What is the difference between a RIC and a non-RIC fund?

As an eight-year-old, I had a secret infatuation with professional wrestling. I’m pretty sure it’s because my mom told me not to watch it, and also because it gave me an excuse to practice my big splash, which involved belly flopping on my grandmother’s bed after getting a running start. Ric Flair was the hottest wrestler around in those days, and while his wrestling career may be a memory, many investors still wrestle with the difference between a RIC and a non-RIC fund.

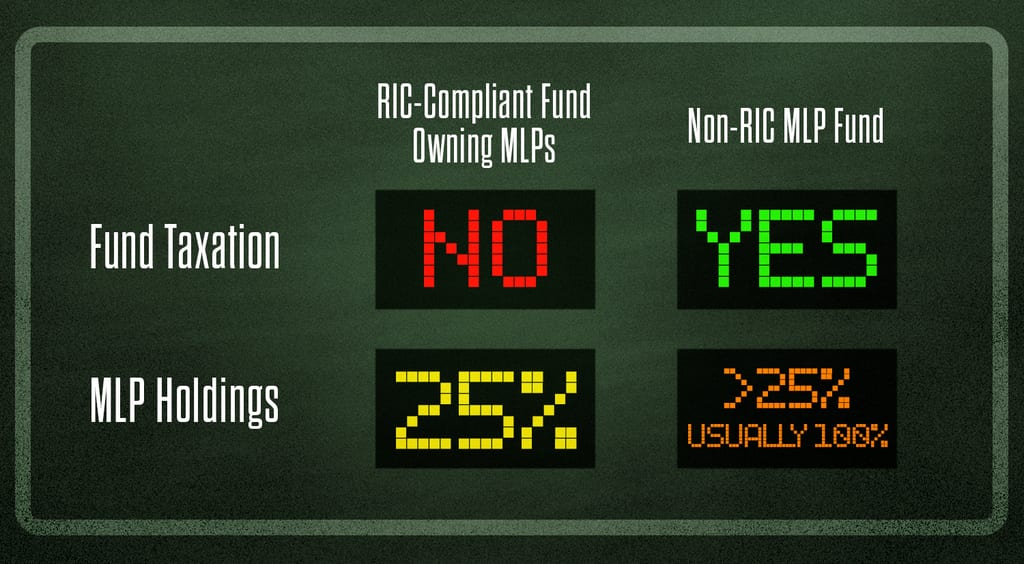

A regulated investment company (RIC) is a company registered under the Investment Company Act of 1940. The word “company” can be confusing and isn’t referring to companies like Apple or Google. Instead, an “investment company” issues securities and is primarily engaged in the business of investing in securities. Section 851 under Subchapter M of the tax code spells out the definition of a RIC. To summarize, at least 90% of its gross income must be derived from dividends, interest, and capital gains. The benefit of a RIC structure is that the fund is eligible to pass the taxes on this income directly to fund investors, thereby eliminating double taxation. The vast majority of funds known to the general investing public are RICs.

But for MLP investors, there is an important caveat: the line item found under “Limitations” which states that a RIC must not have more than 25% of the value of its total assets invested in publicly traded partnerships..

The term “RIC-compliant MLP fund” isn’t really a thing anymore than a fireball is supposed to be a thing in the world of professional wrestling attacks. If a 40 Act fund is RIC-compliant, its direct stake in publicly traded partnerships is less than 25%. In other words, you likely wouldn’t consider a pizza to be for meat lovers if a quarter of it was topped with pepperoni and Italian meatballs and the remainder was piled high with veggies.

If an investor is seeking more than 25% exposure of MLPs in a fund, the alternative would be a fund that is not RIC-compliant. These funds typically own 100% MLPs and have elected to be taxed as a corporation at the fund level (bringing back the double taxation). These funds have been termed “C corp MLP funds” by investors.

In the chart below, the simple differences between a RIC-compliant fund owning MLPs (notice I didn’t call it a RIC MLP fund) and a non-RIC-compliant MLP fund are reflected.

{kind=link}