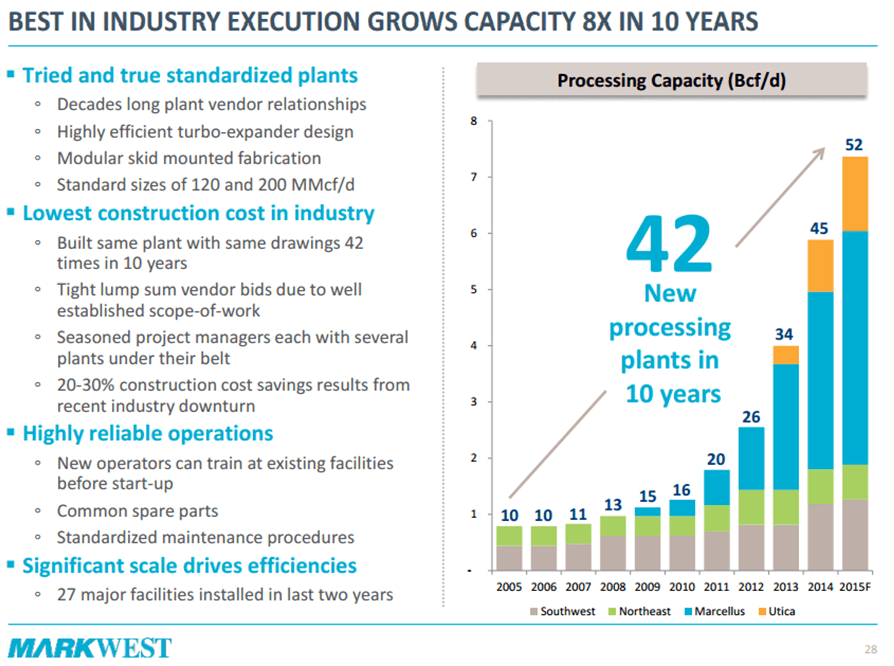

While we’re down in the weeds, let’s check out relevant trivia: What do MWE and Southwest Airlines (LUV) have in common? The way they think about their assets. This was hands down the coolest thing I learned from management. Did you know LUV has been buying 737s for decades while other airlines compete for the newest, coolest, most high-tech planes? There’s a lot of operating efficiency there: your mechanics only need to learn one manual, your pilots are familiar with every plane, and if you need a spare part, there’s probably one around. Plus, I betcha Boeing (BA) gives them a discount for buying in bulk.

MWE applies this same strategy to gas processing plants. It’s been buying the plants from the same few vendors for years. Since these vendors are predominantly located in Tulsa, labor costs are cheaper compared to building a custom plant on site. Not only are the plants built in a factory, but they fit on skids and are moved by truck. Nothing is custom—MWE offers only two plant sizes: 120 MMcf/d and 200 MMcf/d. This way, employee training is simplified since the newest plant is the same as the last plant (plus, employees can be trained at an existing facility before the new plant even arrives). Maintenance is the same across plants, and if a spare part is needed, rather than ordering a custom one that might involve longer downtimes, MWE can generally find one at another plant.

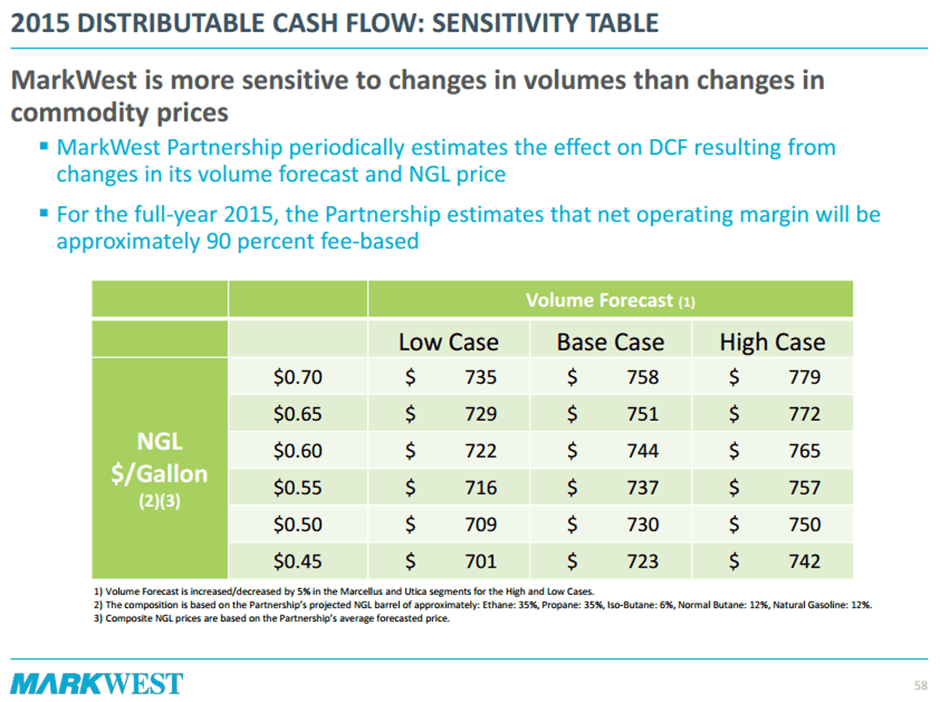

As awesome as a way as that is to operate, in the near term, commodity prices (specifically gas and NGL prices) matter much more. For those of you with a particular view on where NGL prices are going in 2015, here is MWE’s sensitivity table:

Management believes that this year will be tough ($1.5-$1.9 billion in capex spend and 5% distribution growth) and next year will be tough ($1.5 billion in capex and 7% distribution growth). But after that, when MWE expects prices to recover and takeaway capacity to come online in the Northeast (especially for residue gas) MWE will be very well positioned. In fact, this February, management gave distribution guidance further out than ever before. From 2017-2020, they expect 10% distribution growth.

Given the current commodity price environment, I have received many questions from investors about the health of gathering and processing MLPs. Since the issuance of the February guidance, I’ve been using MarkWest as an example of how a conservative management team can take the long-term view. MarkWest still has assets in the Southwest, but they put all their eggs in the Appalachia basket—it’s turning out to be a great basket.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}