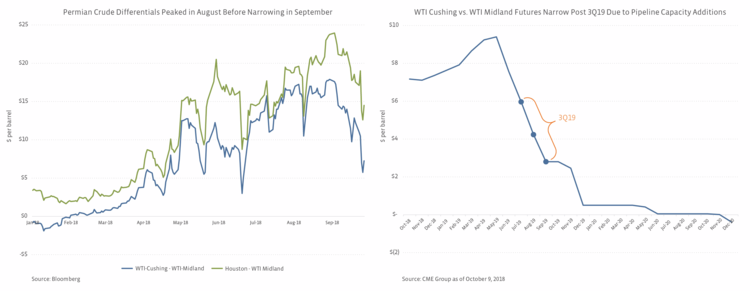

On the natural gas side, Permian differentials also remain wide with Waha natural gas prices trading at $1.93/MMBtu discount to Henry Hub natural gas prices at the end of September, though that discount has narrowed noticeably in October. Similar to crude, there are natural gas pipelines under construction to help alleviate this differential, including the Gulf Coast Express Pipeline and Permian Highway Pipeline – both being built by Kinder Morgan (KMI).

Midstream Companies with potential Permian crude insights: Enterprise Products Partners (EPD), Magellan Midstream Partners (MMP), PAA, Energy Transfer (ETE, ETP)

Midstream Companies with potential Permian natural gas insights: KMI, EPD, ETE/ETP

Cross Reference: Refiners (for crude) such as Delek US (DK), HollyFrontier (HFC), or Valero (VLO); E&Ps (for crude and natural gas) such as Pioneer Natural Resources (PXD), Diamondback Energy (FANG), or Concho Resources (CXO)

NGLs: Will there be any uplift from the price improvement?

Two weeks ago, we discussed market dynamics for NGLs, including growing production, tight Mont Belvieu fractionation capacity, and increased demand for ethane supporting Gulf Coast prices (read more). Given the 67% gain in ethane prices during the third quarter and gains for other NGL purity products priced at Mont Belvieu, investors will be looking for any incremental uplift in 3Q results related to the improved pricing. Specifically, stronger pricing should benefit companies with percentage of proceeds or percentage of liquids contracts. On earnings calls, investors will be listening for commentary around current market dynamics, how long the tightness in fractionation capacity could last, and the potential for additional growth projects related to NGLs. Investors will also listen for any color on how companies may be taking advantage of the current environment, including signing up customers for additional fractionation capacity or pipeline capacity.

Midstream companies with potential NGL insights: DCP Midstream (DCP), EPD, ETE/ETP, ONEOK (OKE), Targa Resources (TRGP), Williams (WMB)

Cross Reference: Chemical companies such as LyondellBasell (LYB) or Westlake (WLK)

