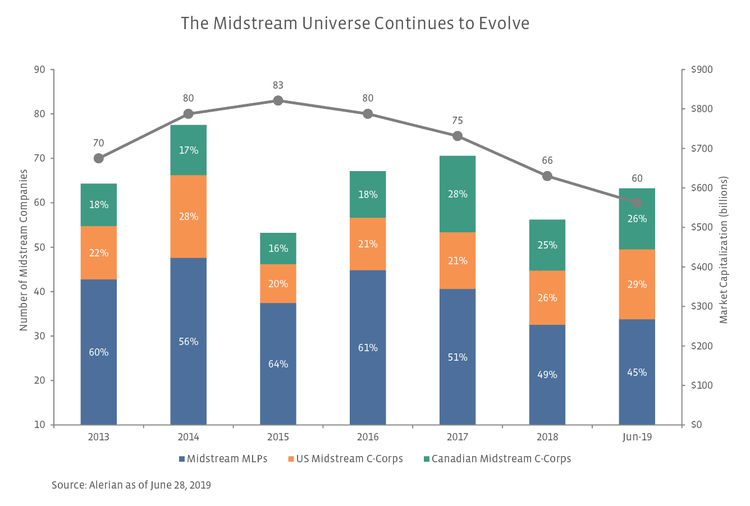

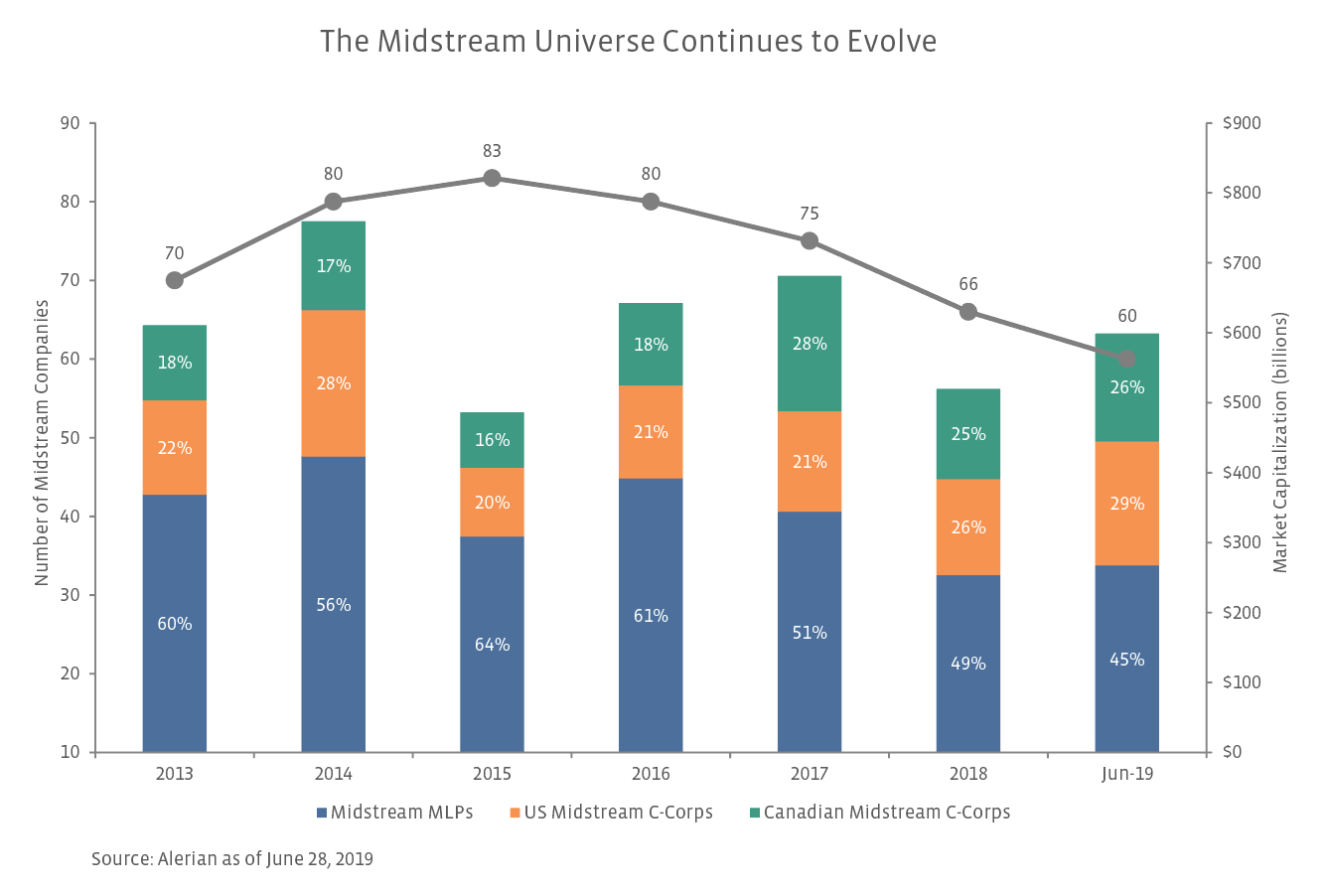

While market cap information is helpful, investors also often ask about the number of midstream MLPs. The Alerian MLP Index (AMZ), which includes midstream MLPs with a market capitalization of at least $75 million, currently has 35 constituents. The Alerian MLP Infrastructure Index (AMZI), which is a subset of the AMZ and includes larger, more liquid MLPs, has 23 constituents. Both indices currently include Buckeye Partners (BPL) and Andeavor Logistics (ANDX), whose acquisitions are expected to close in 2H19. With fewer midstream MLPs, it becomes more difficult for MLP products focused on midstream to differentiate themselves from a security selection standpoint. There are only so many large, investable midstream MLPs from which to choose. Passive managers argue that this strengthens the case for accessing the space using a passive product, while active managers will argue that this landscape requires more nimbleness and selectivity that can only be provided by active management. As an index provider, you can guess where we land in this argument! You can read more about active and passive investing in the MLP Investing section of our MLP University. Though the number of MLPs has decreased, there is the potential for new MLPs to come to market.

Could more midstream IPOs be on the way?

