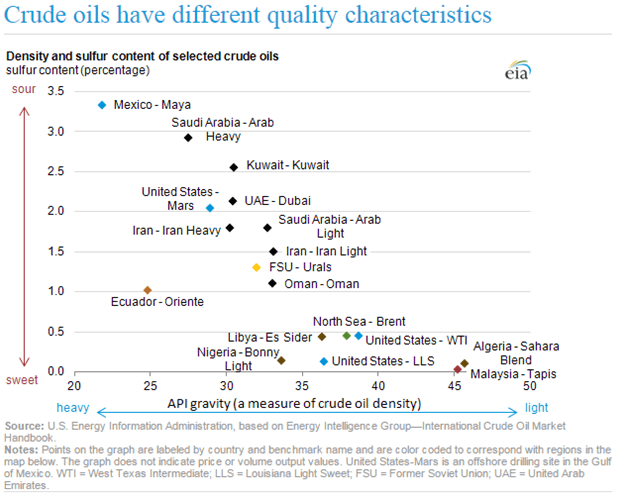

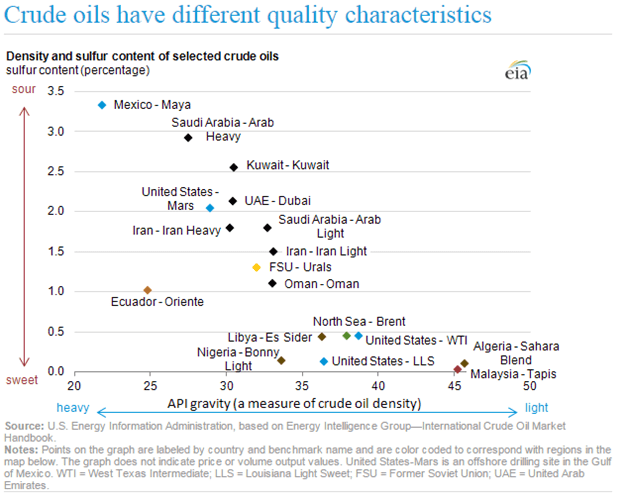

Historically, Brent and WTI have tracked closely in price to each other. However, beginning in 2013, conversations that usually centered on WTI were increasingly focused on Brent. As US crude oil production increased, domestic infrastructure was unable to keep pace, leaving a great deal of oil trapped in Cushing and driving the price of WTI down. Brent consequently became more reflective of global oil prices. In 2014, LLS, which is the less commonly mentioned US Gulf Coast light sweet crude benchmark, became more relevant because of the volume of oil present there, unable to be exported. Today, we’re talking about all three benchmarks, because we’ve yet to come to a consensus about which should be most quoted.

For MLP investors, spreads have little impact on short-term MLP cash flows. However, a wide spread for a sustained period of time between two crude benchmarks that share similar characteristics may imply that infrastructure or legislative measures are needed to equalize the supply/demand imbalance. We could spend longer discussing the implications of new pipelines or the lift of the crude export ban; however, the purpose of our post today is primarily to help you navigate the jargon and to understand the significance of benchmarks. We hope we’ve done that because our readers are our BFFs. TTYL.

{kind=link}