Structure and Strategy

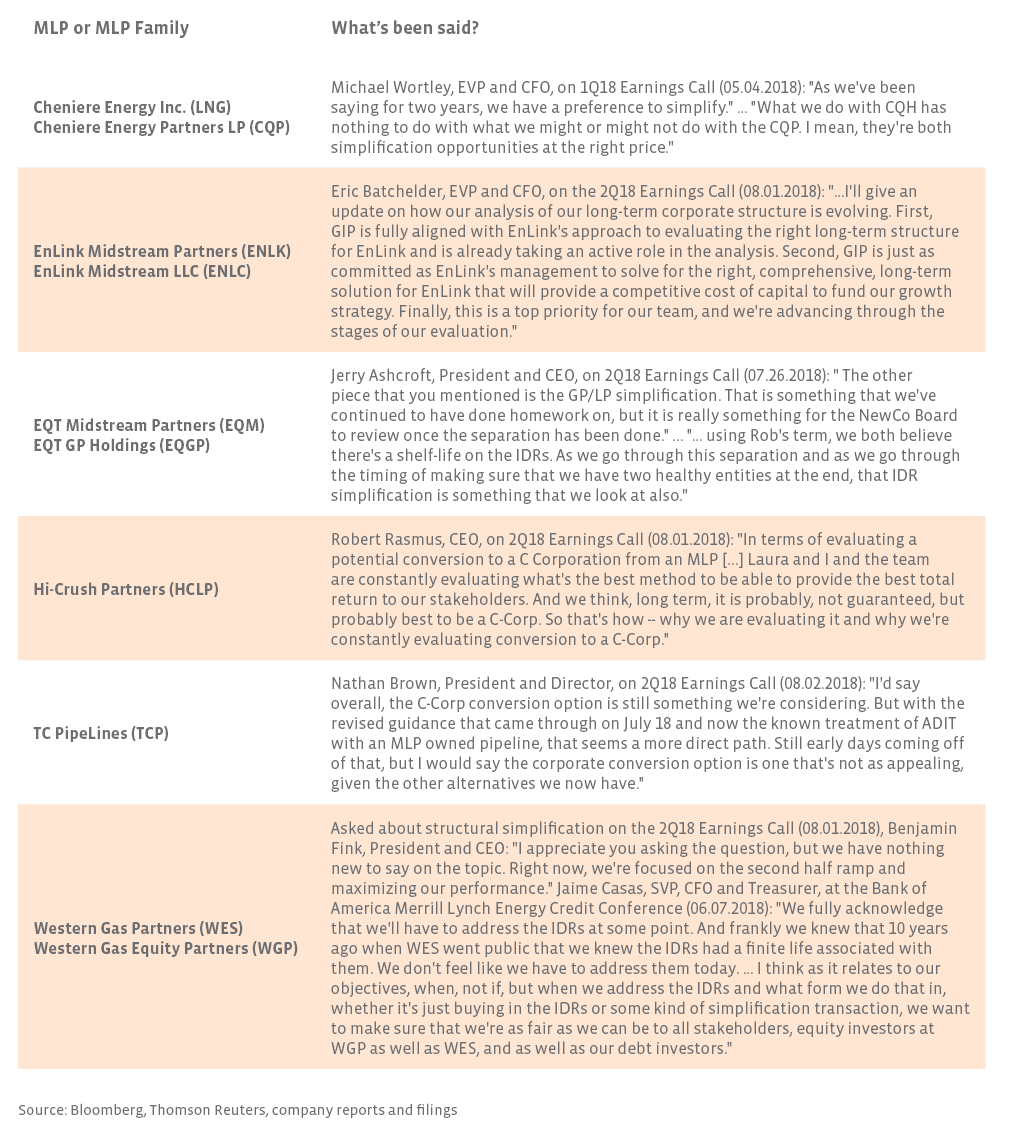

While several restructuring and consolidation transactions have been announced in recent months, some MLP families listed in Part 2 of our Bye, Bye, Bye series as potential reorganization candidates have not announced transactions. The table below provides relevant commentary from these companies, some of which has been updated since our series, and some that has not changed. We would emphasize that these comments are mostly stale, and management teams may change their views as circumstances change, with the FERC announcement in July being a notable example (see below from TC PipeLines [TCP]). Analysts and investors will likely be looking for any updates on how these companies (and potentially others) may be thinking about corporate structure.

In terms of other strategic or structure-related topics, MLPs that still have IDRs, such as PSXP or Shell Midstream Partners (SHLX), may receive questions around how management views IDRs. Buckeye (BPL) announced with its 2Q18 results that it had hired financial advisors to help with a review of BPL’s asset base and financial strategy. On the 2Q18 call, BPL management indicated that they would discuss the results of the review on the 3Q18 call.

Proposition 112 a topic for those with Colorado exposure.

Without going into too much detail (something we plan to do in a future post), Colorado’s Proposition 112 “proposes amending the Colorado statutes to require that new oil and natural gas development be located at least 2,500 feet from occupied structures, water sources, and areas designated as vulnerable” (source). The ballot initiative has created some uncertainty for future oil and gas development in Colorado, which has implications for midstream. Analysts will probably ask about sentiment in Colorado and recent poll results related to the initiative. DCP is one of the largest midstream providers in Colorado and is holding its 3Q earnings call on Election Day, as is Denver-based E&P PDC Energy (PDCE), which operates in Colorado’s Wattenberg Field. On its 2Q18 call, management of DCP discussed the Colorado political climate and noted that similar measures have not been successful in the past.

Midstream companies with exposure to Colorado: DCP, Noble Midstream (NBLX), Tallgrass Energy (TGE), Western Gas Partners (WES)

Cross Reference: E&Ps with Colorado footprints such as Noble Energy (NBL) – call on 11/1, PDCE, Anadarko Petroleum (APC) – call on 10/31

Weather impacts to keep in mind.

When comparing 3Q18 to 3Q17, keep in mind that 3Q17 results for some companies were negatively impacted by Hurricane Harvey, which could complicate comparisons. Additionally, while Hurricane Michael was a 4Q event, investors may ask about potential impacts, even though the storm seemed to mostly skirt Gulf Coast energy infrastructure. The Louisiana Offshore Oil Port (LOOP), for example, suspended operations ahead of the hurricane at its marine terminal. Hurricane Florence, which impacted the East Coast in 3Q18, was more likely to be a hindrance to pipeline projects being built in that area. For example, EQM Midstream (EQM) cited activities around hurricane preparation as an interruption to construction activities for the Mountain Valley Pipeline.

{kind=link}

{kind=link}