The initial public offering (IPO) of Rattler Midstream (RTLR) in May broke a dry spell of MLP IPOs that had persisted since BP Midstream’s (BPMP) IPO in October 2017. RTLR priced at the midpoint of the range in an upsized offering and has gained 11.1% since its IPO on May 23 through July 12 relative to a 3.0% gain in the AMZ Index over the same period. Permian-focused RTLR is unique in that it is structured as an MLP but has elected to be taxed as a corporation and does not have incentive distribution rights (IDRs). Because IDRs are out of favor with investors, we would expect any new MLPs to exclude them from their structure in the same way as RTLR. However, we wouldn’t necessarily expect future MLPs to elect to be taxed as corporations. The MLP structure remains the most tax-efficient way to own midstream assets. Keep in mind, RTLR’s parent, Diamondback Energy (FANG), is also the parent of Viper Energy Partners (VNOM), which is a variable distribution MLP that elected to be taxed as a corporation last year.

The positive reception to RTLR may pave the way for additional midstream IPOs, whether structured as MLPs or corporations. Bloomberg reported in late June that privately-owned Blue Racer Midstream was considering an IPO, though details were scant. Given significant private equity (PE) involvement in midstream (read more), PE firms may pursue an IPO as a potential exit if the equity markets for midstream remain constructive. On the other hand, Howard Midstream Partners, which initially filed a registration statement in 2017, withdrew its registration request in late June 2019. While another midstream IPO does not appear to be imminent, the success of RTLR is not lost on those that may be waiting in the wings, and future IPO activity bears watching.

