The IRS announced the end of the PLR pause. When will they release the newly proposed regulations?

Let’s start with an analogy. Each year around this time, anxious high school seniors across the country wait by the mailbox for college acceptance letters. Students must make a decision about where they will spend the next four years and parents try not to meddle as their almost-adult children weigh their options.

In early March, the Internal Revenue Service (IRS) announced that it was ending its pause on issuing private letter rulings (PLRs) to companies asking whether a particular asset or activity would generate qualifying income. While stakeholders were pleased to learn of this development, a month has now passed, and the MLP community is still waiting to receive clarity from the IRS. It’s almost as if the high school senior emerged from her bedroom and announced, “Mom, Dad: I’ve decided where I’m going to college, and I’ll tell you…sometime.”

According to the IRS’ official statement, “P&SI [Passthroughs and Special Industries] is resuming the ruling process as of today [March 6, 2015], and is beginning to review the pending ruling requests, notwithstanding that we have a guidance project ongoing and that the proposed regulations, which are intended to provide greater transparency, are still being developed.” In other words, while the IRS has made “significant progress” in the process of deciding what does or does not generate qualifying income for an MLP, it has yet to finalize regulations for review.

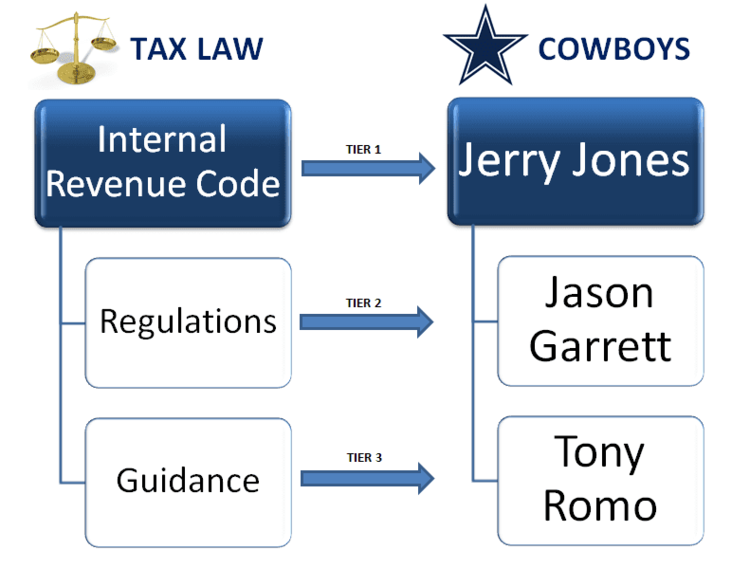

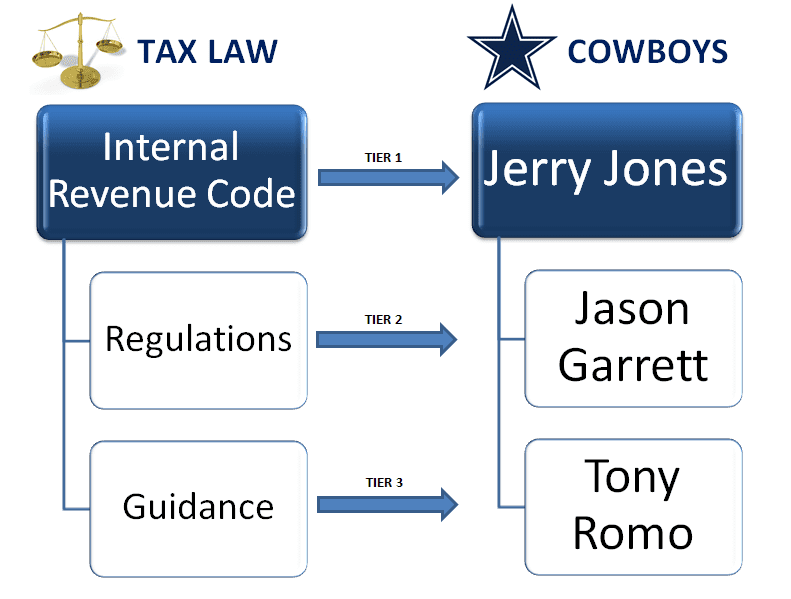

The regulatory process is fascinating. There is an entire chain of authority when it comes to tax law. As a Texas girl who is counting down the minutes to September, I decided a diagram that related the tax law hierarchy to the Dallas Cowboys’ org chart could give us a glimpse of fall as we settle into spring.

(Note: The IRS doesn’t use the term “Tiers,” that’s something I’ve included for purposes of making tax authority more understandable.)

Up until now, the IRS has been using PLRs (which fall under Guidance/Tier 3) to clarify Section 7704 of the Internal Revenue Code. It’d be like Jerry Jones telling Zack Martin the team rules and Zack later asking Tony Romo for further clarification. When the IRS releases its regulations, those will be considered Tier 2 and will have more authority, i.e., Mr. Martin visits Jason Garrett’s office to receive official interpretation of Jerry’s rules.

After a proposed regulation is issued, it is posted to the Federal Register where public comments are accepted. Typically, the agency will allow a 60-day comment period, but times can vary. Some proposed regulations can receive thousands of comments.

Unfortunately, we don’t have any insider information on how long it will take for the IRS to post the proposed regulations. We did a little digging to find out the cadence of past IRS issuances, and it’s nearly impossible to glean anything concrete when it comes to regulations (Tier 2). We found a few examples of guidance, however. Roth after-tax issues remained “”text-decoration: underline; color: #3366ff;">an open question for years and years." Yet, when the Supreme Court’s decision invalidated sections of the 1996 Defense of Marriage Act, a revenue ruling was issued just two months later to align the tax code with the verdict.

In reading the aforementioned statement released by the IRS regarding the end to the pause, it seems as though the IRS intends to keep the process moving and we hope this same spirit will apply to the release of the proposed regulations.

In much the same way, our high schooler may have great intentions of announcing her choice of institution; she just might want to iron out the details of her class schedule, financial aid, dorm, and meal plan before she buys a t-shirt and posts the news on Twitter.

{kind=link}