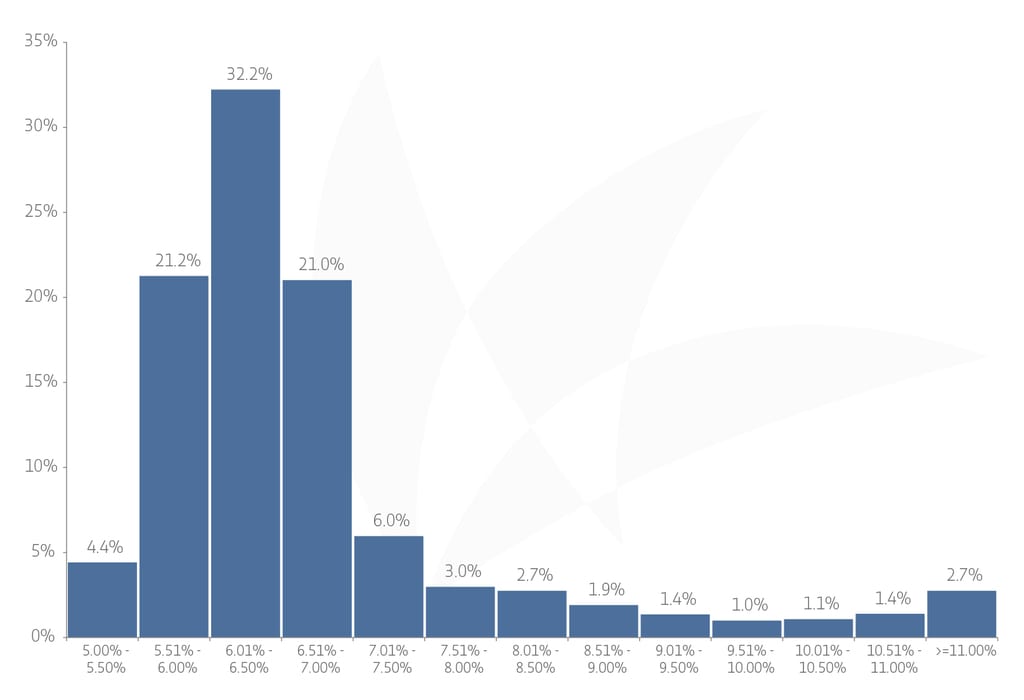

Yield should not be used as the sole basis for an investment decision, because it fails to take into account the security of the income and/or a company’s growth prospects. That said, especially on a relative basis, yield can provide an investor with some quick insight into marketplace considerations.