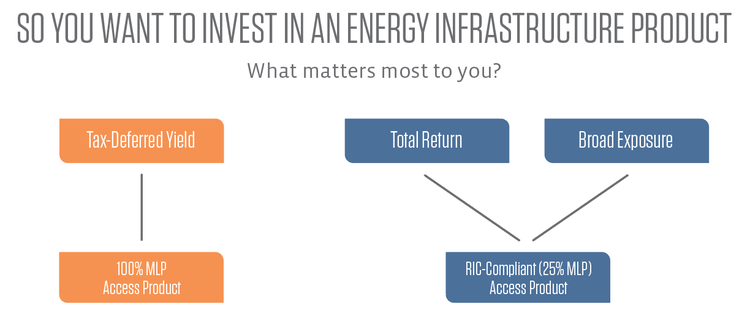

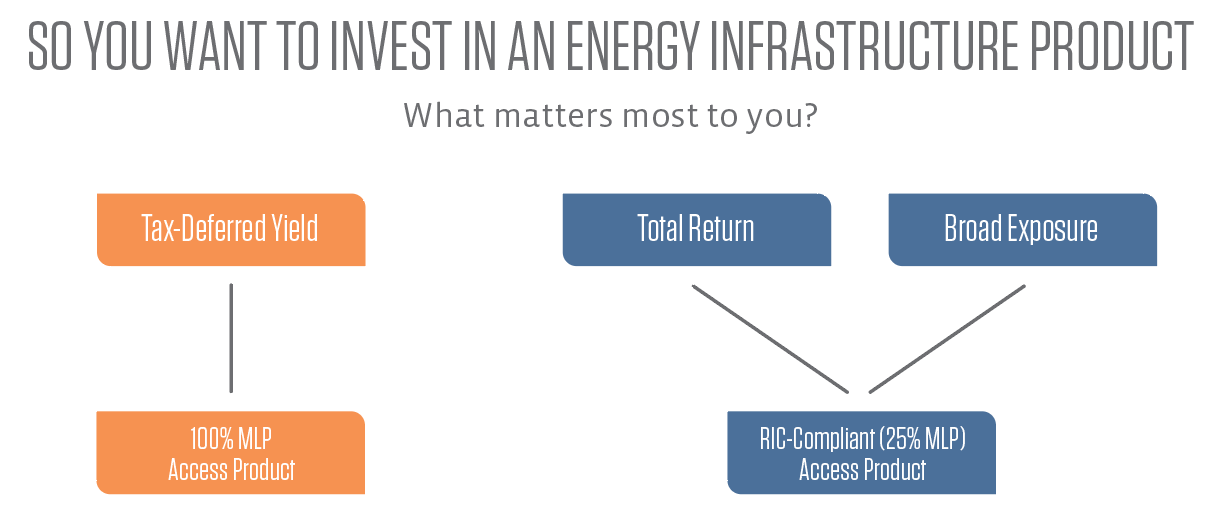

What does the changing midstream landscape mean for investors

In the past, access products that primarily invested in MLPs provided both yield and broad diversification in one product. As a result of consolidations, MLPs are not as representative as they once were. Consequently, investors must choose what is most important to them when accessing the midstream space.

From a product standpoint, there are two main types of MLP funds – C-Corp funds and RIC-compliant funds. We discuss these product types in detail in the MLP Investing section of our MLP University as well as in a January post on MLP access products. In short, any fund that owns more than 25% MLPs will be taxed as a corporation and may experience tax drag when the underlying equities are gaining. A RIC-compliant fund owns less than 25% MLPs and is not taxed at the fund level, providing little or no tracking error. (For a quantitative comparison of two of our midstream indices that represent these two main product types, please see this post from last month).

So, what MLP product may be right for you? Many investors are using MLPs for income, and an access product that predominately owns MLPs is still the best option for maximizing tax-deferred income. A RIC-compliant fund may be a better fit for investors primarily interested in total return (less focused on income) and broad exposure to the midstream space. As a word of caution, it’s important to make sure the other 75% in a RIC-compliant product provides the exposure investors want.

Consolidations concluding could serve as a catalyst.

As discussed last week, we believe that consolidations are largely behind the MLP space, as many companies have already simplified their structures. As transaction activity subsides, investors that have waited on the sidelines for calmer waters may start to dip their toes back into MLPs, which would be supportive for equities. Structure questions have likely served as a distraction from positive trends, including MLPs’ shift to self-funding equity, leverage reduction, improved distribution coverage, and the overall strong fundamentals provided by growing US energy production. In addition to removing distractions, consolidations subsiding also helps alleviate uncertainty, making for a cleaner, more investable space.

{kind=link}

{kind=link}