In a previous mailbag, you discussed how the Federal Register released proposed regulations on qualifying income in early May. I heard the comment period ended on August 4th. Can you give an overview of the comments and tell me when the final regulations will be published?

The Dallas Cowboys kicked off their preseason last Thursday night against the San Diego Chargers. While the final score wasn’t in favor of Dallas, Jameill Showers had a decent showing, giving hope for the future of Cowboy Nation.

At no point in any game during this week’s preseason lineup did NFL referee Ed Hochuli stroll onto the field in his snug-fitting shirt to announce the rules had changed. If this had happened, I’m pretty sure the internet would have broken and Ed would be under more stress than he was after that Broncos/Chargers debacle in 2008. As ludicrous as changing the rules in the middle of an NFL game may seem, this is the equivalent of what some investors say the IRS did when it released the proposed regulations on qualifying income three months ago.

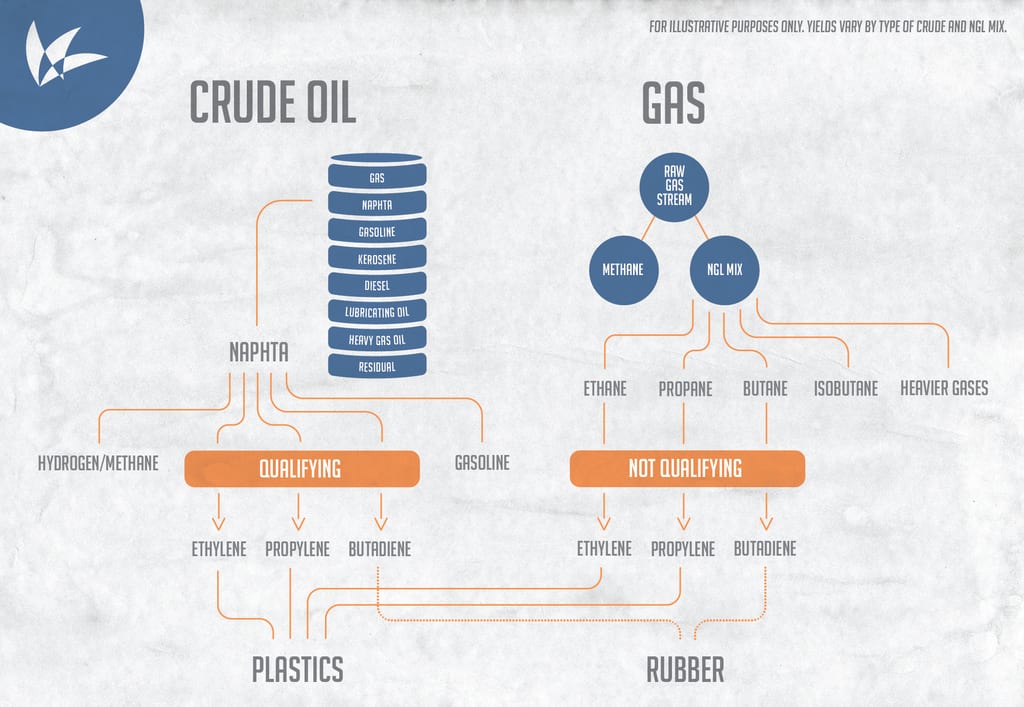

Investors in Westlake Chemical Partners (WLKP) are booing the IRS’ call (helped by WLKP’s page dedicated to the matter) to exclude from qualifying income the processing of natural gas liquids (NGLs) into ethylene. The IRS’ decision is undoubtedly a rule change, given that WLKP received acceptance of the activity in the form of a private letter ruling (PLR) ahead of their August 2014 IPO.

Luckily, unlike in a packed stadium where fans yell, “Stevie Wonder saw that one” (among other insults that might be pushing the envelope to include in a mailbag post), the IRS welcomed comments. Over 130 stakeholders weighed in on the matter and many of them were WLKP investors.

In addition to the Westlake supporters, there were carefully crafted comments from law firms, the Master Limited Partnership Association (formerly known as the National Association of Publicly Traded Partnerships), the Louisiana congressional delegation, energy industry associations, 21 MLPs, and other companies that are not currently MLPs, but may one day hope to be. Vinson & Elkins provides an amazingly organized list that links to comments by organization, type, and topic.

Broadening the current definition of processing and refining was the most contested issue in the comments. As it stands in the proposed regulations, “activities that cause a substantial physical or chemical change… or that transform the extracted mineral or natural resource into new or different mineral products, including manufactured products” are not qualifying. The problem here is that when a company refines crude oil in a manner that is necessary to the “cost effective” production of gasoline or other fuels, resulting ethylene, propylene, and butadiene (“olefins”) production is considered qualifying. However, when the exact same olefins are formed as a product of NGLs from the gas stream, they aren’t qualifying. This is like telling your daughter, Mae, that she can make and sell lemonade, but sorry little Benny, you can’t.

{kind=link}