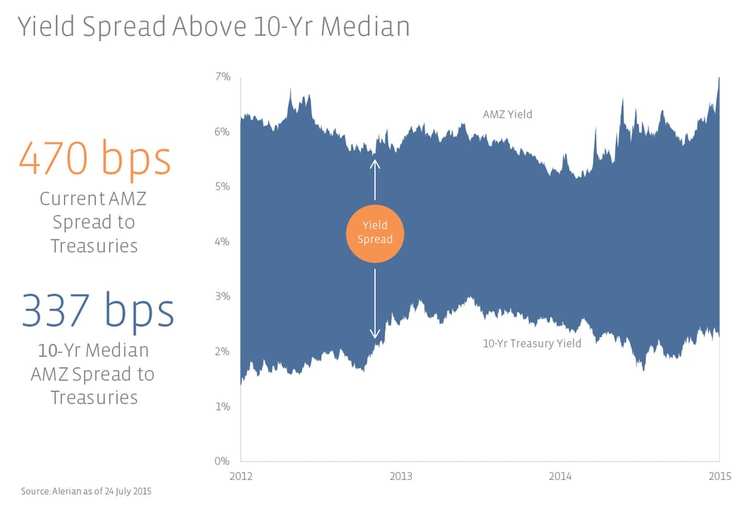

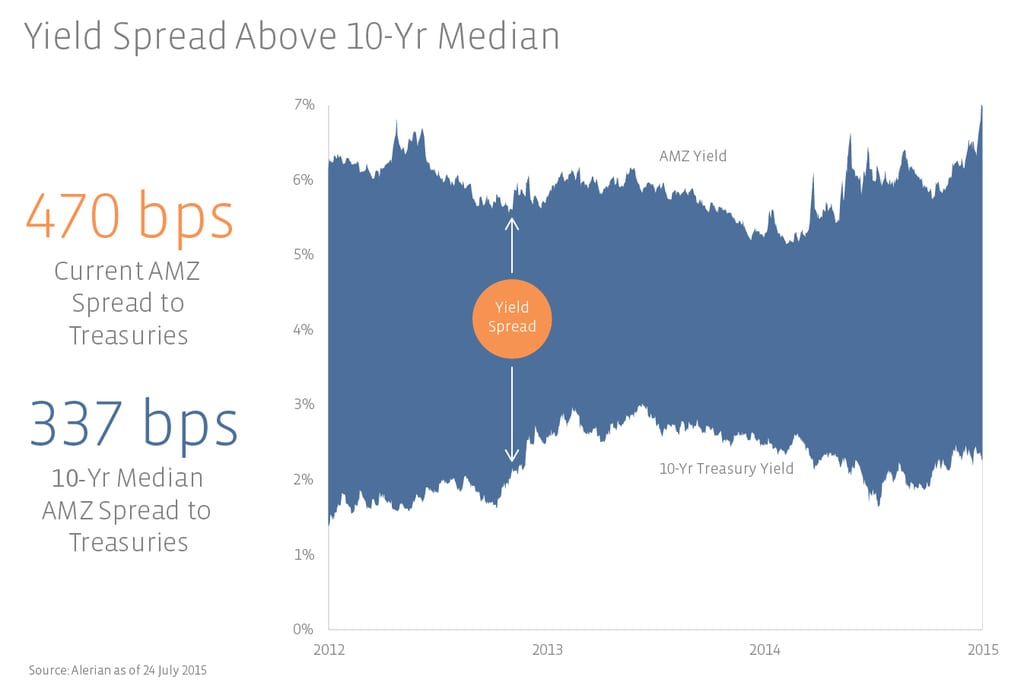

Last Friday (July 24th), the 10-year Treasury closed at 2.27%, while the AMZ rounded out last week yielding 6.96%. This puts the current spread at 469 bps, which is well above the 10-year median of 337 bps.

What does this mean? The above-average spread could indicate that investors are pricing MLPs with the expectation that the 10-year Treasury rate will increase 132 bps in a year’s time. Personally, I don’t know where 10-year Treasury rates will be in the next year, but I do know that 3.59% is higher than what the 30-year Treasury is yielding currently! It’s been about four years since stakeholders have seen the 10-year Treasury rate exceed 3.59%.

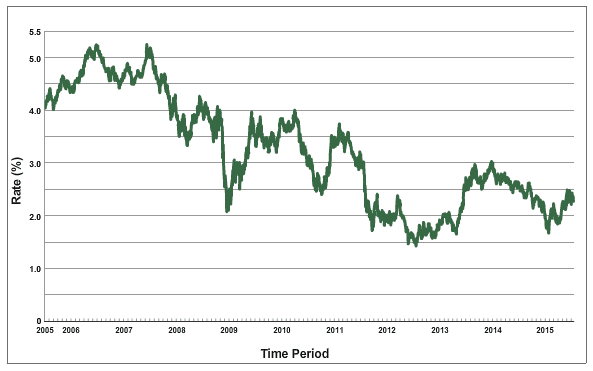

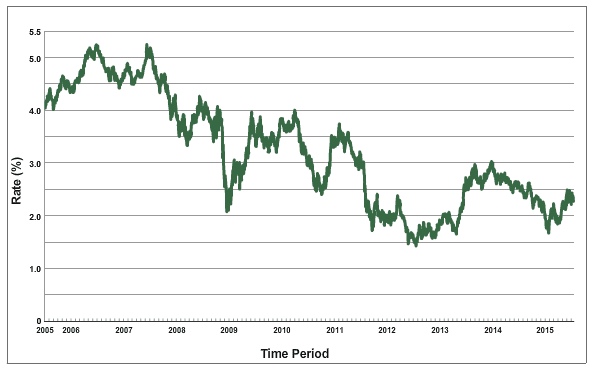

Source: US Department of Treasury

Some believe that interest rates will increase at a slow pace. However, absent the presence of a crystal ball, the exact pattern and timing is unpredictable. Given this information, investors must decide what seems reasonable for Treasury rates, how that compares to what the market expects as suggested by the forward yield curve, whether growth prospects are similar in magnitude and likelihood as compared to recent years, and if investors agree or should agree about said prospects in the near future. These inclinations will enable investors to decipher what the near 7% MLP yield means for the timing of an investment in the long-term build-out of energy infrastructure in North America.

{kind=link}

{kind=link}

{kind=link}